Summary

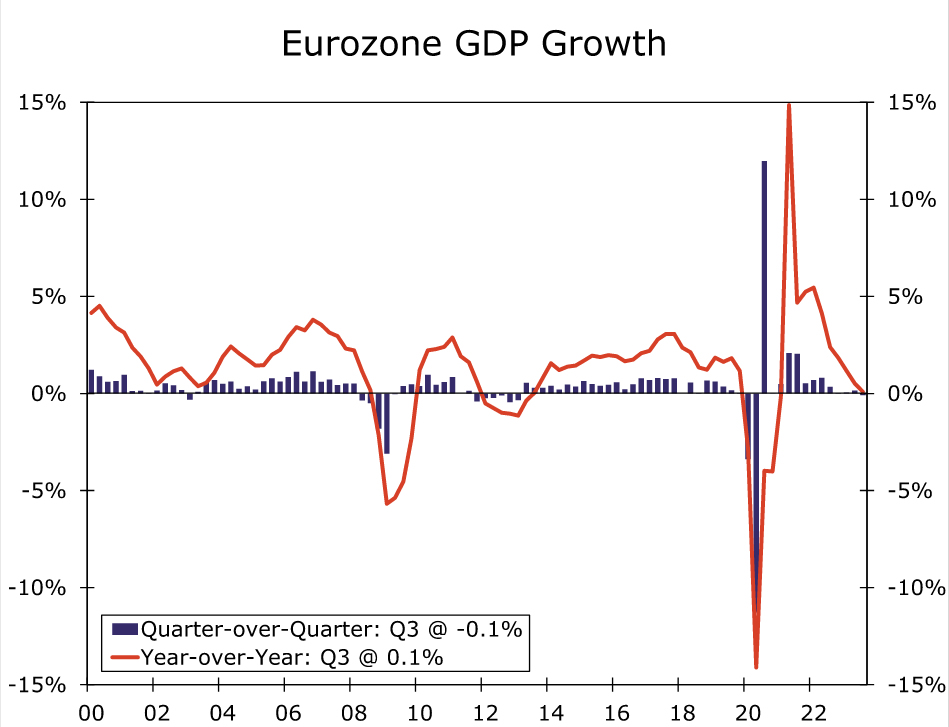

- The Eurozone has continued to deliver disappointing economic data as Q3 GDP shrank 0.1% quarter-over-quarter, the first decline (outside of the pandemic) since early 2013. With recent activity and survey data remaining soft, the natural question to ask is whether the Eurozone is on the cusp of, or perhaps already in, recession.

