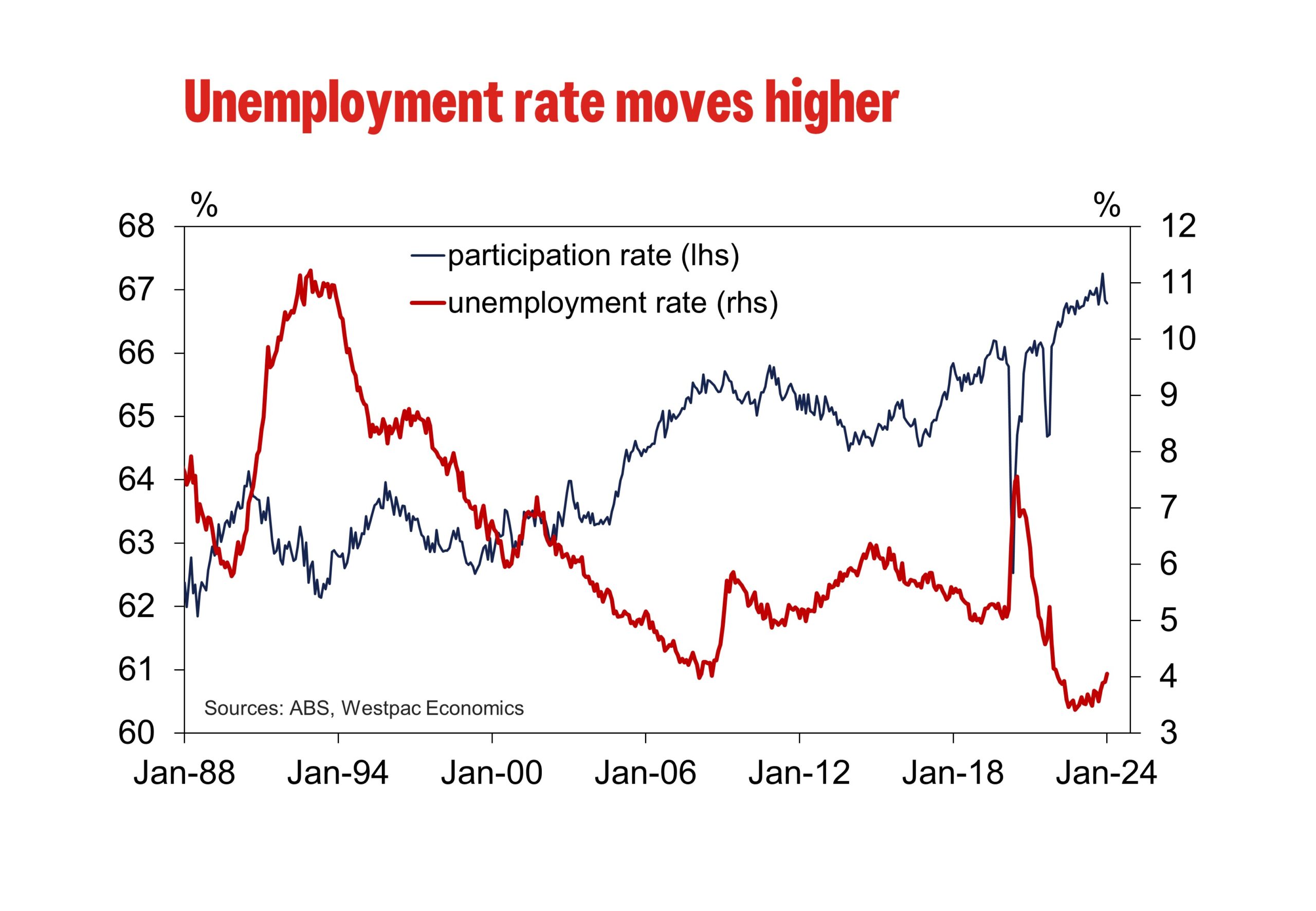

Employment: +0.5k (from –62.7k). Unemployment Rate: 4.1% (from 3.9%). Participation Rate: 66.8% (unchanged).

