Summary

- As widely expected, the FOMC kept its target range for the federal funds rate unchanged at 5.25%-5.50% at today’s policy meeting. The decision to keep rates unchanged was unanimously supported by all twelve voting members of the Committee.

- The statement noted that job gains remain strong, and it continued to characterize inflation as “elevated.” The Committee also reiterated in the statement that “additional policy firming may be appropriate.”

- The Summary of Economic Projections, which highlights the macroeconomic forecasts of the Committee members, was more optimistic than in June. Specifically, median forecasts of GDP growth for this year and 2024 were revised higher, while forecasts of the unemployment rate were revised lower.

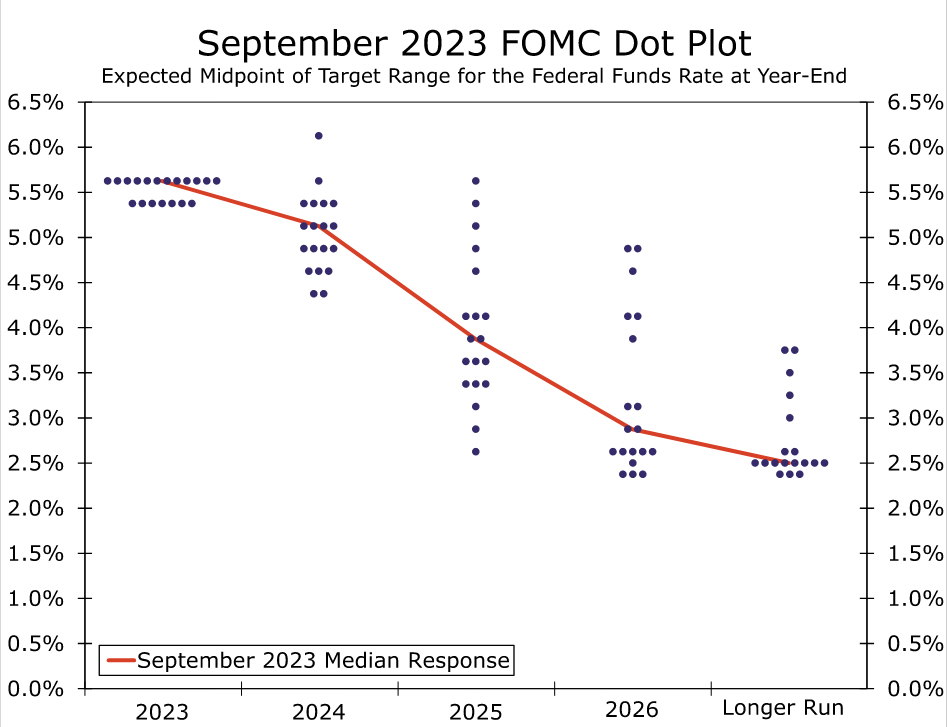

- The so-called “dot plot” showed that 12 of the 19 Committee members believe that another 25 bps of rate hikes would be appropriate by the end of this year. Furthermore, the dot plot shows that only 50 bps of policy easing would be appropriate next year, considerably less than the 100 bps of rate cuts that were forecasted in June.

FOMC Remains on Hold but Continues to Think Further Policy Tightening May Be Appropriate

