Summary

- We look for the FOMC to keep rates on hold at its December 13 meeting, an expectation that is universally shared. If realized, the third consecutive hold would suggest that, rather than the FOMC merely hiking at a slower pace, the fed funds rate probably has reached its terminal level of this cycle.

- Both sides of the Fed’s mandate are moving toward their longer-run estimated levels. The labor market is becoming less tight, and inflation continues to recede.

- That said, inflation has not yet receded all the way back to 2%. Consequently, we expect the post-meeting statement will keep the door open to the possibility of additional tightening this cycle. However, while the statement likely will indicate that further tightening remains possible, we would not be surprised for it to hint that another rate hike is less probable.

- A more benign inflation outlook is the key to what we believe will be a flat-to-modestly-lower “dot plot” in the Summary of Economic Projections released at the conclusion of the meeting on December 13. We expect that the median dot for year-end 2024 will shift down from 5.125% in the September SEP to 4.875%. For 2025 and beyond, we suspect the median dots will be more or less unchanged.

- We look for the FOMC to maintain its current pace of balance sheet runoff (i.e., quantitative tightening).

It Appears That This Tightening Cycle Has Come to an End

Since the summer, the FOMC has been keeping its options open regarding the possibility of additional rate hikes. However, recent economic data and comments suggest less need and desire to exercise that option. We see the Committee leaving the fed funds target range at its current level of 5.25-5.50% at the conclusion of its upcoming meeting on December 13. If realized, the third consecutive hold would suggest that, rather than the FOMC merely hiking at a slower pace, the fed funds rate probably has reached its terminal level of this cycle. With the Committee seeming to settle into a prolonged hold, the conversation around the future policy path will shift toward when—and under what circumstances—the FOMC eventually cuts rates.

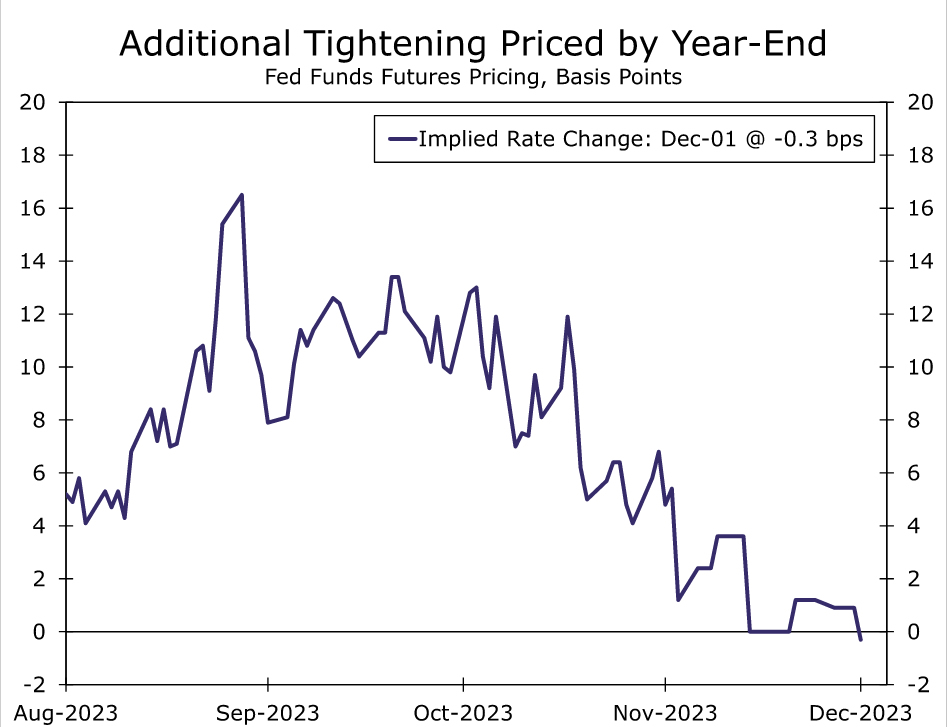

We have maintained since the FOMC last raised the fed funds rate at its July 26 meeting that the increase was likely the last of this hiking cycle, a view not always shared by market participants. As recently as October, market pricing suggested that another 25 bps hike was slightly more likely than not, a bet bolstered in part by Committee members’ own projections in September. Yet over the past two months, market pricing for an additional hike before year-end has fallen close to zero (Figure 1).

