- Chinese stock markets sink to lowest levels in five years

- Real estate crisis and other problems haunt investors

- Valuations are cheap, but more is needed for lasting recovery

Chinese equities implode

It’s been a tough few years for Chinese stock markets. Shares in mainland China have fallen to their lowest levels since 2019 as investors continue to liquidate their positions, despite a series of stimulus measures by Beijing that were meant to stop the bleeding.

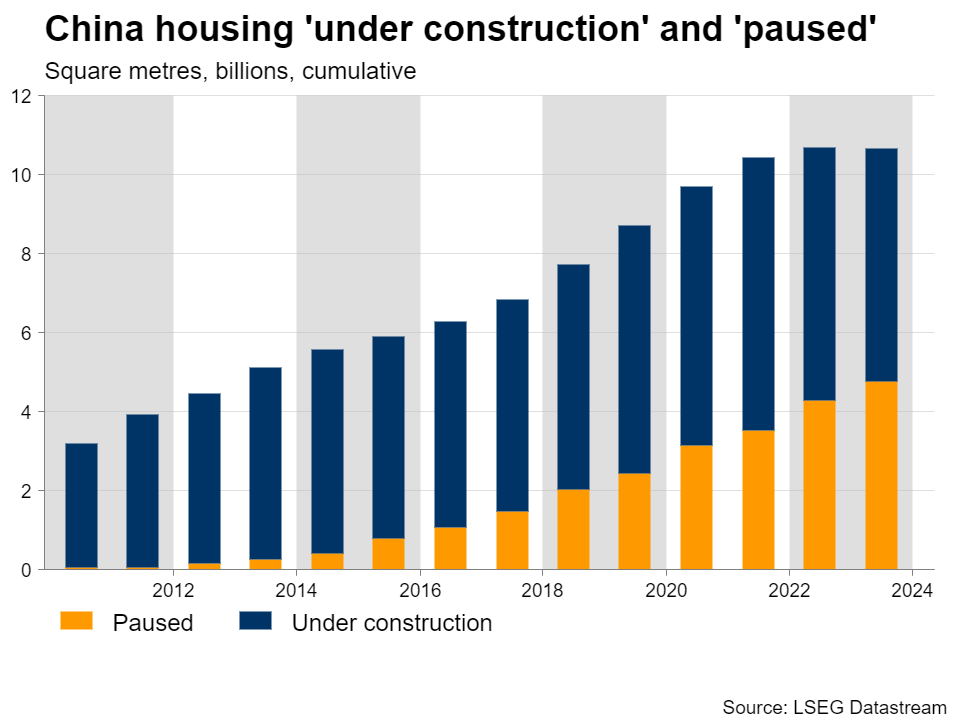

An ongoing crisis in the property sector, a slowdown in global manufacturing, and high youth unemployment have joined forces to hamstring growth, pushing the Chinese economy into deflation. Deteriorating trade relations with the United States have made matters worse, fueling concerns that China is headed for a ‘lost decade’.

In the past, the solution to similar problems was to stimulate the economy, by encouraging local governments and businesses to take on debt and invest in infrastructure projects. Alas, the same trick won’t work this time, as the property sector is already dealing with the toxic aftermath of decades of malinvestment and overinvestment.