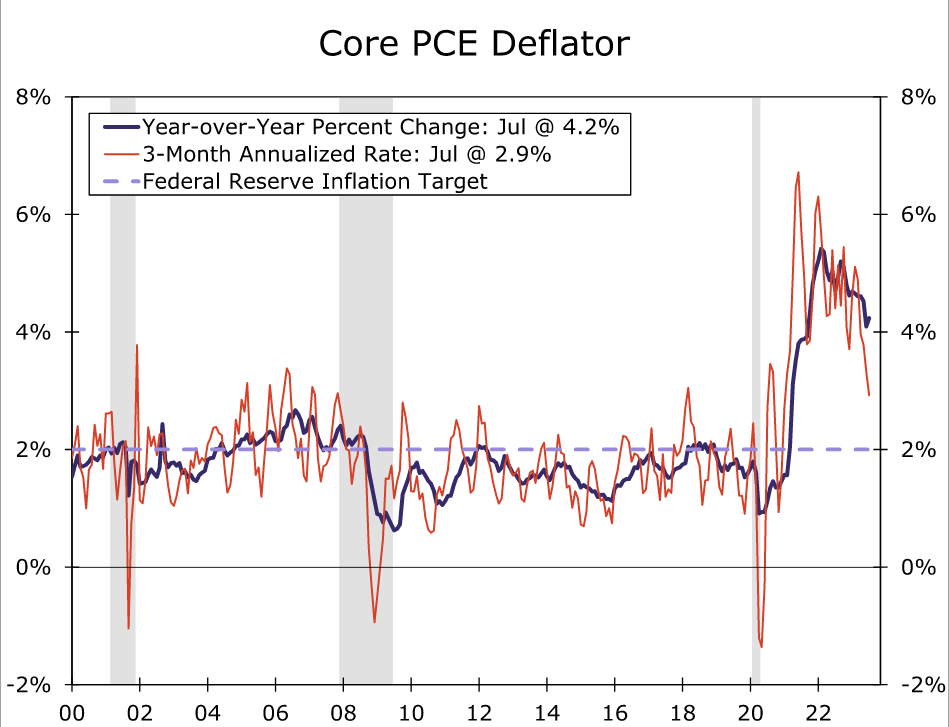

As universally expected, the Federal Open Market Committee (FOMC) decided at today’s meeting to keep its target range for the federal funds rate unchanged at 5.25%-5.50%. All twelve voting members of the Committee supported today’s decision to keep rates unchanged. In the statement that announced the decision, the FOMC said that “economic activity has been expanding at a solid pace.” Although “job gains have slowed in recent months,” they “remain strong.” The Committee continued to characterize inflation as “elevated.” Indeed, the year-over-year rate of core PCE inflation, which is the Fed’s preferred measure of the underlying rate of consumer inflation, printed at 4.2% in July, although the 3-month annualized change slipped below 3% (Figure 1). Nevertheless, core PCE inflation remains above the FOMC’s 2% target.

As has become standard boilerplate, the Committee said that it “will continue to assess additional information and its implications for monetary policy.” In that regard, the FOMC retained a hawkish bias by re-iterating that “additional policy firming may be appropriate to return inflation to 2 percent over time.” As we will discuss further below, this bias was represented in the so-called “dot plot.”

Median Dot for 2024 Revised Higher

Following its usual quarterly procedure, the Committee released an update to its Summary of Economic Projections (SEP), in which each FOMC member outlines his or her macroeconomic forecasts. As we anticipated in our recent report that outlined our expectations for the FOMC meeting, the median GDP growth forecast for 2023 rose from 1.0% in the June SEP to 2.1% today. This revision reflects the run of stronger-than-expected economic data that have been released since the June 14 meeting. At the same, the median projection for the unemployment rate at the end of this year fell to 3.8% from 4.1% previously, reflecting the continued resilience of the labor market. The FOMC also seems to think that a “soft landing” for the economy is increasingly likely. The median forecast for real GDP growth in 2024 was revised up to 1.5% from 1.1% in the June SEP, while the forecast for the unemployment rate fell to 4.1% from 4.5%.

The median forecast for core PCE inflation at the end of this year edged down to 3.7% from 3.9% in the June SEP. Notably, all FOMC members forecast that PCE inflation, whether measured by the overall rate or by the core rate, will remain above 2% at the end of next year.

These macroeconomic forecasts undoubtedly influence the placement of the dots in the dot plot. The median dot for the end of 2023 remains at 5.625% (i.e., the midpoint of a 5.50%-5.75% target range), which is unchanged from the June SEP. In other words, 12 of the 19 members of the FOMC think it would be appropriate to hike rates by 25 bps at either the November 1 meeting or at the final meeting of the year on December 13. Furthermore, there was an important change for next year. In June, the median dot for 2024 stood at 4.625%, which indicated 100 bps of rate cuts next year would likely be appropriate. The median dot today stands at 5.125%. If the FOMC does indeed raise rates by 25 bps by the end of this year, then the Committee would cut rates by only 50 bps in 2024. Although the median dot for 2025 currently stands at 3.875%, there is a wide dispersion in the forecasts, which should be expected of a forecasted variable more than two years from now. In sum, the message from the FOMC today is higher for longer, in terms of interest rates (Figure 2).