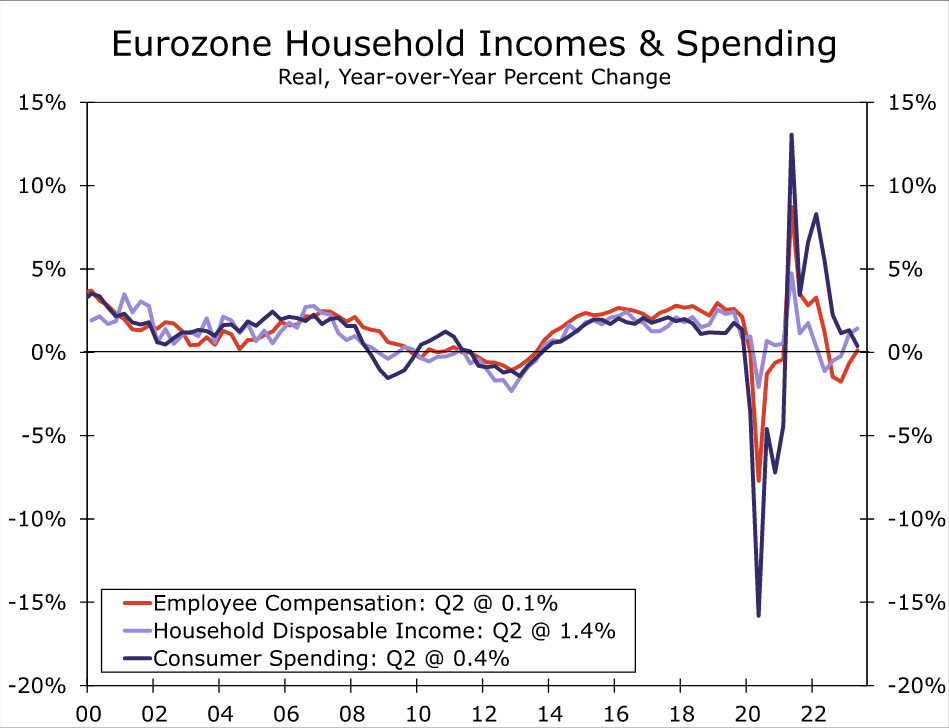

- One notable area of weakness has been consumer spending. That said, we believe the worst of the consumer slowdown may now have largely passed, as real household income trends have turned more positive and household interest costs have risen only moderately. We do, however, expect a further slowdown in investment spending given slowing corporate profit growth and declining capacity utilization rates.

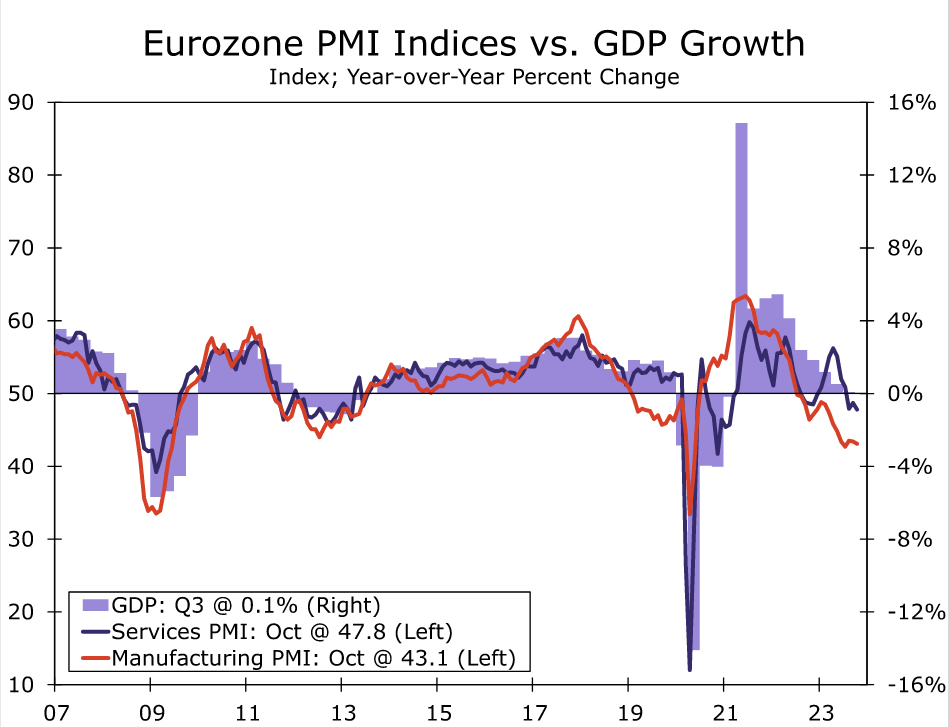

- The mixed outlook for consumer and investment spending leaves the Eurozone very close to recession. While we are not calling for recession just yet, should the PMI surveys stay at their current contractionary levels in the months ahead or soften further, an economic downturn may eventually become unavoidable.

- The underwhelming growth outlook means European Central Bank (ECB) rate hikes are very likely done, with the most recent progress on the inflation front reinforcing the view that the peak in policy rates has already been reached. However, we believe the ECB will still want to see underlying inflation trends move closer to, and remain near, its 2% inflation target before it becomes comfortable embarking on a monetary easing cycle.

