- Dollar slides as investors pencil in 100bps worth of Fed rate cuts

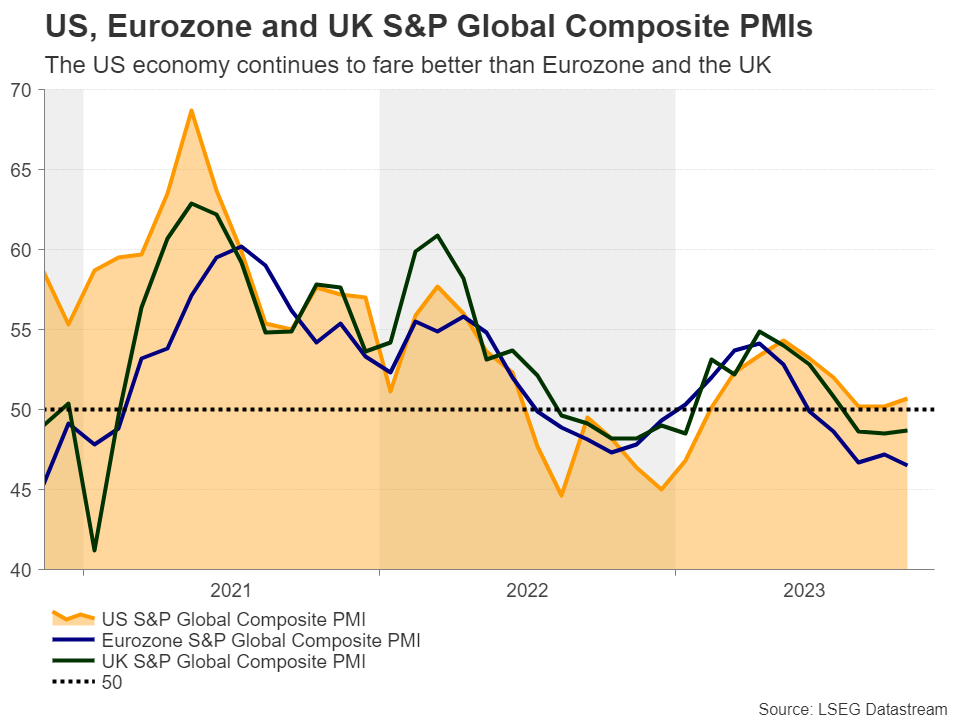

- US economy is expected to slow, but still fare better than its major peers

- Fed likely to begin rate reductions next year, but ECB may cut earlier

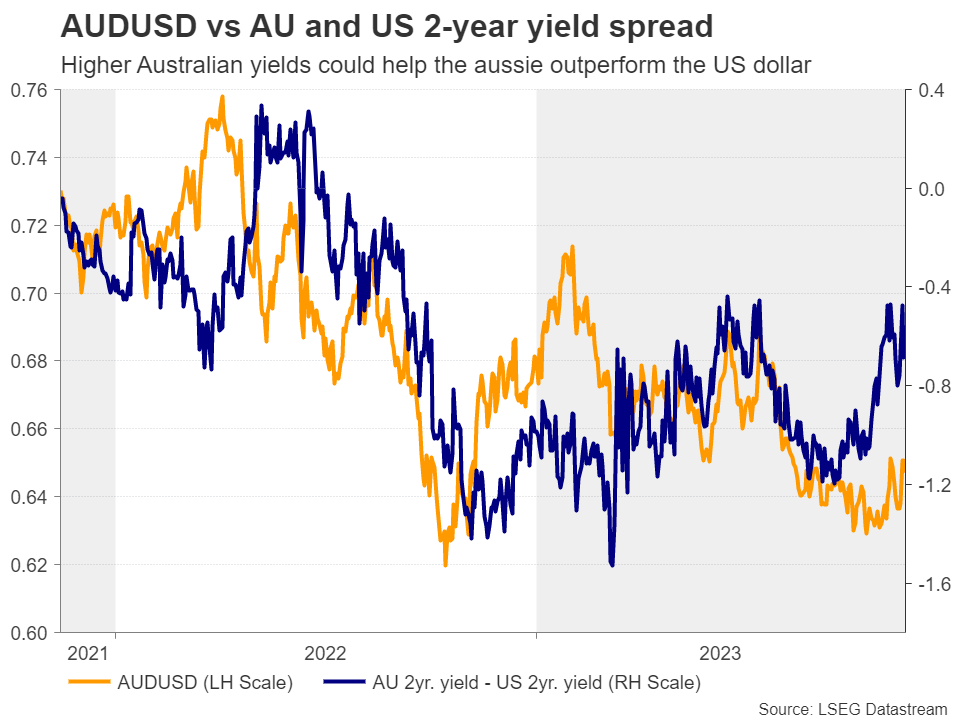

- Aussie the most likely candidate to outperform the greenback

Jobs and inflation data hurt the dollar

The US dollar suffered a major blow this week after the US CPI data revealed that inflation cooled by more than anticipated in October, adding credence to investors’ view that the end credits of the Fed’s tightening crusade have