U.S. Highlights

- The third quarter is shaping up to be the strongest of the year for the U.S. economy, with GDP tracking 3.7% q/q (annualized).

- The August reading of CPI showed inflationary pressures accelerated last month, though the trend remains favorable, with the three-month annualized change on core inflation slipping to 2.4%.

- A 1-2-3 punch of risks lies on the horizon for the U.S. economy. The end of the student debt moratorium, a potential government shutdown, and the UAW strike could all leave a mark on Q4 growth.

Canadian Highlights

- We can’t fault Canadian investors for peeking south of the border for signs on what the Bank of Canada (BoC) is going to do next. The stronger than expected U.S. Consumer Price Index (CPI) print may provide a good guide for Canada’s CPI release next week.

- The BoC has spoken about the stickiness of Canadian inflation as a rationale for its higher for longer interest rate strategy. The expectation for another increase in CPI next week has government yields and mortgage rates stabilizing at higher levels.

- While inflation has been slow to respond to the BoC’s hikes, there has been a clear deceleration in Canadian economic momentum over the last few months. Look no further than the August real estate data, which showed another drop in sales activity and prices.

U.S. – Flying High in Q3, But Headwinds on the Horizon

There were a lot of new data reads on the U.S. economy this week, but on balance it is looking like the third quarter is shaping up to be the strongest of the year. Real GDP growth is on track for a nearly 4% q/q (annualized) pace! That performance is driven by defiant consumer spending, which is also close to 4% even though August retail sales weren’t much to write home about. The tradeoff, however, is that persistently higher demand undermines the Fed’s efforts to cool inflation. That was evident in the August CPI data, where both headline and core inflation accelerated relative to July.

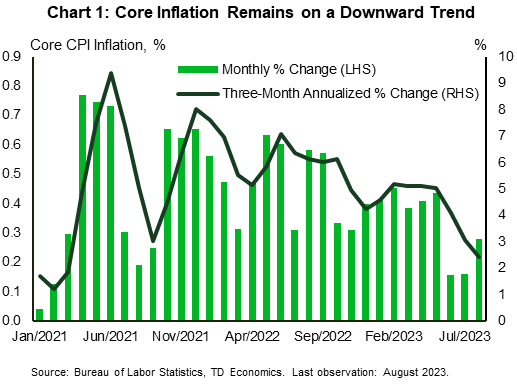

Over half of the gain in headline inflation was due to higher gasoline prices, which rose sharply alongside the recent uptick in oil prices. Meanwhile, the 0.3% m/m gain in core inflation came in a tick above expectations and bucked the trend from the ‘soft’ 0.2% gains seen in both June and July (Chart 1). However, putting these numbers in context, the monthly gain was still the third smallest in nearly two-years. Moreover, the trend on inflation remains favorable, with the three-month annualized pace cooling to 2.4% – the slowest pace of growth since March 2021.

Next week’s interest rate announcement hangs in the balance, where it is widely expected that the Federal Reserve will keep the policy rate unchanged. However, the devil will be in the details. The FOMC will also release revised economic projections, where at a minimum, they’re likely to lift the near-term growth forecast and lower the unemployment rate projection to account for the more persistent strength since the June update. The big question will be if policymakers see the near-term resilience as a source of more persistent inflationary pressures, and whether that alters the expected future path of the fed funds rate. While it is very unlikely that the FOMC would lift its terminal rate projection of 5.75% for 2023, a shallower rate cut trajectory could be signaled, reinforcing the need for rates to remain higher for longer.

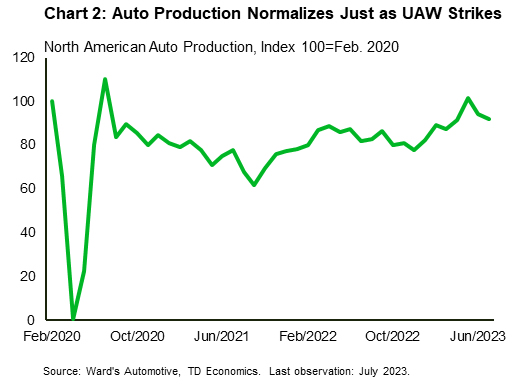

The Fed needs to thread a very small needle in its communication next week. While policymakers will need to show a continued commitment to fight inflation, coming off too hawkish runs the risk of leading to an over tightening in financial conditions. This is particularly crucial now, as there is a trifecta of headwinds to fourth quarter growth on the horizon: the end of the student debt moratorium, a potential government shutdown, and the United Auto Workers (UAW) strike. The UAW strike, which began Thursday evening, comes just as auto production had normalized to pre-pandemic levels (Chart 2). As it currently stands, the UAW has announced work stoppages at three facilities, accounting for about 7.5% of overall U.S. production. Assuming no other stoppages, this alone would shave about 0.025 percentage points (pp) for each week the strike lasts. The hit from a government shutdown is a multiple of that, while the impact of the end of the student debt moratorium could have a cumulative Q4 hit of 0.3pp. So, while growth is flying high in the third quarter, there’s the potential it ends 2023 with a thud!