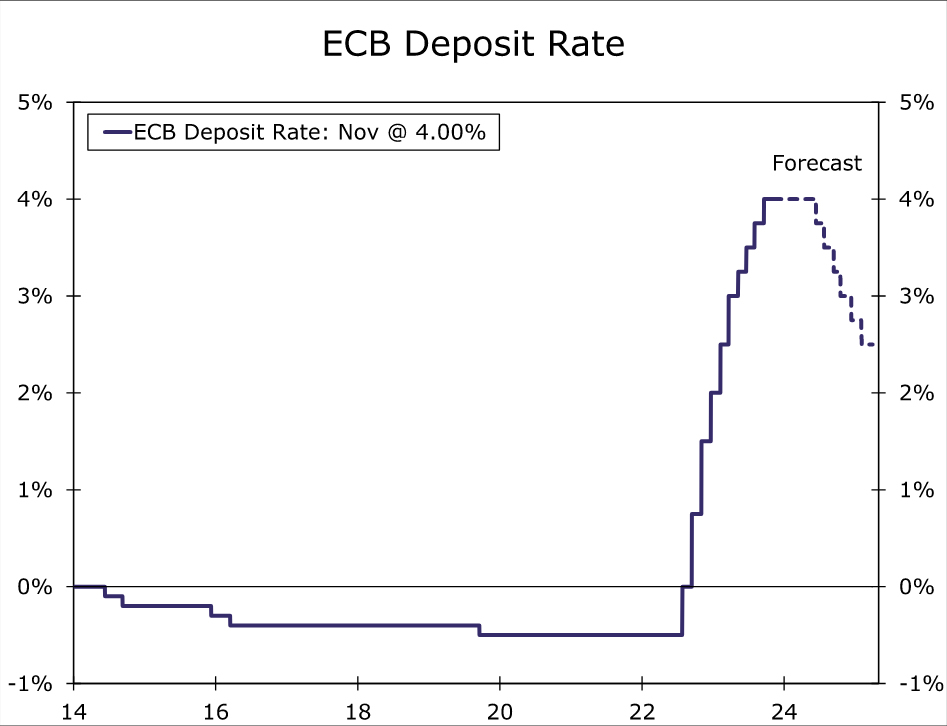

- Against that backdrop, we do not forecast an initial ECB rate cut until the June 2024 meeting, although a steady series of rate cuts after that should see the ECB lower its Deposit Rate by a cumulative 150 bps to 2.50% between mid 2024 and early 2025. Overall, we view the risks as skewed toward the ECB lowering interest rates earlier, or more aggressively, than generally expected.

Eurozone Economy Delivers Disappointing Data

Eurozone economic data have been broadly downbeat in recent months, a trend capped by the region’s third quarter GDP report. Q3 GDP surprised to the downside, dipping 0.1% quarter-over-quarter, although an upward revision to Q2 GDP provided a partial offset. Growth in the region’s largest economies was subdued, as German GDP fell 0.1%, Italian GDP was flat and French GDP edged up just 0.1%. With recent activity and survey data remaining soft, the natural question to ask is whether the Eurozone is on the cusp of—or perhaps already in—recession. In this report we take a look at updated consumer and business fundamentals to offer some perspectives on those questions.

Consumer Slowdown May Be Passing The Worst

One notable area of weakness has been consumer spending, which has declined by a cumulative 0.6% in the three quarters through Q2-2024, the latest quarter for which full data are available. Moreover, the indications for third quarter spending are not encouraging. Retail sales fell in both June and July, and the average level of sales for the July-August period is down 0.6% compared to Q2. That said, we believe the worst of the consumer slowdown may be coming to an end. As headline inflation has receded, real household disposable income has returned to positive territory during this first half of this year. For Q2, real household disposable income rose 1.4% year-over-year, outpacing the 0.4% year-over-year increase in real consumer spending.

