U.S. Highlights

- The Federal Reserve’s policy statement took center stage this week. As expected, the Fed kept policy rates unchanged but preserved the option of hiking in the future.

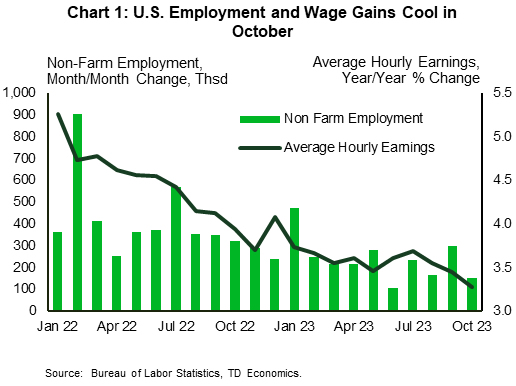

- Hiring in the U.S. slowed in October, with wage gains decelerating and the unemployment rate edging up.

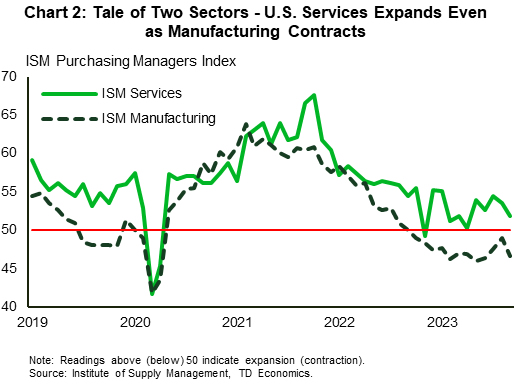

- Activity in the manufacturing sector continued to contract in October, in contrast to the continued expansion in the services sector (though at a slower rate).

Canadian Highlights

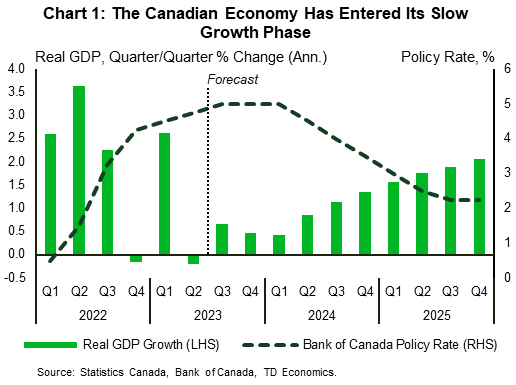

- GDP growth in the month of August and September is reigniting chatter around a Canadian recession. It’s too early to tell, but the Canadian economy is evidently slowing.

- Canada’s labour market continued to add jobs in October, but not enough to keep pace with labour force growth, pushing the unemployment rate higher.

- The Bank of Canada (BoC) likely welcomed this week’s developments. Their decision to hold the policy rate at 5.00% last meeting is shaping up to be the prudent move.

U.S. – The Fed’s Door is Still Open

The U.S. economic calendar was packed this week with a mix of key data, central bank meetings and even Treasury auction announcements. To start things off, the Treasury announced its financing requirements for the upcoming quarter. In the announcement, issuance is dominated by shorter dated securities (2-7 year), with planned 10-to-30-year range issuance less than most had expected. What’s more, Treasury’s projection that it will slow the recent flood of new long-dated debt, contributed to a rally in the bond market and a pullback in long-term yields.

The next key focus was the labor market, with varying reports giving snapshots of the state of this important sector. November’s nonfarm payrolls, the most important, showed that hiring in the U.S. economy has slowed. Additionally, the pace of wage growth has cooled (Chart 1). The unemployment rate also edged up slightly, bucking expectations for no change. The job opening and labor turnover survey (JOLTS) was slightly backward looking, covering September, and showed an increase in job openings, which was offset by a rise in the number unemployed, leaving the ratio of the two largely unchanged at 1.5. The pace of hiring also eased and the quit rate levelled off at its pre-pandemic rate. The employment cost index on the other hand showed that wage gains ticked up in the third quarter, but compensation growth still slowed from 4.5% to 4.3% on a year-on-year basis. Overall, the labor market metrics are consistent with what the Fed wants to see – a market that is slowly cooling with likely further deceleration in wage pressures ahead.

