Economic data releases since the Bank of Canada opted to forego an interest rate hike in September have been mixed, but we expect that they on net have made a hike at next week’s decision unlikely. Inflation has surprised on the upside relative to the central bank’s last forecasts in July. But most of that was driven by rising energy inflation more recently as global oil prices edged higher. The latest CPI data for September also looked decidedly better, with slower growth in the BoC’s preferred ‘core’ measures breaking a string of upside surprises.

Underlying inflation pressures in Canada are still running well above the 2% inflation target, but softer economic growth numbers and the central bank’s own Business Outlook Survey (BOS) suggest that price growth will continue to decelerate. The Q3 BOS showed Canadian businesses have not yet returned to ‘normal’ pricing practices, but the frequency and size of price adjustment has been moving back towards pre-pandemic trends. Easing cost pressures have contributed to that, but softening consumer demand has likely also played a big role as well. Indeed, 60% of consumers surveyed in the separate Canadian Survey on Consumer Expectations reported having reduced spending in Q3 to combat elevated inflation and rising interest expenses.

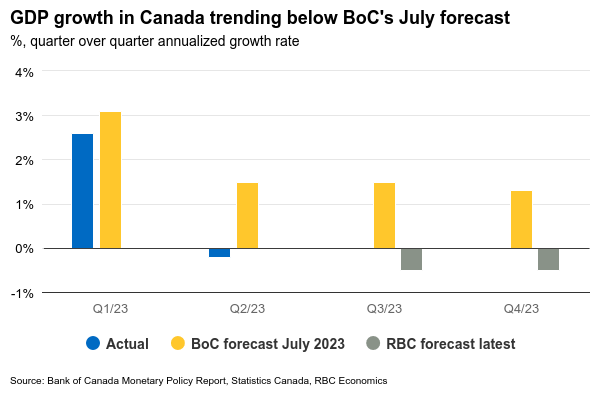

And interest rates are already at levels that should continue to slow consumer demand over time, as they pass through to increase household debt payments with a lag. Overall GDP growth is tracking well-below the BoC’s last forecasts in July, contracting 0.2% in Q2 instead of the 1.5% annualized growth the BoC expected. The change also looks substantially softer on a per-capita basis controlling for surging population growth. We are tracking another small GDP decline (-0.5%) in Q3 (BoC at +1.5%.) And labour markets are showing signs of softening with the unemployment rate up half a percentage point from the spring. Near-term inflation projections will very likely be revised higher given the rise in energy prices into the fall. But with signs the economy is cooling, we expect the BoC will likely maintain their call for a more gradual return back to the target inflation rate, somewhere in late 2024 or early 2025.

Week ahead data watch

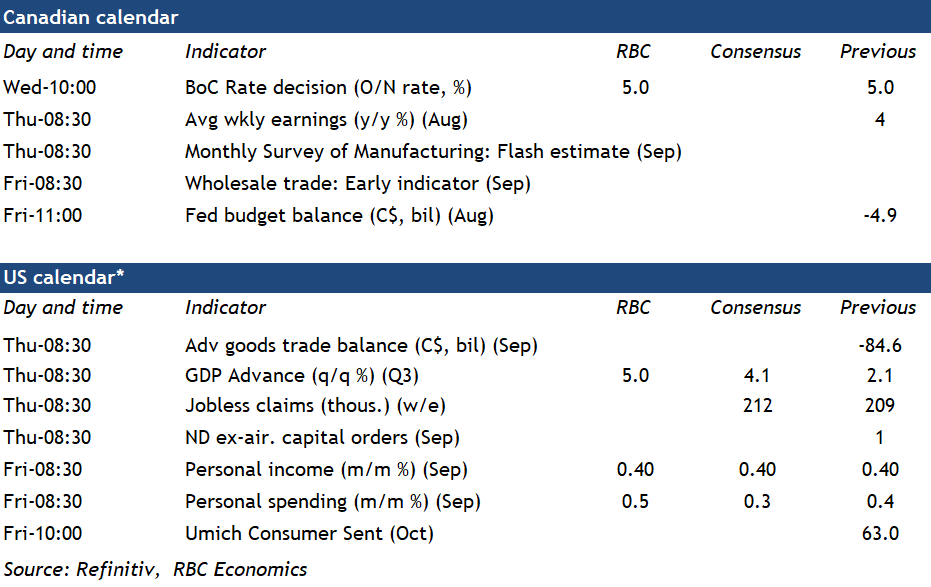

U.S. personal spending likely ticked up 0.5% in September due to strong retail sales (+0.7%) data for that month. We expect personal income to have edged up 0.4%, given earlier released September payroll report showed a deceleration in wage growth (+0.2%) during that month.

Q3 U.S. GDP is tracking a 5% quarter over quarter annualized increase on firm consumer spending, a larger net trade build and a jump in inventories.

For Canada, we look for more signs of softening labour demand from the August SEPH report. Job openings have been declining, and we expect that trend to continue. Employment growth from the latest Labour Force Survey was still robust, but the unemployment rate has ticked higher to 5.5% since spring, consistent with ongoing softening in labour demand.

{kind=link}