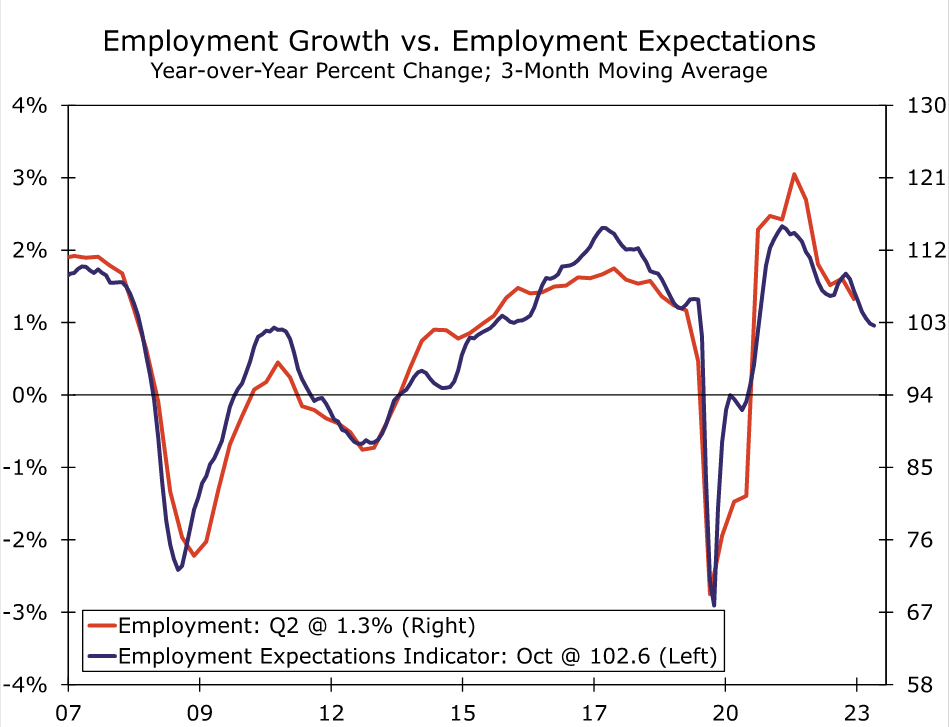

Our outlook is for growth in real household incomes to continue, and perhaps strengthen slightly further, through the rest of 2023 and into 2024. We see continued employment growth, though perhaps at a somewhat more gradual pace than recently. We note that while the European Commission’s Employment Expectations Indicator (EEI) has softened, it has held up better than the broader Economic Sentiment Indicator. Indeed, the EEI remains above its long-term average from 2000 to 2022, and its October reading of 102.8 is historically consistent with employment growth of around 1% per year. With labor costs still growing by around 4.5%-5.5% and with inflation likely to decelerate somewhat further, we anticipate some further firming in real income growth going forward. We also note the household saving rate rose to 14.9% of disposable income in Q2, and remains moderately above pre-pandemic levels, providing Eurozone consumers some capacity to spend. Finally, we observe that household interest costs have risen only moderately over the past several quarters, to 2.1% of household disposable income by Q2-2023. Overall, while we don’t necessarily envisage a sharp rebound, these moderately favorable household finance fundamentals should, in our opinion, prevent a significant further decline in consumer spending.