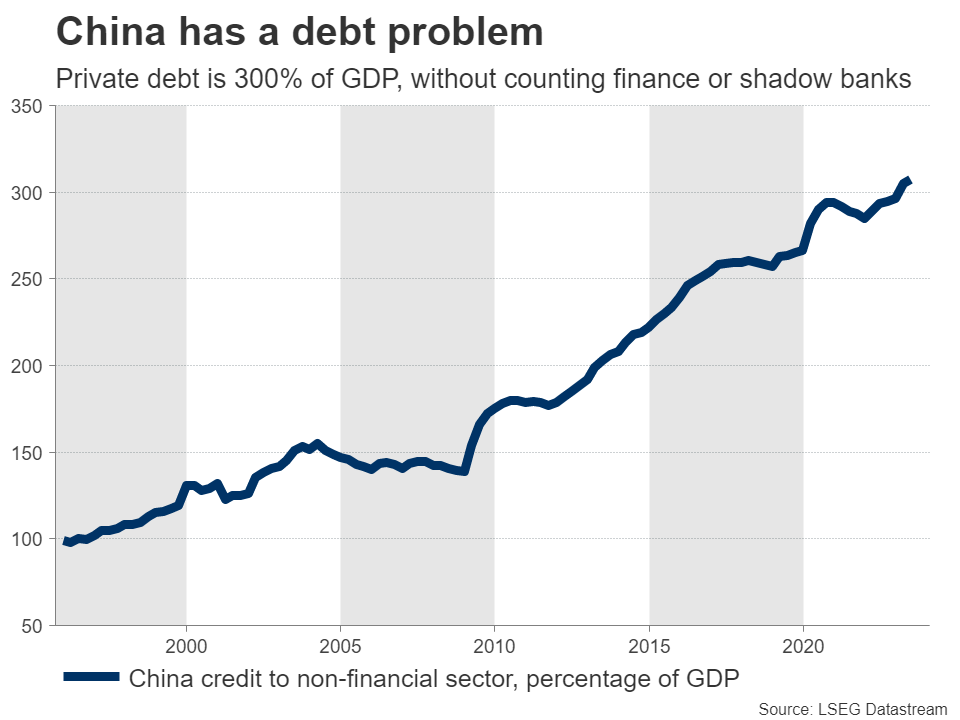

Another issue is that the scope for stimulus measures is limited. Debt in the private sector has skyrocketed to reach 300% of GDP, and that’s without even counting debts of financial institutions or shadow banks. Chinese authorities want to avoid a further increase in debt levels, as that could destabilize the financial system and lead to a deeper crisis.

For similar reasons, the central bank has not slashed interest rates in a meaningful way.

So far, measures have not been enough

Unable to flood the economy with debt-fueled stimulus, Beijing has taken a more cautious approach, announcing a series of piecemeal measures that appear insufficient to turn the tide.

The latest steps include a reduction in the cash that banks must hold in reserve. This is estimated to free up 1 trillion yuan that can be used for lending, which equals nearly 140 billion dollars. In tandem, the government said it will expand access to loans for struggling property developers, to restore confidence in a sector mired in bankruptcy.

But for the most part, authorities have focused on lifting the stock market. Strict restrictions on short selling have been introduced and recent reports suggest Beijing will deploy about 2 trillion yuan to purchase stocks directly.

Sadly, this rescue package probably lacks the firepower and scope to make a true impact on an economy haunted by plunging investment and depressed consumer sentiment. Throwing money at the stock market could temporarily calm investors, but a lasting recovery will require a turnaround in the real economy.

Valuations are cheap

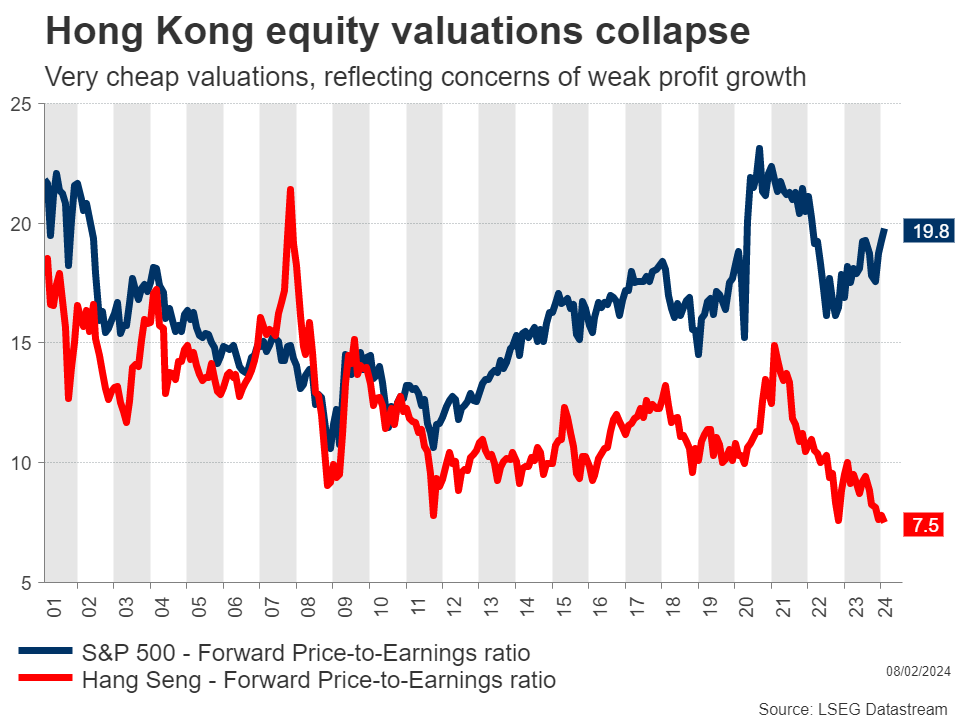

With stock markets getting hammered, valuations have collapsed. For instance, shares listed in Hong Kong are currently trading for only 7.5 times what analysts expect earnings to be over the next year, which is their cheapest valuation in at least two decades. That’s almost three times as cheap as US equities.