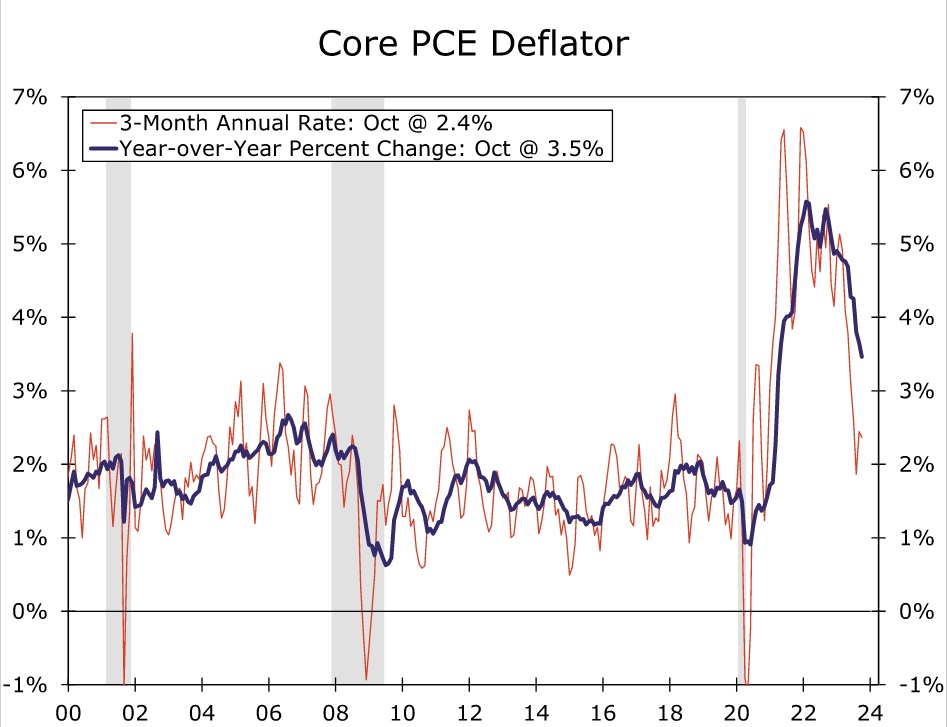

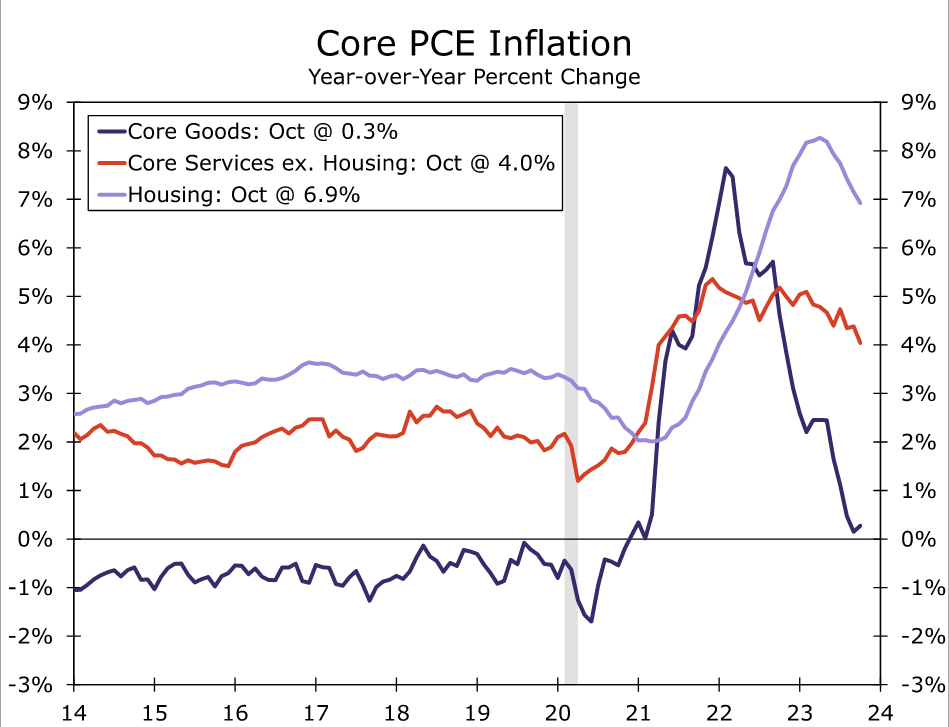

The declining odds of one additional hike this year come as both sides of the Fed’s mandate are moving toward their longer-run desired levels. Notably, inflation has made encouraging progress toward returning to the FOMC’s 2% target. In October, core PCE inflation, the Fed’s preferred benchmark for price growth, fell to 3.5% year-over-year, nearly a two-and-a-half-year low. The latest monthly readings suggest the recent pace has downshifted even further, with core prices in October up at an annualized rate of only 2.4% relative to July (Figure 2). All major categories frequently highlighted by FOMC members have contributed to the slowdown: core goods prices are nearly flat relative to a year ago, housing inflation has rolled over and even “super core” inflation (core services less housing) has come off its recent peak (Figure 3). In addition to softer core inflation, lower energy prices and more modest increases in food costs have helped drive the year-over-year rate of the headline PCE deflator down to the lowest rate since early 2021.

