- Today, the ECB delivered a 25bp rate hike and indicated that it is now on pause, which is fully in line with our expectation.

- ECB still expects inflation will ‘remain too high for too long’, but it now wants to work with the ‘patience’ argument more than the ‘level’ argument for additional hikes, i.e. see the lagged effect of the monetary policy tightening already implemented impact the inflation outlook.

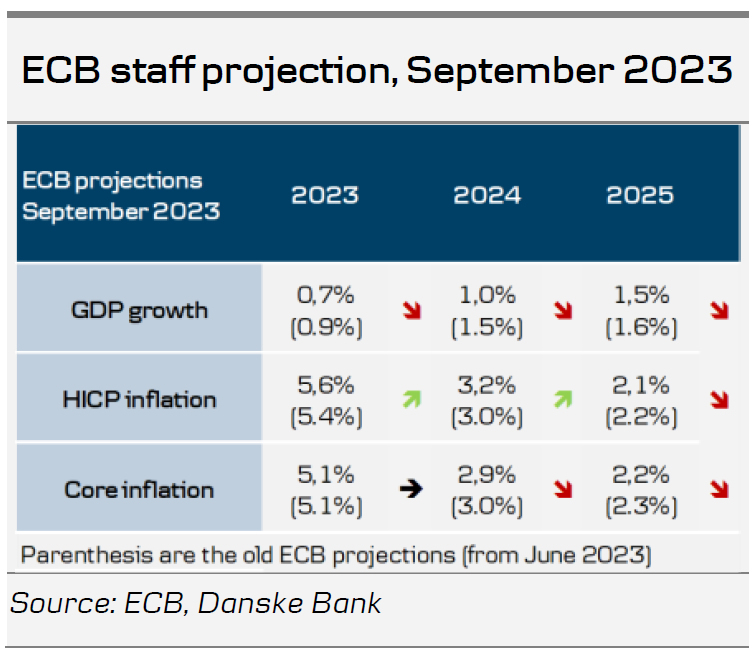

- The ECB’s staff inflation projection was revised higher for 2023 and 2024 but lower for 2025. For core inflation, the projection is now slightly lower across the board.

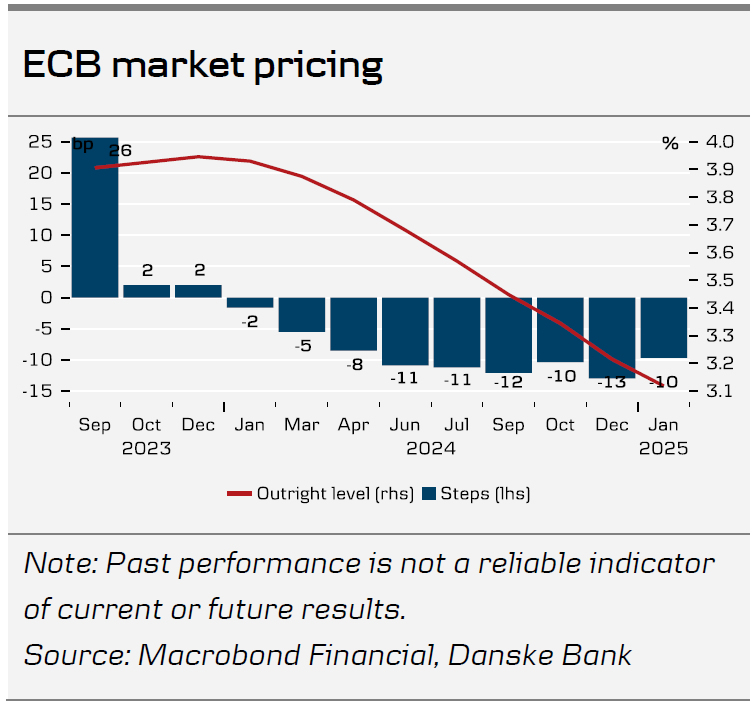

- We recommend to pay the December 2023 ECB meeting.

No additional ECB hikes

Today, the ECB announced that all three policy rates will be hiked by 25bp (effective from 20 September) and guided that it will not make any more hikes for now. In our view, the monetary policy statement can best be described as a balancing act in a stagflationary-ish environment. The ECB’s clear message to markets is that inflation is still too strong, but economic activity and the outlook are weaker. As a result, today’s decision should be seen as a compromise in the governing council. During the Q&A session, president Lagarde also said that today’s hike was taken on the back of a ‘solid majority’ as ‘some’ members favoured a pause to see how the monetary policy decisions already taken so far are working through the economy.

It was somewhat surprising to us that the ECB didn’t include much optionality for additional rate hikes, should the incoming data warrant it. The guidance provided was clear the ECB is on pause for now as it weighs the weakening economic outlook and its impact on inflation. As usual, Lagarde also highlighted that the three key elements still prevail in their reaction function: monetary policy transmission, inflation outlook and the economic and financial data. As such, given the current information, the ECB is done with further hikes, but should economic acitivity hold up better than anticipated or inflation see another rise near term, the ECB is ready to adjust its policy rate. Overall, we see the ECB’s monetary policy-setting approach focusing on the ‘patience’ argument and not the ‘level’ one.

During the Q&A session, Lagarde also said that the transmission channel is working faster in the current hiking cycle than in previous hiking cycles.

The ECB didn’t discuss advancing PEPP reinvestments or potential APP sales today. The Italian-German bond spread tightened marginally on the ECB not having discussed further balance sheet normalisation.

