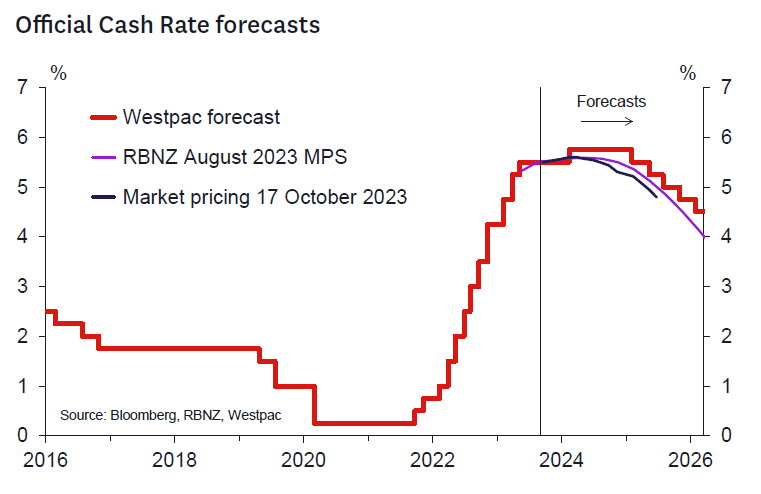

The RBNZ has had a tough balancing act to manage in recent months. Core inflation pressures –especially those related to domestic prices – remain elevated two years after the start of the interest rate hiking cycle. In addition, economic activity and net migration have exceeded the RBNZ’s expectations and the housing market is stirring. But at the same time, we are seeing mounting evidence that growth is turning down, there’s been softness in some key overseas markets, and longer-term interest rates have pushed higher both in New Zealand and abroad.

With arguments on both sides, the Westpac Economics team has again been considering how the outlook for monetary policy might evolve over the coming year or so. To help organise our thoughts and promote thought and debate, we have marshalled a range of hawkish and dovish considerations that, while not exhaustive, could influence the future direction of policy. We don’t weigh the various arguments to reach a conclusion, but we seek to highlight the issues we have been thinking about as we mull over the outlook in preparation for our updated Economic Outlook later this month. We invite feedback on the perspectives we discuss here and any additional relevant viewpoints.

The Hawk’s Eye View.

Net migration surge underpins strength in demand and inflation (see Figure 1).

- Net migration rose to a record 110,000 in the year to August and is set to rise further over the coming months, pushing population growth to the highest levels we’ve seen in decades.

- While population inflows are helping to address labour shortages, they are also adding to demand. That could mean current domestic inflation pressures take longer to dissipate.

- The strength in migration could also add to pressures in the housing market. New rents are already rising rapidly in larger regions like Auckland.

Housing market resurgence frustrates disinflation (see Figure 1).

- The earlier fall in house sales and prices has been arrested, and the housing market is now turning upwards despite increased borrowing rates.

- First home buyers/owner occupiers could be joined by investors given the more investor friendly policies campaigned on by the incoming centre- right government.

- A further resurgence in the housing market could boost demand more generally, including related increases in household spending or construction.

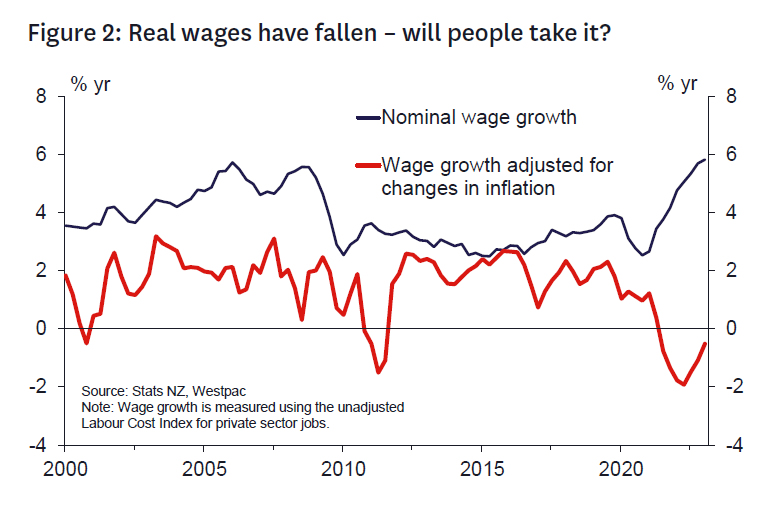

Strong household income growth prevents significant disinflation (see Figure 2).

- Strong job and wage growth relative to productivity growth could underpin domestic demand.

- The unemployment rate remains low, the labour participation rate is at record highs and employment is elevated, supporting household income growth.

- Workers pursue real wage gains/protection (e.g., through multi-year wage agreements) that prevent disinflation in the services/non-tradables sectors.