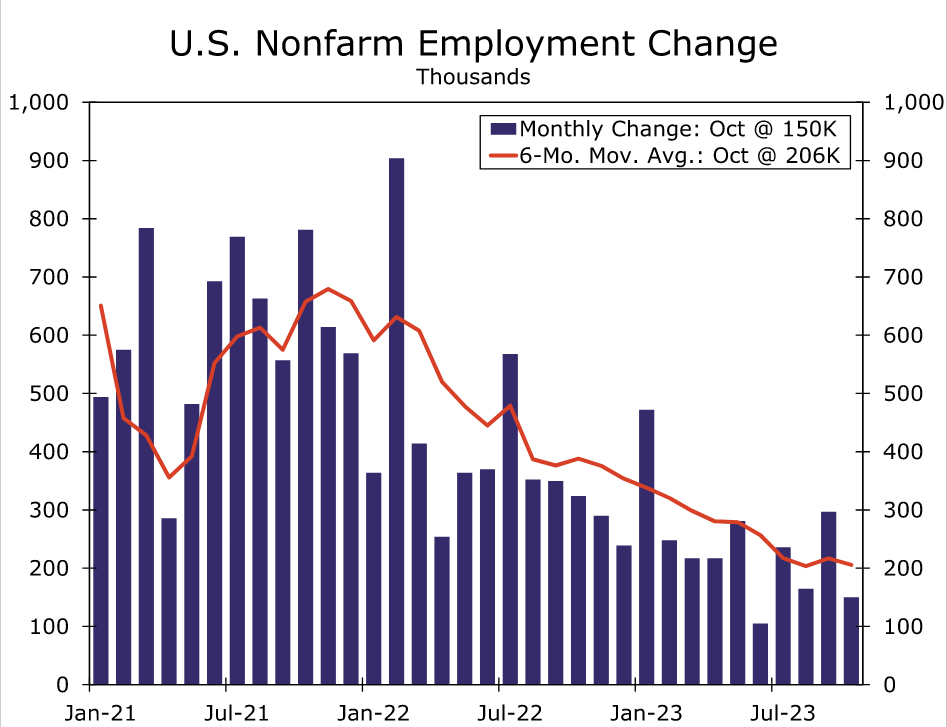

Meantime, the labor market is showing clearer signs of cooling. The share of workers quitting their job is essentially back to pre-COVID levels, which, along with strong growth in the labor supply, has helped to reduce upward pressure on wages. Layoffs remain low, but continuing jobless claims have crept higher in a sign that it is taking displaced workers longer to find new employment. The FOMC will get one more key read on the labor market before its upcoming meeting with the November jobs report to be released on December 8. Although we expect to see a pickup in payroll growth thanks to the conclusions of the United Autoworkers and Hollywood strikes, the overall trend in hiring has downshifted since earlier in the year (Figure 4), while the unemployment rate has drifted up from 3.4% in April to 3.9% in October.