Cooling economy lowers staff projection of growth and core inflation

Lagarde characterised the current economic environment as a period with sluggish growth. The service sector now looks weak too, but real incomes will underpin consumer spending. The labour market is still strong amid signals that employment demand is fading. Lagarde stressed that the ECB expects inflation to decline significantly in the coming months due to base effects from energy prices last year. However, inflation is expected to remain too high for too long.

The new staff projections revised the inflation forecast higher for 2023 and 2024 but lower for 2025. Headline inflation is now expected at 5.6% in 2024 (vs 5.4% in June), 3.2% in 2024 (vs 3.0% in June) and 2.1% in 2025 (vs 2.2% in June). The upward revisions mainly reflect a higher path for energy prices since the forecast in June. The ECB revised down projections for core inflation by 0.1pp for both 2023 and 2024, while 2025 was left unchanged. The ECB acknowledged that underlying inflationary pressure remains high, even though most indicators have started to ease. The lower estimate for core inflation reflects that the previous policy tightening is working its way through financial conditions into the real economy. Hence, the wage forecast for 2024 was revised down to 4.3% from 4.5% in June. The ECB lowered the forecast for growth to 0.7% in 2023 (vs 0.9% in June), 1.0% in 2024 (vs. 1.5% in June) and 1.5% in 2025 (vs. 1.6% in June). Most of the downward revision for 2024 is due to carry over from sluggish growth in second-half 2023.

Risks to the economic outlook are tilted to the downside due to stronger monetary policy transmission and weak external demand. These two factors pose downward risks to the inflation outlook while upside risks to inflation include higher than expected energy prices, wage increases and profits.

ECB has finished hiking, but paying the Dec ECB meeting is attractive from a risk-reward perspective

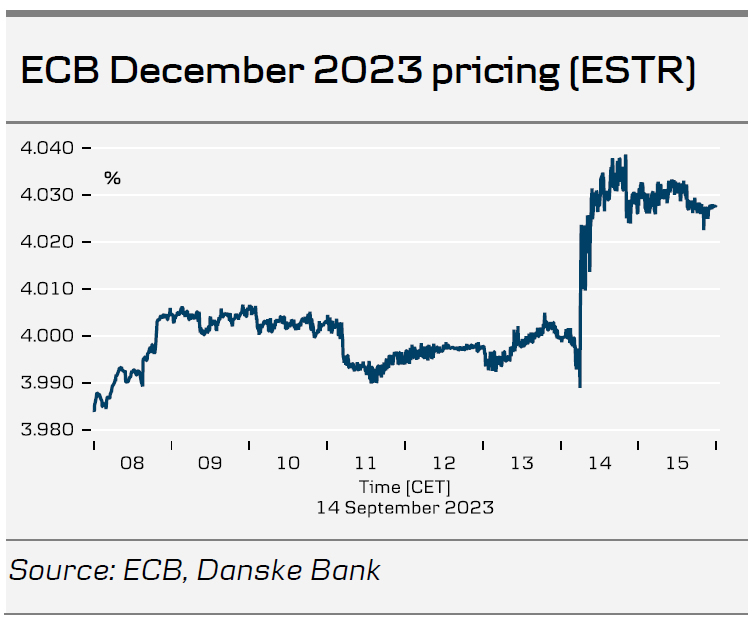

With the ECB guiding that its policy rate has ‘reached levels that have been maintained for a sufficiently long duration’, we observe that markets are pricing 4bp of additional hikes this year. And while our baseline is for the ECB not to make further rate hikes, we still recommend to pay the Dec23 ECB meeting with an entry level of 4bp and a target of 12bp, which we perceive as an attractive risk-reward. With the ECB’s hike today, we book a 19.5bp profit on our paid September ECB meeting, which we initiated on 1 September. Markets are pricing 73bp of rate cuts in 2024, which is 7bp more than before the meeting.

EUR weakness and USD strength

EUR/USD first declined towards 1.07 on the dovish 25bp rate hike from the ECB, and shortly after further declined well below the 1.07 mark on stronger-than-expected US retail sales. The USD broadly strengthened in the G10 space, while the EUR fell to its weakest level since May this year. Altogether, the dovish hike from the ECB and ongoing US outperformance are weighing on the cross. The next big event for the cross should be the Fed meeting on 20 September. We expect a relatively muted market reaction on that meeting, as it is highly expected that the Fed will be on hold.

Overall, we make no changes to our EUR/USD forecast, and hence we maintain our strategic case for a lower EUR/USD based on relative terms of trade, real rates and relative unit labour costs. As we deem that peak rates have now been reached – we do not expect further rate hikes from the Fed or the ECB – we expect the relative strength of the US economy to continue weighing on the EUR/USD in the coming months as growth differentials take the driver’s seat, and we continue to forecast the cross at 1.06/1.03 in 6/12M. As it is hard to imagine a sudden change of the current USD momentum, and with commodity prices currently rising, we may reach our 6M forecast for the cross earlier than expected.

and guided that it will not make any more hikes for now. In our view, the monetary policy statement can best be described as a balancing act in a stagflationary-ish environment. The ECB's clear message to markets is that inflation is still too strong, but economic activity and the outlook are weaker. As a result, today's decision should be seen as a compromise in the governing council. During the Q&A session, president Lagarde also said that today's hike was taken on the back of a 'solid majority' as 'some' members favoured a pause to see how the monetary policy decisions already taken so far are working through the economy.){kind=link}