Business Outlook Gradually Softening

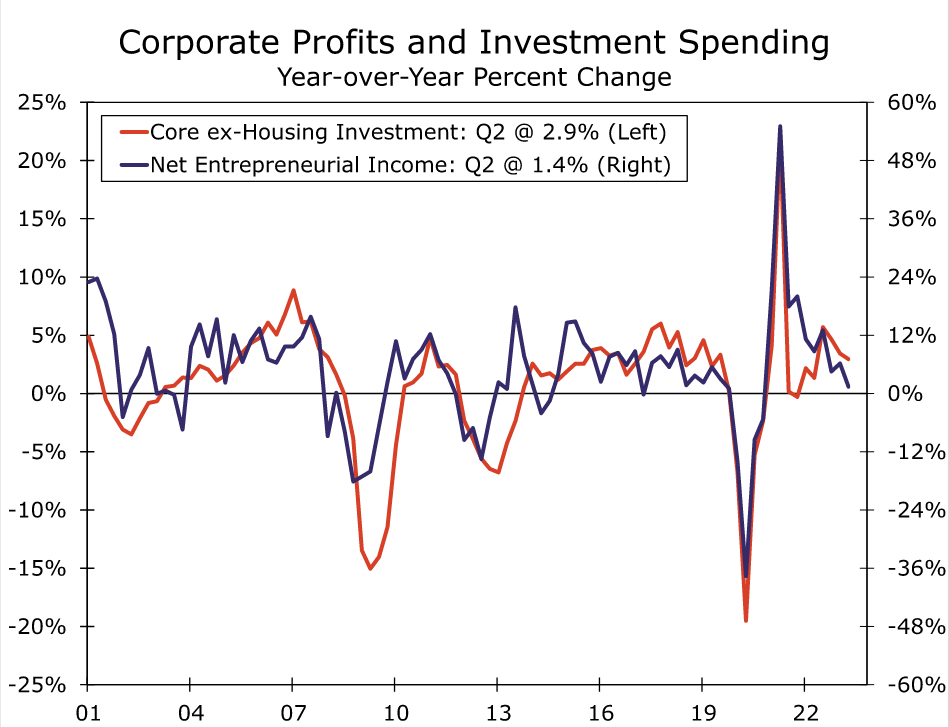

While we believe the consumer outlook may be passing the worst, we see potential for a moderate further weakening in the business outlook across the Eurozone and, as a result, possible weakness in investment spending in the quarters ahead. Eurozone corporate profits have held up reasonably well so far, but are showing signs of softening. Net Entrepreneurial Income (which, according to Eurostat, broadly approximates pre-tax corporate profits) grew 1.4% year-over-year in Q2-2023, the latest available data. On the positive side, corporate profits have not shown an outright decline so far, though on the more negative side, profit growth has slowed noticeably over the past year.

How might these gradually worsening trends for Eurozone businesses affect employment growth and investment spending? As we highlighted above, the gradually softening in business environment has led to only a moderate slowdown in employment growth. We expect job gains can continue in the quarters ahead, albeit at a slower pace than recently.