These businesses are not heading for bankruptcy. The biggest among them include Alibaba and Tencent, both of which are highly profitable and regularly return cash to shareholders via dividends and buybacks.

Of course, there’s a reason why valuations are so cheap. Weak prospects for future profit growth, sudden regulatory crackdowns, and a general lack of investor protection have eroded confidence in Chinese assets. It’s going to take more than cheap valuations to solve that.

There are several other threats too. Another trade war could ensue if Trump is elected US president in November, as he has already promised new tariffs against China. Not to mention the risk that Beijing might let the yuan depreciate if the economy worsens.

The bottom line

Bearing all this in mind, the outlook for Chinese assets is not very bright. The housing sector will probably need several years to recover, judging by other countries that saw similar property collapses, such as Japan in the 1990s and the United States after 2008. That could restrict growth, especially in the absence of ‘bazooka-style’ stimulus.

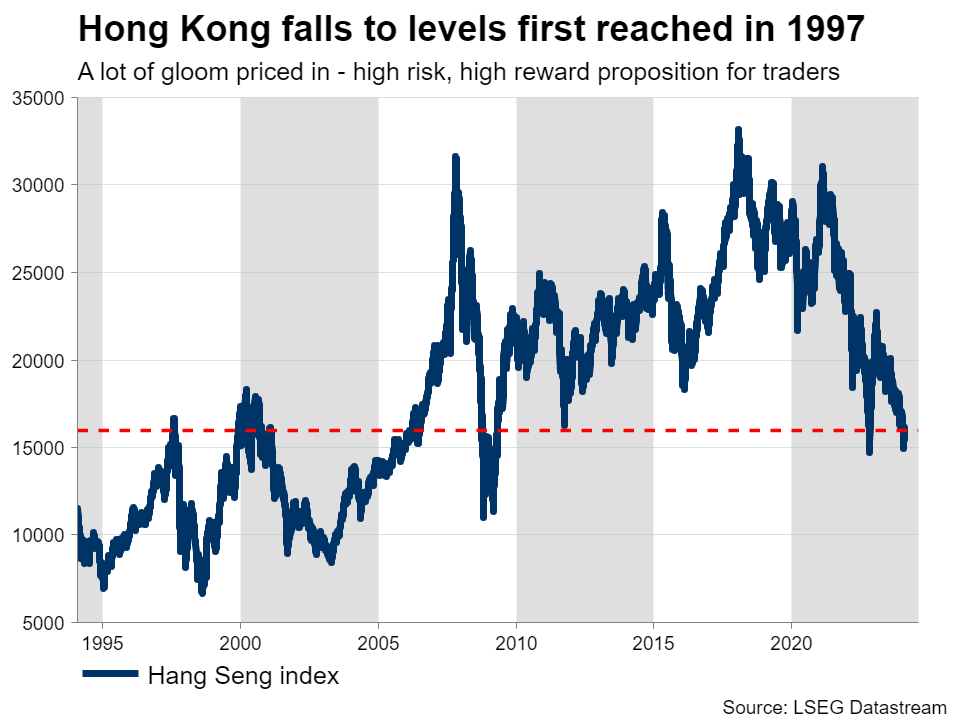

That said, much of this pessimism is already reflected in depressed valuations. With so much gloom priced into Chinese equities, any piece of good news could have a disproportionately large impact. Therefore, Chinese markets offer a high-risk, high-reward proposition for traders.

The middle ground would be to focus on quality businesses. Companies such as Tencent are still growing earnings at a rapid pace, yet their share price has been slammed lower with the rest of the market and their valuations are as cheap as they have ever been.

In other words, shares of quality companies have suffered collateral damage, which might present an opportunity for brave investors. Ultimately though, the road to a sustained stock market recovery will be long and will almost certainly require more forceful steps from Chinese authorities.

{kind=link}