Yet, while inflation is progressing back toward target, it has not yet arrived at 2%. At the same time, financial conditions have eased since the FOMC’s last meeting, only partly due to adjusted expectations for the Fed’s policy path, in our view. Therefore, we expect the post-meeting statement will keep the door open to the possibility of additional tightening this cycle.

However, while the statement likely will indicate that further tightening remains possible, we would not be surprised for it to hint that another rate hike is less probable. A modestly more dovish outlook could be relayed through adjusting the current statement that “In determining the extent of additional policy firming that may be appropriate…” to verbiage indicating that the risks to the outlook, and therefore the policy path, are becoming more balanced. A slightly less-constructive assessment of recent economic conditions could also suggest that the Committee views additional tightening as less necessary ahead.

SEP: Slower Inflation = Lower Dots?

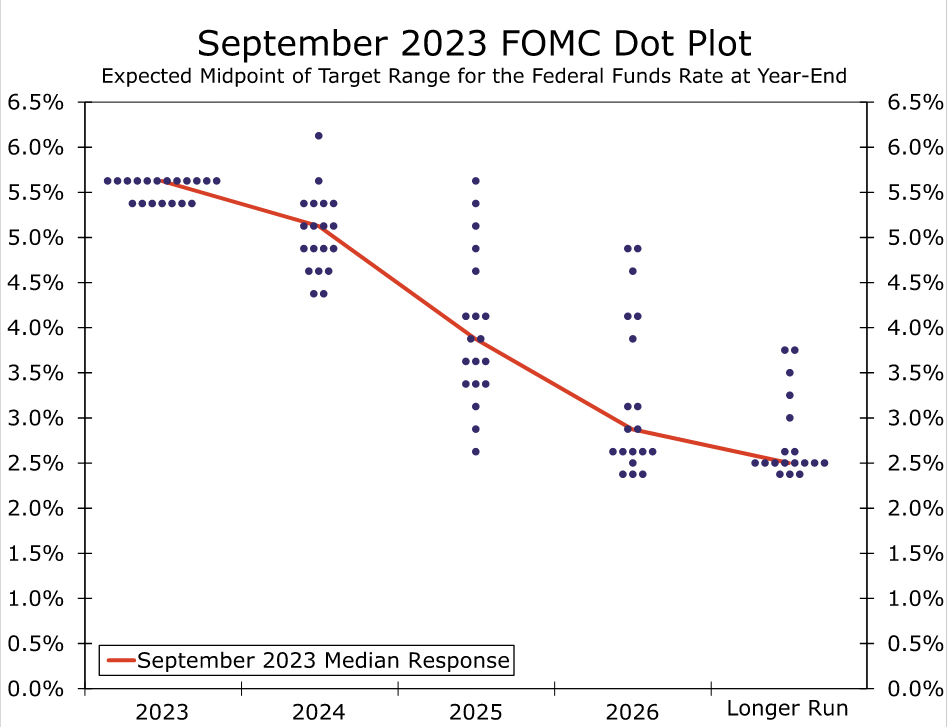

The December FOMC meeting will include an update to the Committee’s Summary of Economic Projections (SEP). The last SEP, which was published in September, implied one more 25 bps increase in the target range for the federal funds rate by year-end 2023. Barring a rate hike on December 13, which would come as a major surprise to the vast majority of market participants, the median dot for 2023 will come down to 5.375%, the midpoint of the current target range for the federal funds rate. The September dot plot contained a median projection of 5.125% for the federal funds rate at year-end 2024 (Figure 5). However, the distribution of the 2024 dots was skewed to the downside, with nine submissions below 5.125% and only six above. Given this distribution, and given that inflation has continued to recede faster than the Committee anticipated in September, we expect the median 2024 dot will decline 25 bps to 4.875%. For 2025 and beyond, we suspect the median dots will be more or less unchanged. The distribution of dots for the “longer-run” has an upward bias, and it would not take much to move the median up from its current 2.5%, where it has been since the pandemic began. We have no compelling reason to think an upward revision is coming in December, but the skew and ongoing debate about r-star (i.e., the “equilibrium” real interest rate) suggest that this is something to keep an eye on going forward.

