U.S. Highlights

- The 10-year Treasury yield briefly surpassed 5% earlier this week. Though yields have since retraced, the 10-year looks to end the week at a still elevated 4.85%.

- The advance estimate of GDP showed the economy registered its strongest gain in nearly two years in the third quarter, with most major areas of spending recording gains.

- The FOMC is expected to hold rates steady next week, but the uptick in September inflation along with any signs of continued labor market strength in next week’s data will tilt the scales in favor of another rate hike later this year.

Canadian Highlights

- Fears around what higher-for-longer rates might do to growth dominated markets this week. Equities were lower and yields fell. Meanwhile, easing concerns of a wider Middle East conflict weighed on oil.

- The Bank of Canada held the policy rate at 5% this week. Their Monetary Policy Report emphasized the economic toll from higher rates, consistent with no further hikes.

- However, policymakers retained a hawkish tone, given still robust wage growth, elevated inflation expectations and corporate pricing behaviour that’s yet to normalize.

U.S. – Economic Resilience on Full Display in Third Quarter

Longer-term Treasury yields continued to creep higher through the early portion of the week, as the looming threat of a mid-November government shutdown, increased Treasury issuance, and heightened geopolitical tensions remain key drivers pressuring the term-premia higher. After briefly surpassing 5% earlier this week, the 10-Year Treasury yield has since pared its gains and currently sits at a still elevated 4.85%. Meanwhile, equities edged lower for the second straight week – down 2% at the time of writing – but remain 8% higher on the year.

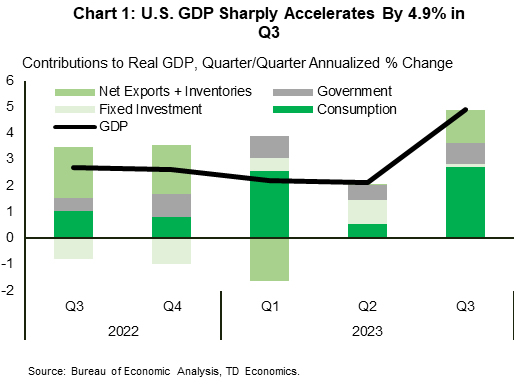

Turning to the economic data calendar, the Bureau of Economic Analysis (BEA) released its advance estimate of third quarter real GDP. The report showed economic activity accelerating at more than double the rate of expansion seen in Q2. The ongoing theme of economic resilience was on full display last quarter, with most major areas of spending recording gains. The strength in consumer spending was particularly eye-catching, jumping up 4.0% (Chart 1). The summer shopping spree was fueled by a resilient labor market and a further drawdown of the excess savings accumulated during the pandemic. Moreover, because many homeowners locked-in mortgages at ultra-low rates in 2020/21, the passthrough of higher interest rates to the consumer has been more muted relative to past tightening cycles.

Perhaps more concerning for policymakers is that spending momentum heated up at the end of the third quarter. September’s gain was the second strongest over the past eight months, and suggests consumers didn’t hold back last month, despite the looming headwind of student loan repayments restarting in October. At this point, we see Q3’s blowout numbers as the ‘last hurrah’ and expect a more tepid pace of consumer spending (1.5-2%) for Q4, before slipping sub-1% through the first half of next year.

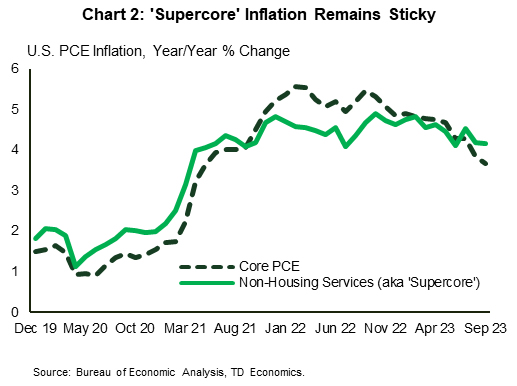

Should the consumer prove more resilient, that will spell trouble on the inflation front. In fact, core PCE inflation data for September has already telegraphed some evidence of progress stalling. Price growth picked up to 0.3% m/m (up from the 0.17% m/m gains averaged over the three prior months), with notable strength in Powell’s ‘supercore’ measure, which has barely budged from last year’s highs (Chart 2).