already rolled, despite Chair Powell and several of his colleagues pushing back against such expectations recently.

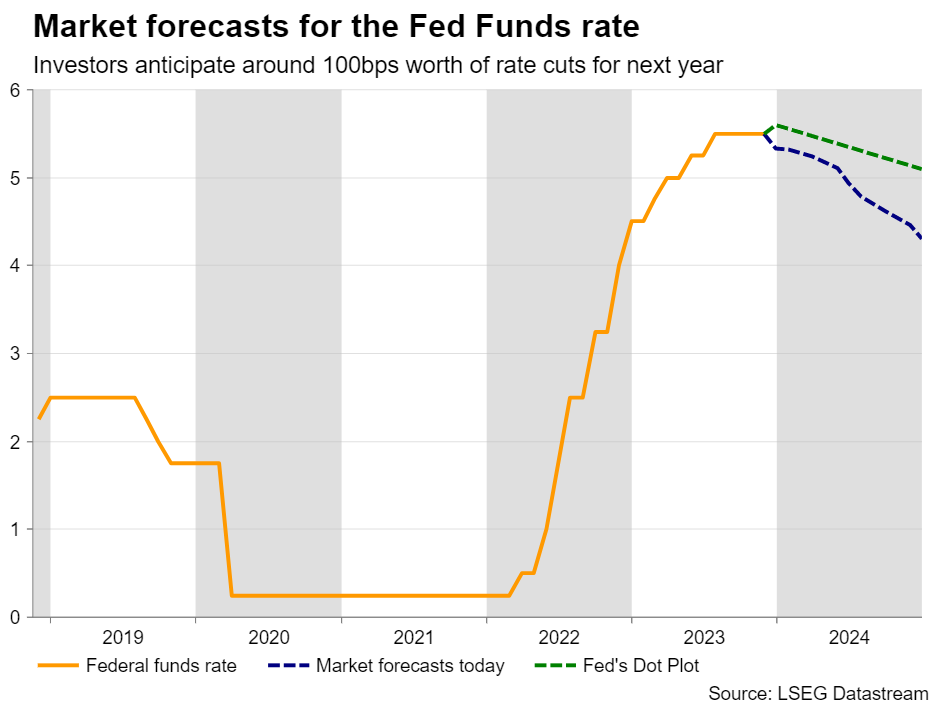

This was the second hit in less than two weeks for the US dollar, with the first one coming after the disappointing jobs report for the same month. Bearing in mind that the Fed is linking its monetary policy decisions to both inflation and the labor market, easing conditions on both fronts prompted market participants to price out any chance for another hike this year and to pencil in around 100bps worth of rate reductions for next year.

Fed to cut in 2024; but by how much?