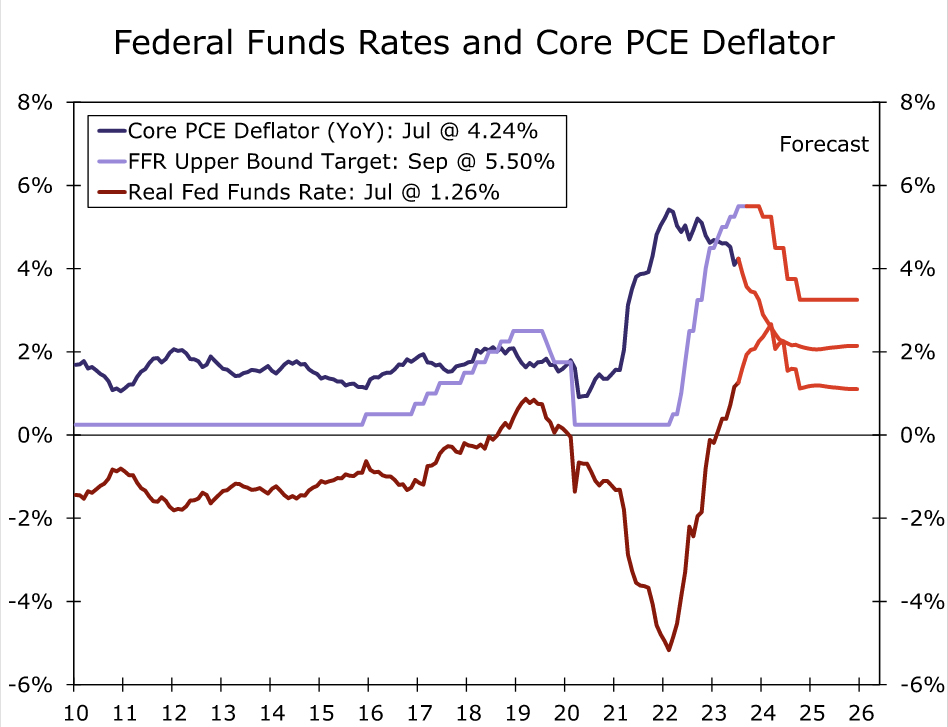

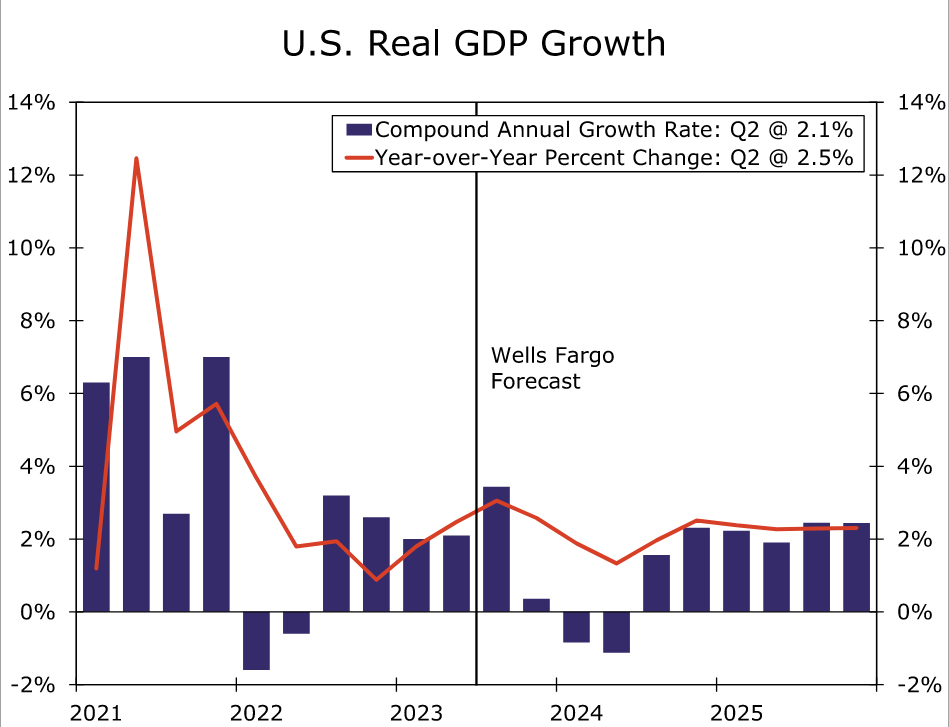

We tend to side with the seven FOMC members who believe that no further rate hikes are needed this year, although we acknowledge the risk that the Committee could indeed hike one more time. As we outlined in our most recent U.S. Economic Outlook, monetary policy will tighten passively in coming months (Figure 3). That is, even with the FOMC on hold, the real fed funds rate will creep higher in coming months if, as we forecast, inflation continues to recede. This rise in real interest rates will exert stronger headwinds on the economy, which we believe will lead to a modest contraction in economy activity next year (Figure 4). We then look for the FOMC to cut rates by more than the market (and most Committee members) currently expect. Not only will lower rates be appropriate if the economy weakens, but the FOMC will need to cut rates just to prevent an upward creep in the real fed funds rate.

{kind=link}