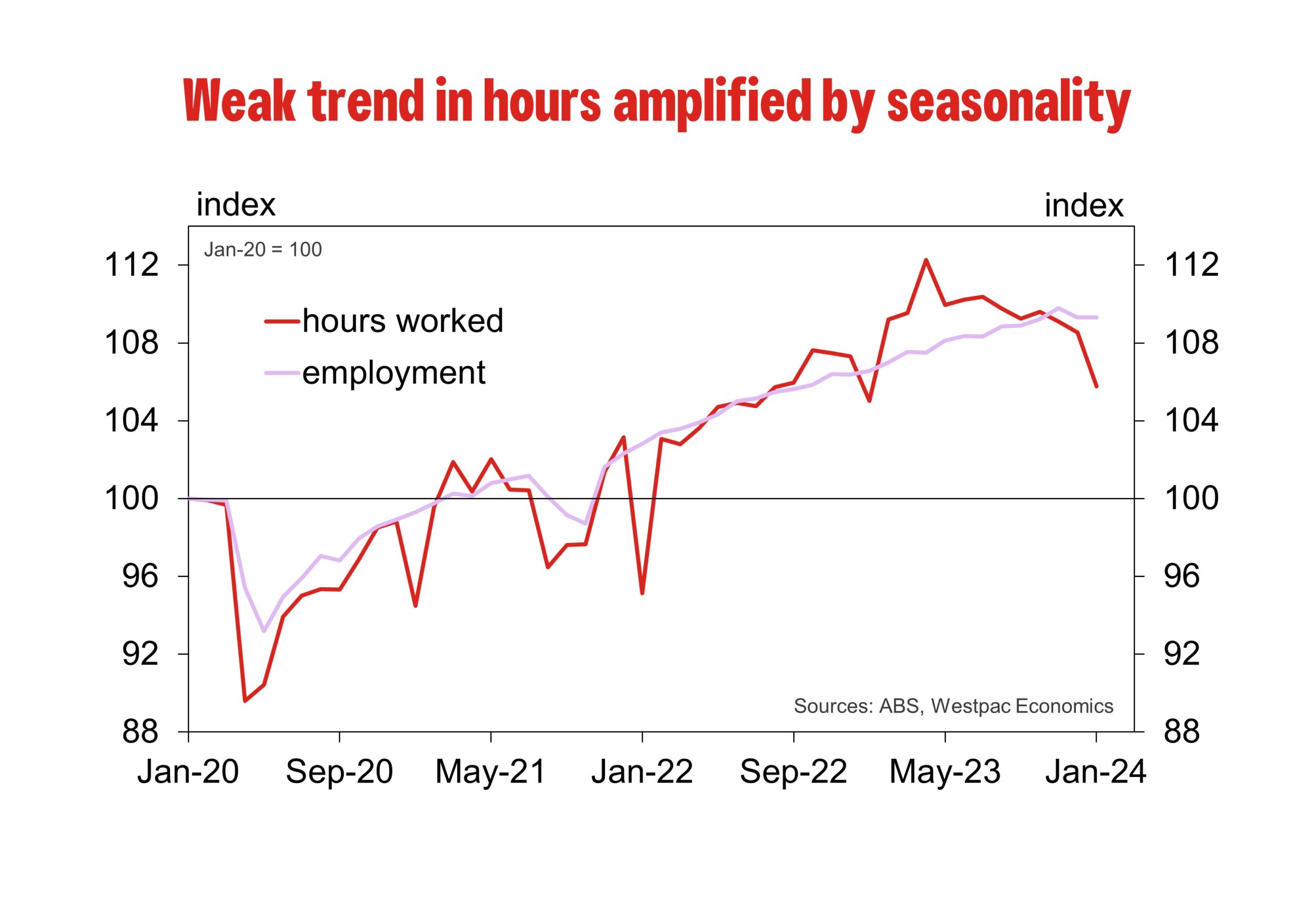

January is the most seasonal time of the year for the labour market, and this year was no exception. As we had anticipated, the softening trend in labour market conditions that extended into the new year was amplified by shifting seasonal dynamics that have become increasingly apparent in the years since the pandemic. The ABS are not yet able to completely remove the influence of these dynamics in its seasonally adjusted estimates, so the results from this month’s survey should be read with caution.