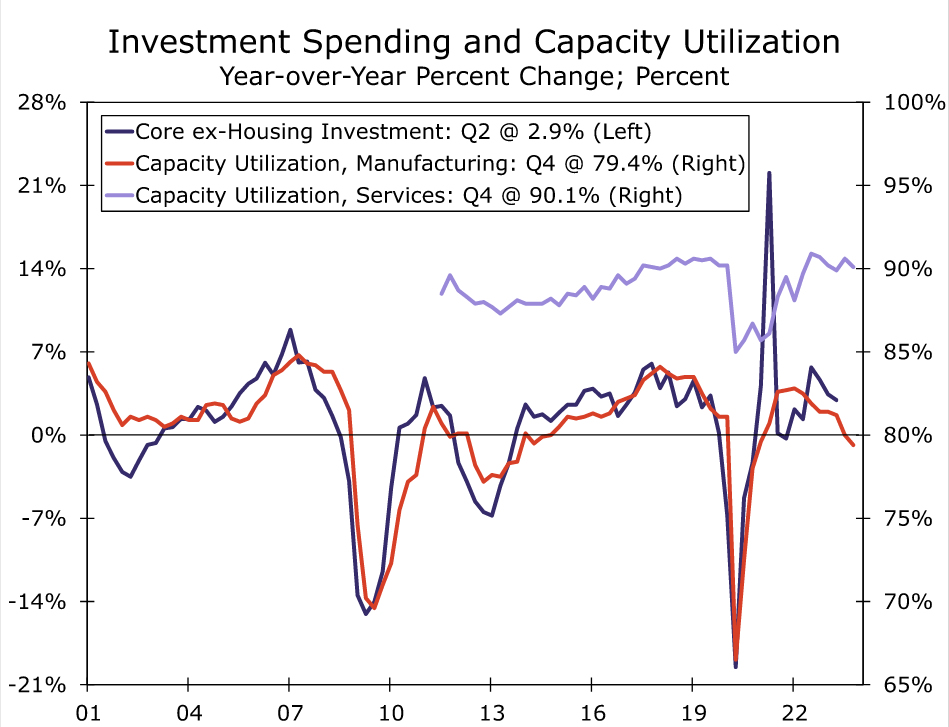

With respect to investment spending, we believe a range of recent indicators point to some decline in investment spending in the quarters ahead. For the Eurozone, a precise measure of business fixed investment is not readily available. We can, however, estimate a measure that broadly approximates that metric, and for which we believe investment cycles are broadly similar. Specifically, we calculate Eurozone investment spending excluding dwellings (or housing) investment and excluding intellectual property products. We exclude dwellings on the basis that it is clearly related to households and not businesses. While spending on intellectual property products is clearly relevant for business investment, it is also a particularly volatile series, and its removal allows for a clearer sense of underlying investment trends. Fortunately our estimated metric, which we define as “Core ex-Housing Investment”, shows a similar but less volatile cycle than overall Eurozone investment spending. While growth in core ex-housing investment has slowed, it was still up 2.9% year-over-year in Q2-2023. That said, trends in Eurozone net entrepreneurial income (or corporate profits) point to a further slowdown in core ex-housing investment ahead. Historically, Eurozone profit growth and investment growth cycles have followed reasonably similar patterns, and thus the slower growth in corporate profits also portends a downturn in investment spending. That would especially be the case if Eurozone profit growth turns negative, which is clearly a distinct possibility.

We also see some other indicators than reinforce the outlook for an investment spending slowdown. In particular, Eurozone capacity utilization measures have fallen in recent quarters, a trend that would suggest a slowdown in investment spending. That decline in capacity utilization has been most evident in the manufacturing sector, from 82.8% in Q1-2022 to 79.4% by Q4-2023. Historically, a capacity utilization rate of below 80% for manufacturing has been consistent with declining core ex-housing investment for the Eurozone. Capacity utilization in the service sector has also softened, though only slightly, from 90.9% in Q3-2022 to 90.1% by Q4-2023. Finally, Eurozone bank lending to non-financial corporates slowed to just 0.2% year-over-year in September, also an indirect indicator of slower investment spending ahead.

Overall the mixed outlook for consumer and investment spending leaves the Eurozone very close to recession, and largely dependent on whether the improvement in consumer spending transpires more quickly than any investment spending slowdown. Among the indicators we will be monitoring most closely are monthly retail sales and quarterly corporate profits and capacity utilization. Moreover, while we are not calling for Eurozone recession just yet, should the Eurozone PMI surveys stay at their current contractionary levels in the months ahead or soften further, an economic downturn may eventually become unavoidable.