As widely expected, the Federal Reserve held interest rates steady at 5.25%-5.50% on Wednesday. This is the first time in the current tightening cycle that the Fed has paused for two consecutive meetings. However, the central bank still left the door wide open to potentially raising rates in the future if needed to keep the disinflation momentum going. October’s cooling in the labor market combined with expectations that economic activity will pullback in Q4, suggests that they may not need to walk through it before the year is done, but only time (and the data) will tell.

One sector of the economy that is not fairing very well is the manufacturing sector. Activity in the sector, as measured by the ISM sentiment survey, continued to contract in October, falling to its lowest level since July, on broad-based weakness. The silver lining, however, is that a pullback in raw materials prices is easing cost pressures, which should help to mitigate price pressures for consumer goods. The services side of the economy fared a bit better, with the ISM services index expanding again in October, though at a slower pace (Chart 2). Twelve out of eighteen industries reported growth; however, the softer-than-expected reading suggests that the Fed’s hiking campaign is influencing the services sector as well.

The takeaway from the week is that if the disinflationary trend remains intact, the Fed’s December decision is a tougher call. There will be several economic releases over the next six weeks that will influence the Fed’s decision. But, so far, consumer spending momentum has remained stronger than expected, risking an uptick in inflation. This still suggests that the Fed’s work is likely not done.

Canada – Proceeding With Caution

The “R” word has crept back into discussion this week. Could the Canadian economy already be in a recession? Technically speaking, maybe–but we won’t know until official third quarter GDP readings land at the end of the month. GDP updates this week for August (no growth), combined with guidance for flat growth in September, suggests that third quarter GDP could have contracted by a very small 0.1% annualized rate. If so, that would mark a technical recession, given the narrow decline in economic activity in the quarter prior.

Technicalities still matter, but economic activity would be better characterized as flat over the last two quarters. On the one hand, this is impressive as the economy battled through significant wildfire activity, major strikes, and other idiosyncratic shocks concurrently with multi-decade high interest rates. On the flip side, this is clear evidence that the economy is cooling. From here, we expect a prolonged period of below-trend growth before activity picks up in the second half of next year, alongside interest rate cuts commencing around the mid-year mark (Chart 1).

The Canadian labour market is also slowing but hasn’t fully ceded its strength. The Canadian economy added another 18k jobs in October, pulling the three-month trend in job gains slightly upward. The unemployment rate, however, has moved up seven-tenths since April, as labour force gains outpaced employment. The labour market is holding up relatively well at this point in the cycle, but the Bank of Canada (BoC) likely wants to see the market move further into balance. Notably, wage gains are still robust, potentially fanning future inflation fears and vacancies, while declining, are still at elevated levels.

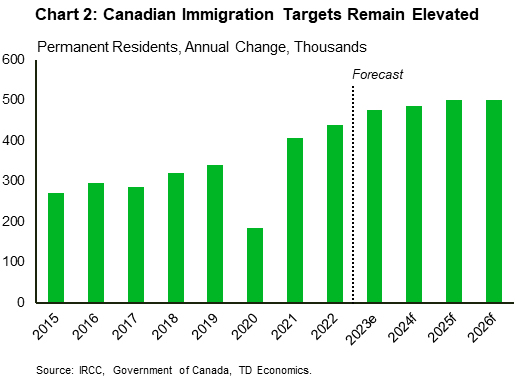

Strong labour force and employment growth in the last year were a function of the rapid population increase across the nation. Over the last 12 months, Canada added over one million people, which provided an impulse to hiring and spending. The Canadian government updated its immigration plan this week, targeting 485k, 500k, and 500k new permanent residents in 2024, 2025, and 2026, respectively (Chart 2). These targets suggest that population gains will remain durable, adding upward pressure to labour force growth as employment continues to moderate.

The BoC’s mission is to get inflation back to its two-percent target. Governor Macklem and Deputy Governor Rogers reiterated the BoC’s policy stance this week in two separate testimonies, nailing down a few key points. Firstly, further easing in inflation will take some time, but that if inflationary pressures exist, they are “prepared to raise the policy rate further to restore price stability”. Secondly, just as we have highlighted above, the BoC has acknowledged that the Canadian economy is showing clear signs slowing and will continue to do so as higher interest rates curb consumer spending and rebalance supply and demand. Overall, developments this week should add a layer of comfort to the BoC’s decision to stand pat on the 5.00% policy rate.

, with planned 10-to-30-year range issuance less than most had expected. What’s more, Treasury’s projection that it will slow the recent flood of new long-dated debt, contributed to a rally in the bond market and a pullback in long-term yields.){kind=link}