In the media release, the ABS made note of two distinct dynamics which we expected to appear again. Firstly, with regards to hours worked, the ABS noted: “Compared with January surveys before the pandemic, we again saw a higher proportion of employed people working no hours because they were on leave.” This was associated with a 2.5% decline in seasonally adjusted hours worked in January 2024, similar to the 2.3% decline in January 2023.

Secondly, the ABS noted that the increase in the unemployment rate “coincided with a higher-than-usual number of people who were not employed but who said they will be starting or returning to work in the future.” This was similar to what was observed this time last year – in the presence of a tight labour market, individuals may seek more opportunities and look to change jobs (typically over holiday periods), leading to a larger-than-usual (and in the case of last year, temporary) increase in the unemployment rate.

Looking past the volatility associated with shifting seasonal patterns, the headline results were broadly as we had anticipated. Growth in employment flatlined in the month, rising just +0.5k to be up 0.4% on a three-month average basis, the softest pace since the ‘delta’ outbreak in 2021. At a time of rapid population growth, the employment-to-population ratio also continues to moderate, down 0.1ppt to 64.1% in January.

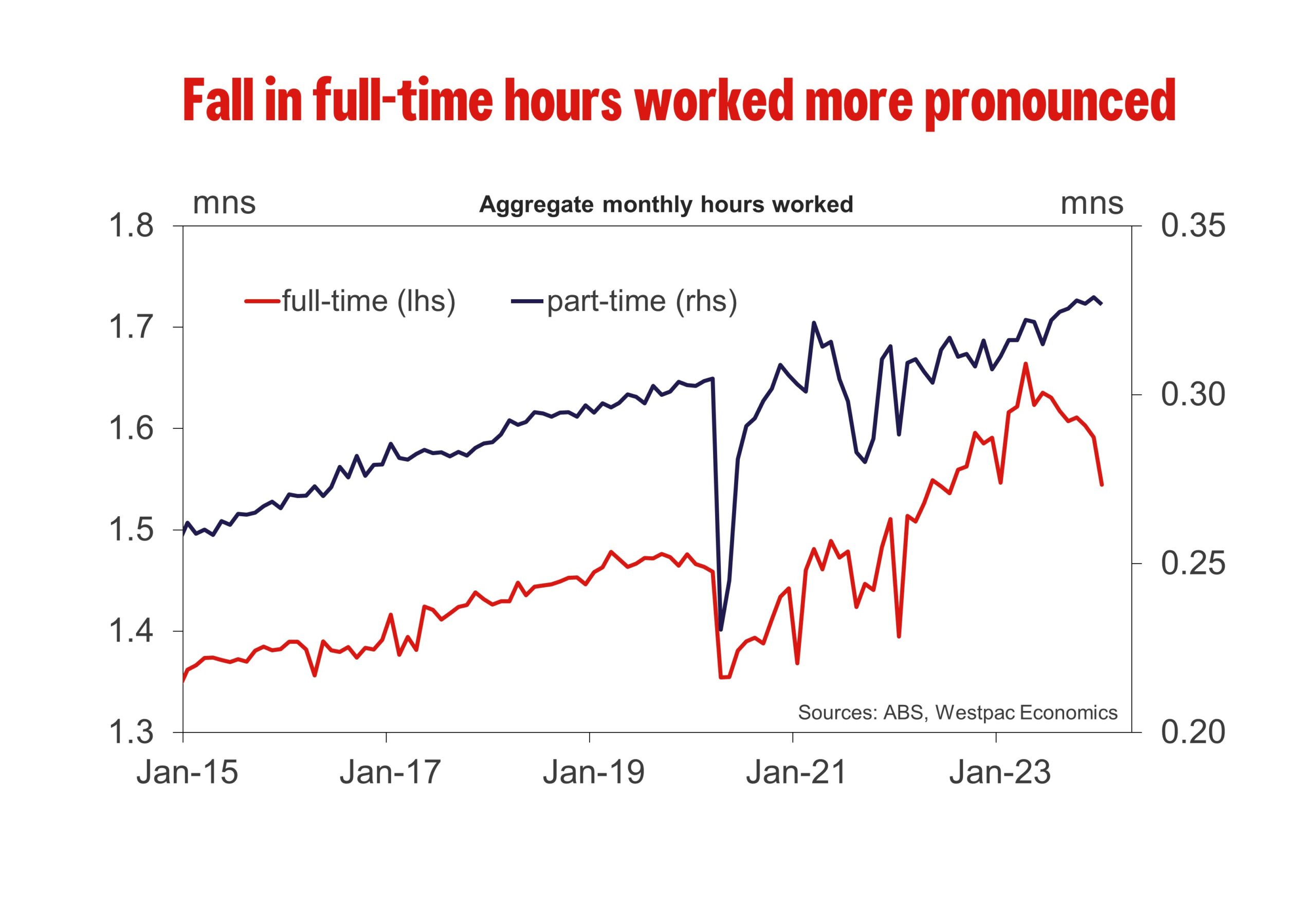

Given the flatness in employment growth, and with participation holding flat at 66.8%, the unemployment rate ticked higher from 3.9% to 4.1%, marking the first time the unemployment rate has been above 4.0% in two years. And, as discussed below, the majority of net employment growth has recently been from part-time work, and those working fewer hours are struggling to gain more, implying a very weak trend for aggregate hours worked.

Overall, the broader picture is of a labour market that is in transition, as softness begins to emerge after a period of historic tightness.

Hours Worked

The number of hours worked declined by 2.5% over the month of January. There were particularly large monthly falls in NSW (–4.1%), South Australia (–3.8%), Victoria (–3.4%), and Western Australia (–2.8%).

While the very weak monthly read in part reflects difficulty associated with adjusting original data for the evolving seasonal patterns, the underlying trend is unambiguously weak. Over the last six months, in annualised terms, hours worked have declined by 8.2%, the sharpest fall on record (going back to 1979) outside of the pandemic.