Eurozone Rate Hikes Are Done, Monetary Easing Still Some Way Off

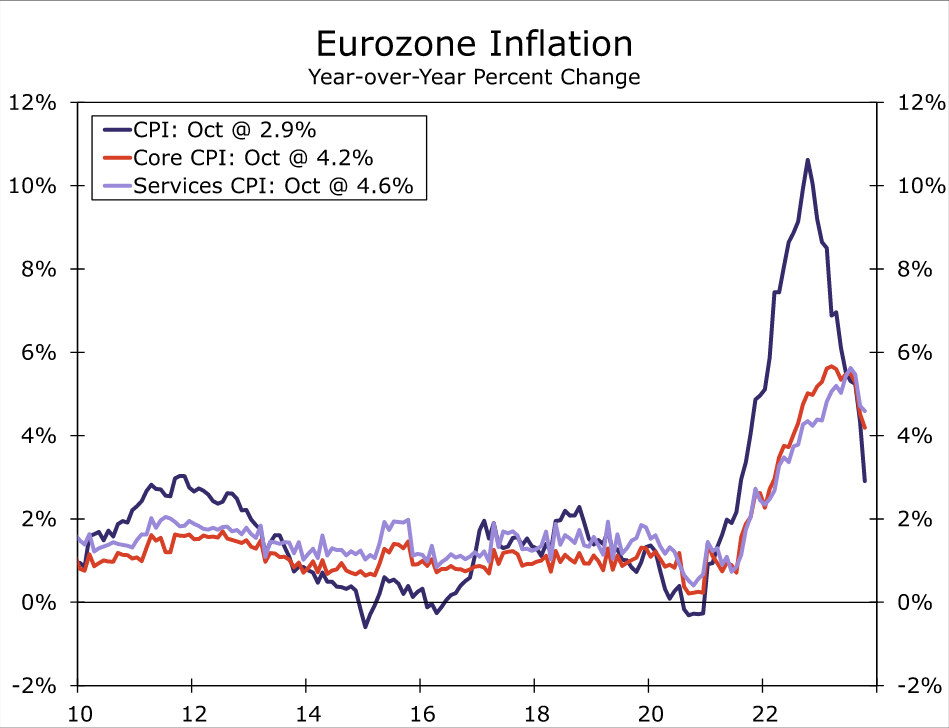

Regardless of whether the Eurozone falls into recession, we see enough growth headwinds to suggest that the European Central Bank’s (ECB) monetary tightening is done. At its October announcement, the ECB held Deposit Rate at 4.00% and repeated that interest rates are at levels that if “maintained for a sufficiently long duration, will make a substantial contribution” to returning inflation to its 2% target in a timely manner. The most recent progress on the inflation front reinforces the outlook that a peak in policy interest rates has already been reached. The Eurozone October CPI slowed sharply 2.9% year-over-year, while there was also a moderate deceleration in core inflation and services inflation to 4.2% and 4.6%, respectively. The improvement in inflation trends when measured on a three-month annualized basis is even more noteworthy. Service sector inflation slowed to a 3.5% annualized pace in the three months to October, while the CPI excluding food and energy rose at a 2.3% annualized pace—the slowest rate of increase for this metric since June 2021.

Despite these encouraging trends, we believe it is too early for the ECB to sound the “all clear” on the inflation front and, accordingly, too early for the central bank to consider rate cuts just yet. Even on the three-month annualized measures, inflation remain a bit above the ECB’s 2% inflation target. Moreover, it’s not yet clear whether the October outcome reflects a temporary inflation reprieve, or the start of a more sustained downtrend. We expect three-month annualized inflation would need to slow closer to 2%, and remain in that region for several months, before the European Central Bank becomes comfortable enough to embark upon a rate cut cycle. For that reason, and even with an underwhelming growth outlook, we currently do not forecast an initial ECB rate cut until the June 2024 meeting. That is slightly earlier than the consensus forecast of economists, which envisages an initial rate cut at the September 2024 meeting, and broadly in line with the timing implied by market pricing.

While the view the risks around our base case as relatively balanced, we certainly wouldn’t rule out an initial rate cut coming even earlier than June next year. Given the progress on inflation so far and if the Eurozone does indeed fall into recession, we could envisage an initial rate cut as early as the April 2024 meeting. In addition, considering the underwhelming Eurozone economic outlook, we believe the ECB will be inclined to deliver a steady series of rate cuts once it is comfortable that inflation is under control. Accordingly, our base case is for the ECB to lower its Deposit rate by a cumulative 150 bps to 2.50% between Q2-2024 and Q1-2025. Overall our main takeaway is that, relative to the consensus economist forecast or market implied pricing, we believe the risks are tilted toward the ECB lowering interest rates earlier, or more aggressively, than generally expected.

since early 2013. With recent activity and survey data remaining soft, the natural question to ask is whether the Eurozone is on the cusp of, or perhaps already in, recession.){kind=link}