- Savings rates have risen since the pandemic, and households are ahead on mortgage repayments.

Output growth does not decline significantly due to bottoming confidence and population growth.

- Households and firms have weathered the worst and now anticipate rising asset prices and near peak interest rates.

- Public sector capex remains strong due to infrastructure needs, including replacing damage from this year’s storms.

Risk of an exchange rate correction as global risk-free rates ratchet higher (see Figure 3).

- Global risk-free interest rates are adjusting up to reflect a higher than pre-COVID norm in part reflecting persistent global inflation.

- NZ rates need to remain high to manage exchange rate risks from the elevated current account deficit. Related risk for imported inflation.

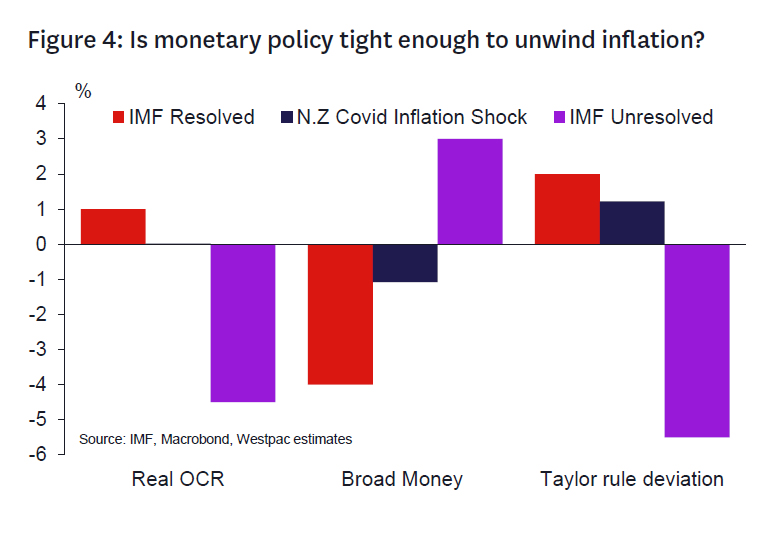

NZ interest rates are higher but not high (see Figure 4).

- Higher interest rates have disproportionately affected upper quintile income households who have a lower propensity to consume.

- Other households have seen strong income growth (reflecting labour market shortages during COVID) and their wealth has not been reduced by falling asset prices.

- Aggregate demand proves resilient as nonmortgagees continue to spend.

- Comparing the RBNZ tightening cycle since Covid-19 against the metrics determined in a recent IMF study on the metrics associated with countries who have in the past successfully versus unsuccessfully unwound large inflation shocks could suggest the RBNZ has not done enough.

Inflation remains persistently high, resulting in high inflation expectations.

- RBNZ needs to pursue tighter policy to dislodge inflation.

The Dove’s Tale.

Monetary policy works with long and variable lags; policymakers need to be forward-looking.

- The economy is growing below trend and key upstream indicators of inflation are clearly moving in the right direction, even though policy is yet to attain its maximum effect.

- As long as those upstream indicators maintain their current trend, the RBNZ can afford to be patient and allow the current policy stance to work.

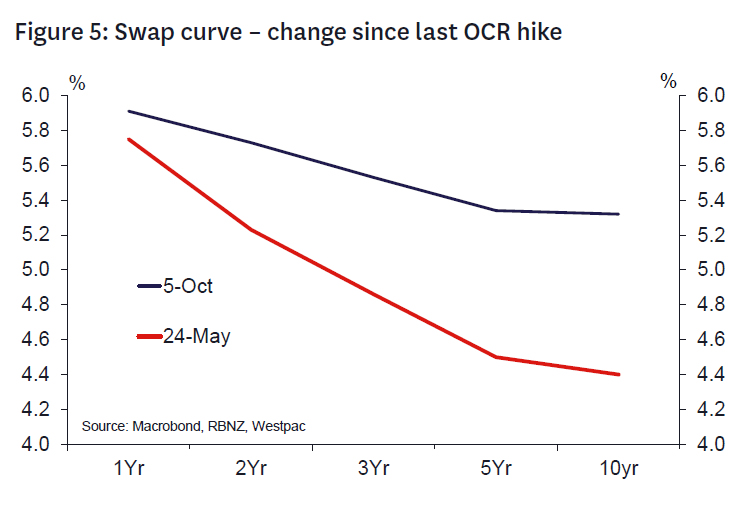

Markets are now working with the RBNZ, rather than against it (see Figure 5).

- Earlier in the year markets were undermining the effectiveness of the RBNZ’s stance by pricing in an early easing, keeping longer term interest rates lower than otherwise.