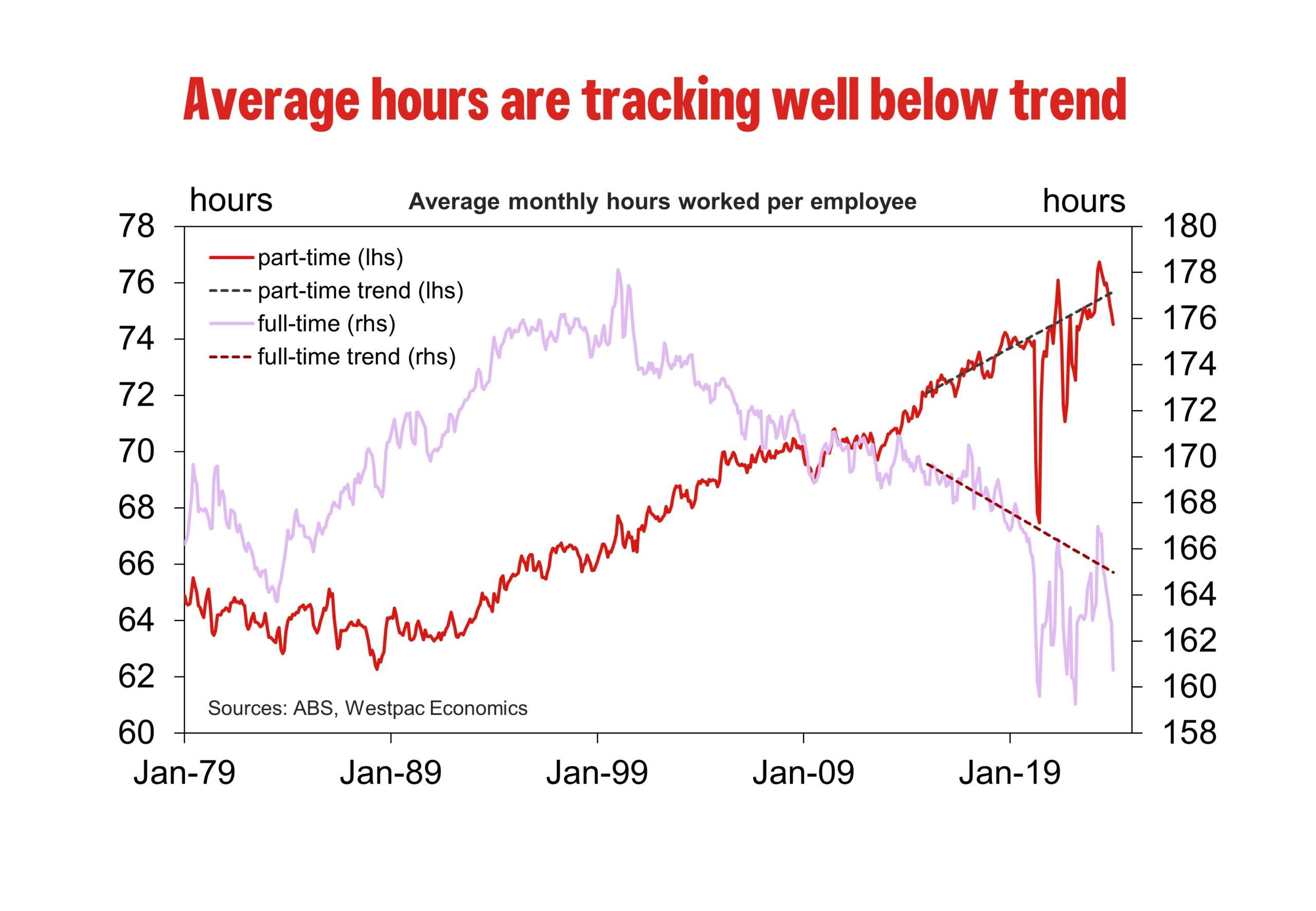

Employers are now clearly responding to the pull back in spending by adjusting the number of hours employees are required to work. With lower demand there is less need for overtime or extra shifts. This is consistent with the sharp falls we have seen in the average number of hours worked by both full time and part time employees. We have also seen a significant fall in the share of part time workers who are able to pick up extra hours and move to full time status (those working 35hrs/wk or more). This has seen the share of full-time employment fall from around 70.0% a year ago to 69.0% today, and trending toward the pre pandemic average of around 68.5%.

As the supply side of the economy continues to adjust from the pandemic and demand slows on the back of tighter macroeconomic policy, employers are likely to continue to pull back on demand for labour. Given how tight the labour market has been during this cycle, employers are understandably wary of letting people go. Instead, they are likely to make this adjustment through demanding fewer hours of their employees.

Other Labour Market Measures

Consistent with the sharp fall in the number of hours worked, other labour market indicators are pointing to a softening in conditions.