From the Fed’s perspective, nothing out this week will influence next week’s interest rate decision. At this point, markets are fully priced for the FOMC to hold rates steady, and only attach a 20% probability to another rate hike in December. However, that could quickly change over the next week should the FOMC statement and/or Powell’s press conference strike a more hawkish tone. Next week’s Employment Cost Index release for the third quarter is also important given it contains a measure of wage inflation that the Fed watches closely. As well, October’s employment figures out Friday will be closely scrutinized as usual. Unless these reports show a definitive sign that the labor market is cooling, which looks unlikely given the recent strength in higher frequency indictors including jobless claims and Indeed job posting data, another rate hike come December seems inevitable.

Canada – Holding the Line

The mood in financial markets was more dovish this week, on concerns on what higher-for-longer rates could mean for growth prospects. The North American benchmark WTI slid about $3 per barrel, greased by weaker-than-expected seasonal demand in the U.S. and (likely) some degree of assurance that the Israel/Hamas conflict would be regionally contained. This decline helped pull the TSX to its lowest level since October of last year. Even the sustained and severe upward march in bond yields observed over the past several months hit a pause this week, with yields down across the curve.

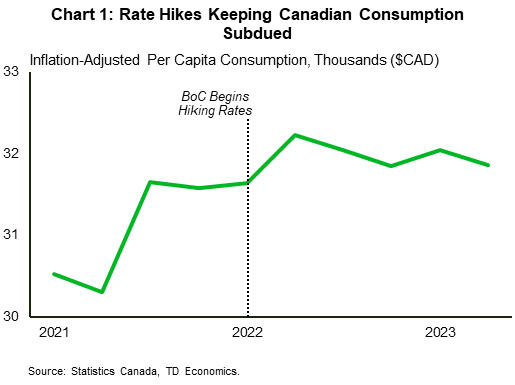

The pullback in yields doesn’t change the fact that they remain near-multi year highs and are exerting a braking force on the Canadian economy. The Bank of Canada hammered this point home in this week’s interest rate announcement. The Bank stood pat on rates, and the accompanying Monetary Policy Report (MPR) even included a special section detailing the impact of rates on economic activity. Policymakers noted that inflation-adjusted per capita consumption has stalled since the Bank started hiking rates (Chart 1), weighed down (to varying degrees) by both rate-sensitive and non-rate-sensitive goods and services.

The impact of higher rates also shows up in the Bank’s near-term growth projections, where they are forecasting (annualized) gains of 0.8% for GDP in both the third and fourth quarters of this year. While we wouldn’t quibble too much with these projections, monthly GDP data suggests some modest downside risk to the Bank’s Q3 forecast. Preliminary estimates had pointed to a 0.1% month-on-month gain in August, although we’ll receive confirmation of that (alongside an early read on September) when the monthly GDP data is released next week.

While softer growth would certainly be consistent with our view that the Bank is done hiking rates this year, we can’t necessarily close the book on that possibility. The Bank upgraded its inflation forecast for this year and next, while making pains to emphasize their concern that core inflation is not cooling as rapidly as expected. They also noted that inflation expectations are far from normal while corporate pricing behaviour also has yet to normalize.

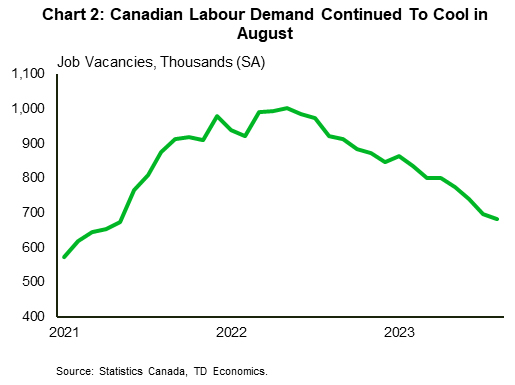

In addition to these factors, the Bank remains concerned that a tight job market is keeping wage growth in the 4-5% range, which is simply too strong to move inflation to their 2% target, especially given Canada’s poor productivity. Our view is that wage growth will likely cool moving forward amid robust population growth and an economy that’s struggling to keep its head above water. Notably, this week’s Survey of Employment Payrolls and Hours showed some cooling in wage growth, declining payroll employment and falling job vacancies for the month of August (Chart 2). Next week, all eyes will be on Friday’s Labour Force Survey release, which will offer the latest temperature reading on wage growth.

{kind=link}