- The recent sharp rise in longer term interest rates (and thus mortgage rates) means that the RBNZ now has greater leverage for a given OCR, tightening overall financial conditions.

Tightening further would add volatility to the economy.

- Tightening further to achieve a quicker decline in inflation would result in a steeper downturn in the economy, potentially making it more difficult to calibrate the eventual easing.

- Adding volatility to growth and interest rates increases uncertainty for businesses, which is as detrimental to the economy as temporarily above-target inflation.

Households are yet to feel the full impact of past rate hikes (see Figure 7).

- Mortgage rate fixing has delayed the impact of OCR hikes. A sizeable rise in debt servicing costs will occur in 2023/24, even more so now given the recent lift in mortgage rates.

- The effective mortgage rate will rise well above pre- Covid average levels, crimping household spending and homebuilding.

Downside risks for Chinese growth remain.

- Chinese households are overleveraged, asset prices are overvalued and consumer confidence is weak.

- While Chinese authorities have announced numerous small measures aiming at boost the economy, it remains to be seen whether they will have a durable impact.

Aside from China, there are a number of other risks that could impact negatively on the economy.

- Global inflation proves persistent requiring further policy tightening offshore, leading to slower global growth and weaker demand for New Zealand’s exports.

- The recent flare-up in the Middle East could develop into a regional conflict, weighing on business confidence here and abroad.

- A severe El Nino could depress agricultural production in the coming summer.

Inflation dampening impact of migration flows.

- Migrant inflows are helping reduce labour shortages and wage pressures, which should help to moderate services/non-tradeable inflation over the coming year.

- Business surveys highlight a very sharp easing in labour market pressures.

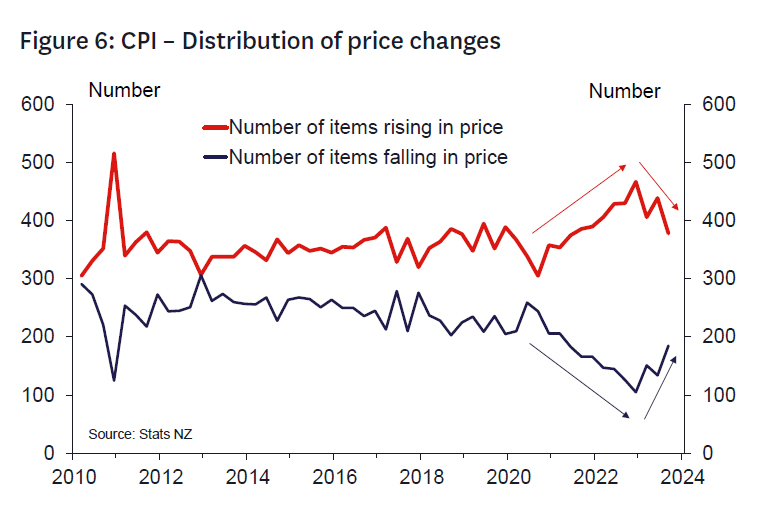

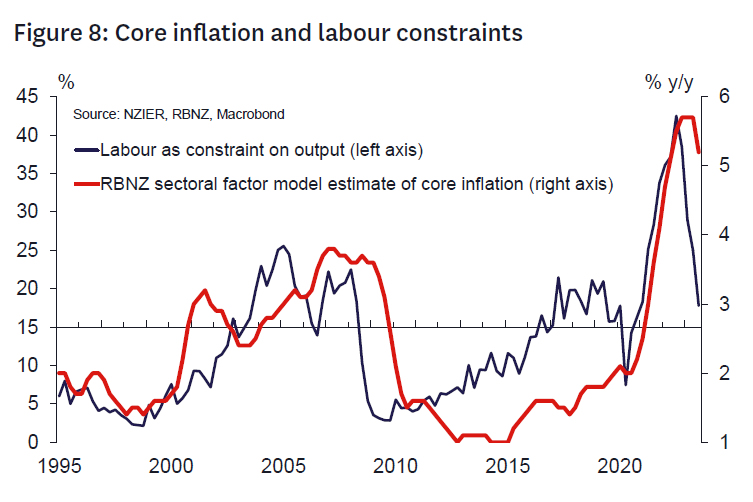

Core inflation proves less sticky than feared (see Figure 6,8).

- Encouragingly, inflation expectations have continued to decline despite a rise in petrol prices in recent months, suggesting that the RBNZ’s credibility remains intact.

- Increasingly fewer items are rising in price and more items are falling price, suggesting the inflation surge is already narrowing.

Fiscal policy is likely to be more contractionary following the recent General Election.

- The National Party intends to run a modestly more contractionary fiscal policy than the outgoing government, and its likely coalition partners could lead policy to be tighter still.

- At the very least, the risk of fiscal targets being missed seems likely to be lowered.

{kind=link}