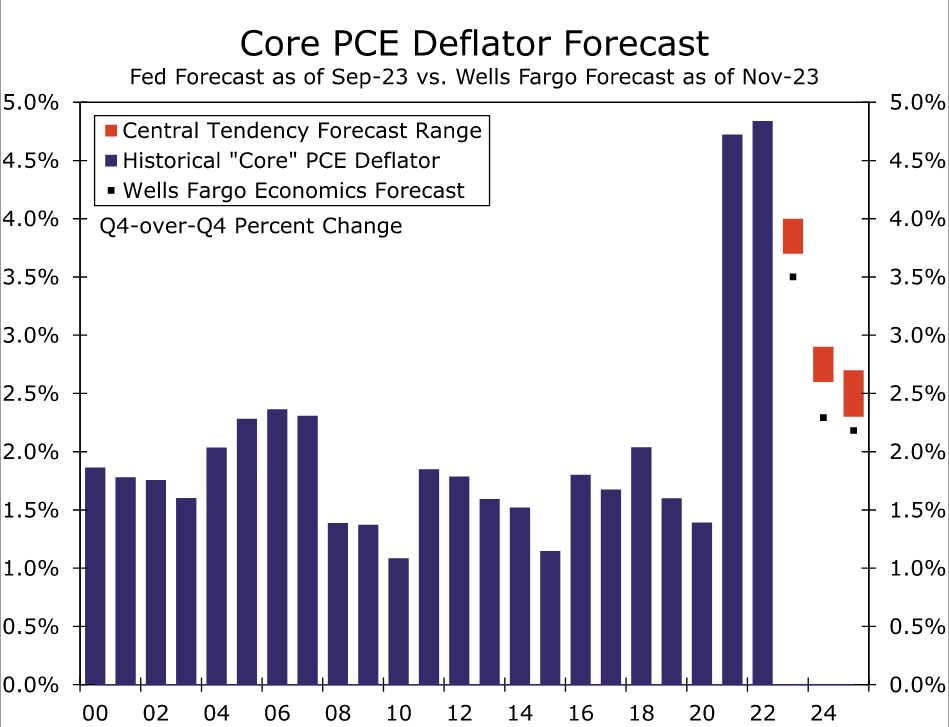

A more benign inflation outlook is the key to a flat-to-modestly-lower dot plot. In September, the FOMC’s median inflation projections declined for the first time since 2020. The median submission for core PCE inflation in 2023 fell from 3.9% in June to 3.7% in September. We expect a similar downward revision in the December SEP, as our current forecast for core PCE inflation is 3.5% year-over-year in Q4-2023 (Figure 6). The median projection for headline PCE inflation for 2023 should also fall a few tenths-of-a-percentage point on the back of lower energy prices. For 2024, we think the median inflation forecast may fall a tenth-of-a-percentage point or so, but probably not much more than that. We doubt the FOMC will want to signal an overly optimistic 2024 inflation outlook even with the recent progress.

Real GDP growth projections for 2023 are poised for another upward revision. As recently as June, the median Committee participant expected just 1.0% real GDP growth this year. This estimate was upwardly revised to 2.1% in the September SEP, and another notch higher to 2.5% or so seems likely at the December meeting. We would not be surprised if the Committee’s median projection for economic growth in 2024, currently 1.5%, falls slightly to account for a higher base comparison after the faster-than-expected growth in recent months. Accordingly, the median projections for the unemployment rate in 2024 and 2025 may rise by a tick or two but likely will remain close to the longer-run projection of 4.0%.

Quantitative Tightening: Full Steam Ahead

We also expect the FOMC to once again reaffirm its ongoing quantitative tightening (QT) program. The FOMC is currently allowing up to $60 billion of Treasury securities and $35 billion of mortgage-backed securities to roll off of its balance sheet each month. This passive runoff has reduced the size of the Fed’s balance sheet from a peak of nearly $9 trillion in Q2-2022 to roughly $7.8 trillion today, and so far there have been few signs of bank reserves becoming scarce. The effective federal funds rate remains comfortably within the FOMC’s target range, and other key benchmark rates, such as the Secured Overnight Financing Rate (SOFR), have been relatively stable. As a result, the FOMC likely will reaffirm its intention to continue QT into 2024. We analyzed the outlook for the Fed’s balance sheet in 2024 and beyond in a recent special report, which can be found here.

{kind=link}