Canada – Waiting in Inflation Limbo

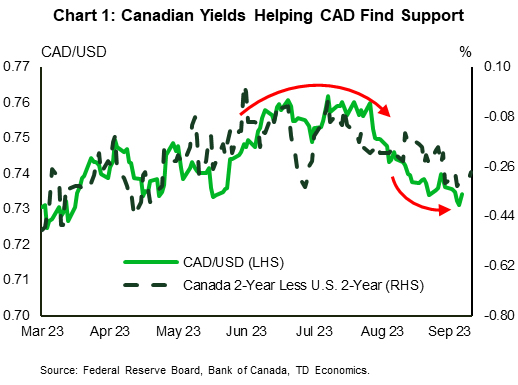

We can’t fault Canadian investors for peeking south of the border for an indication of what the Bank of Canada (BoC) is going to do next. The stronger than expected U.S. CPI print may provide a good guide for Canada’s CPI release next week. The expected rebound in Canadian inflation has raised bets of another BoC hike by year-end. Canadian yields have subsequently kept pace with their U.S. equivalents this week, putting a floor under the loonie at 73 U.S. cents (Chart 1).

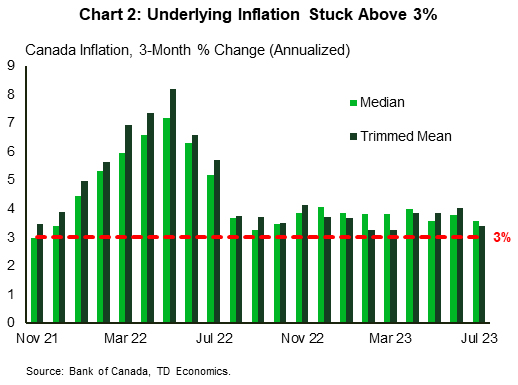

Our expectation is that Canadian consumer price inflation will show a hefty increase – hitting 3.8% year-on-year (y/y), from 3.3% y/y in July and 2.8% y/y in June. The 5% month-on-month pop in the price of gasoline will once again be the culprit for rising CPI in August. But given its volatility, the BoC would be right to look straight past that headline print and focus on the movement of core inflation. Unfortunately, we aren’t expecting much progress here. There is no longer any downdraft coming from base effects and the three-month average of monthly price movements in the BoC’s two core measures appears stuck at the mid-3% level (Chart 2). No wonder the BoC has been reinforcing that investors shouldn’t rule out more rate hikes.

Part of the rationale for the BoC’s hawkishness has been the resiliency of the Canadian consumer. Given an improved financial position, consumers have been able to withstand the impact of higher rates. Adding to this narrative was the release of Canadian household wealth data, which revealed an overall improvement in net worth. Canadian’s wealth grew by a whopping $256 billion in 2023 Q2. This only adds to the financial cushion of Canadians, who already have approximately $140 billion in excess savings that have yet to be spent. This could pose a problem for the BoC if consumers decide to spend their newfound wealth.

The one area of the economy that has been most responsive to the BoC’s policy actions has been the real estate market. When the BoC hit pause in January 2023, we saw a surge in real estate activity in the spring, sending the market decisively back into sellers’ territory. But once the BoC started hiking again in June, mortgage rates started to rise, pushing would-be buyers to the sidelines. Today’s data confirm a continuation of that trend, with sales down another 4.1% month-on-month in August. With the rise in listings bringing greater balance to the market, house prices dropped 2.3% on the month, and 5.2% in the last three months.

While there has been a clear slowing in spending, employment, and the real estate market, the better financial position of Canadians and stubbornness of inflation make the BoC’s job more challenging. And although we don’t think the BoC needs to raise rates again this year, the Bank will likely keep the door open in case economic data surprise again to the upside.

is going to do next. The stronger than expected U.S. CPI print may provide a good guide for Canada's CPI release next week. The expected rebound in Canadian inflation has raised bets of another BoC hike by year-end. Canadian yields have subsequently kept pace with their U.S. equivalents this week, putting a floor under the loonie at 73 U.S. cents (Chart 1).){kind=link}