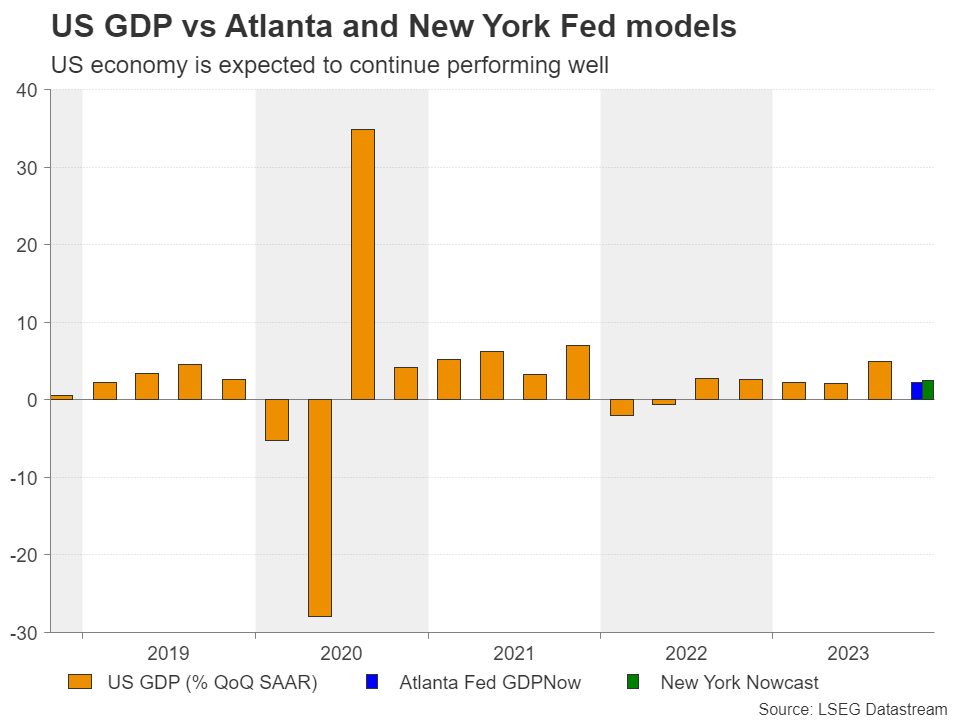

Nonetheless, there is no evidence yet supporting so many basis points worth of cuts for next year. Yes, the US economy is expected to have slowed in Q4, with the Atlanta Fed GDPNow and the New York Fed Nowcast models projecting growth rates of 2.2% and 2.5% respectively, but with interest rates at such high levels and the economy growing at the astounding pace of 4.9% in Q3, such a slowdown appears quite normal.

On the other hand, the Fed could start cutting rates and monetary policy would still stay tight, pushing inflation in the right direction. So, should data continue to suggest that inflation is drifting south faster than anticipated, then the Fed may be tempted to start cutting sooner than it currently anticipates, in order to avoid a more severe than forecast economic slowdown.

According to its September dot plot, the Committee is projecting one more hike and expects interest rates to end 2024 within the 5.00-5.25% range. In other words, it anticipates only 50bps worth cuts for next year, which is a decent deviation from what the market is currently pricing in. Therefore, the big question moving forward is: Who is right? The market or the Fed?

US economy seen slowing, but 100bps cuts not justified

The Fed’s own economic forecasts suggest that the economy could slow to 1.5% growth in 2024 and then reaccelerate to 1.8% in 2025, with inflation easing to 2.2% by the end of 2025 and hitting the 2% objective in 2025. Indeed, such projections do not justify 100bps worth of rate cuts and should incoming data continue to point to a US economy that is faring better than its major peers, investors may be eventually convinced to lift their implied path. Even if new rate hike bets do not resurface, market participants could scale back a decent amount of basis points worth of cuts, which could prove positive for long-dated Treasury yields, and thereby help the dollar rebound.

Although traders currently appear willing to sell the dollar more aggressively on anything confirming the ‘no more hikes’ narrative than on anything corroborating the Fed’s ‘higher for longer’ mantra, there is nothing suggesting that a bearish reversal is imminent. The Eurozone seems to be headed for its own recession, which could eventually prompt the ECB to start cutting its own rates before the Fed does. The UK economy is also in a bad shape and following the larger-than-expected slowdown in UK inflation during October and disappointing growth-related data, investors may be tempted to continue bringing forward their BoE cut bets. This could happen despite Governor Bailey arguing that it is too early to be thinking about rate cuts. Such thinking by investors is likely to leave the euro and the pound in a vulnerable position for a while longer.

Dollar could struggle against aussie, kiwi, and yen

Currencies that have more chances in outperforming the dollar may be the risk-linked aussie and kiwi, as expectations of several rate cuts by the Fed have already been translated to increasing risk appetite, as made evident by the latest rally in Wall Street. What’s more, with investors not even pricing in a full 25bps cut by the RBA in 2024, the aussie could perform even better. That said, this may be a story for next year, when the Fed begins to cut rates and the slide in short-dated Treasury yields accelerates. The yen could also perform better than it did this year if the BoJ abandons its yield curve control (YCC) policy, although improving risk appetite is usually not a plus for this currency.

{kind=link}