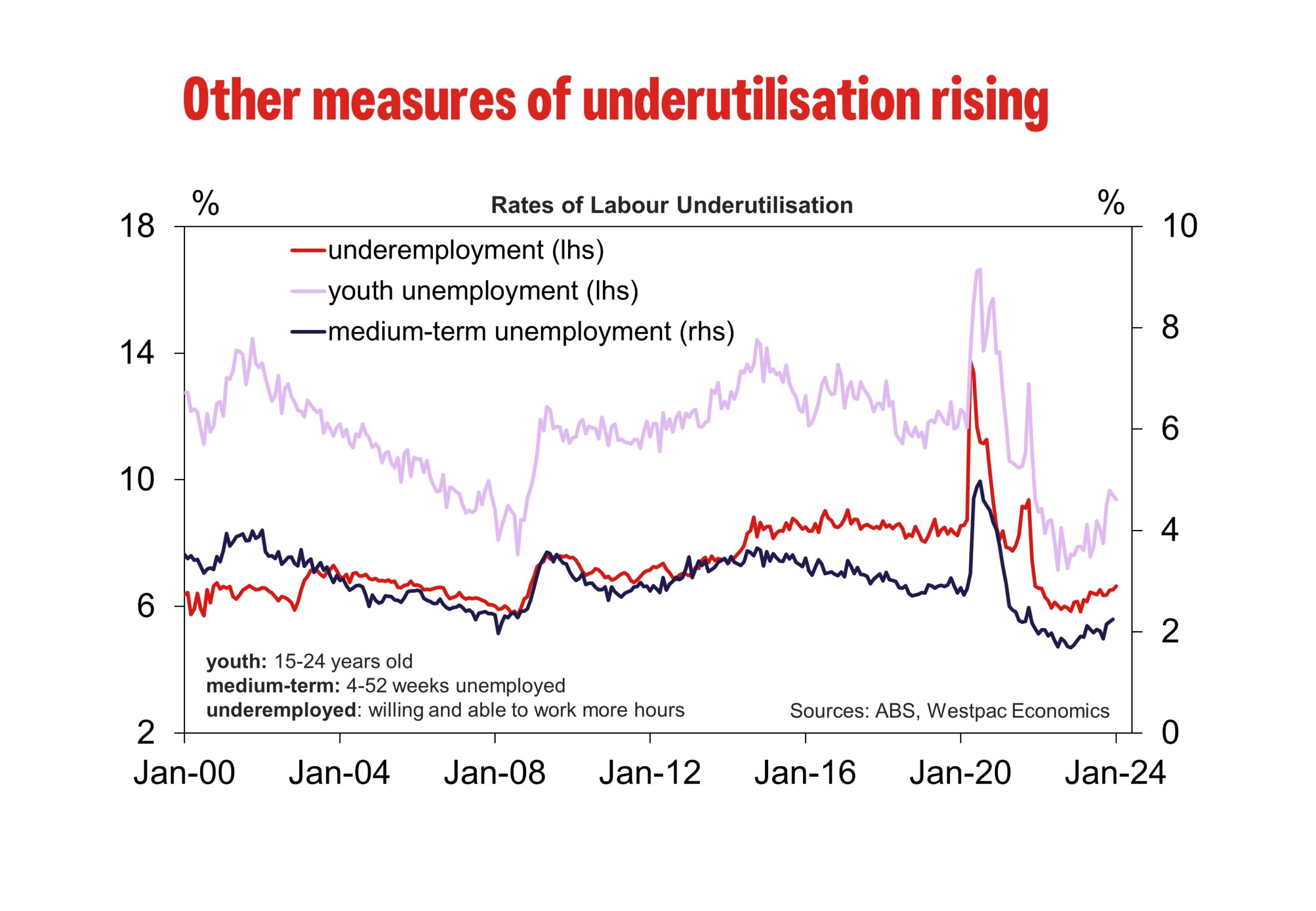

The underemployment rate, which measures the share of employed workers who are willing and able to work more hours, ticked up to 6.6% in January. Over 2023, the underemployment rate has drifted higher in trends terms, coinciding with the slide in the number of hours worked. The underutilisation rate, which combines the unemployment and underemployment rates, increased to 10.7% – highest rate since January 2022.

The youth unemployment rate, which measures the share of unemployed workers between the ages of 15 and 24, ticked lower to 9.4% from 9.5% last month. Some of this fall was driven by a lower participation rate (70.0% in January compared with 70.1% in December). Again, this could reflect difficulties associated with adjusting the data for evolving seasonal patterns. However, the trend is clear – the unemployment rate has moved higher since late 2022, with the participation rate also trending lower over this period. Being a highly sensitive group to changes in labour demand, this provides another signal that softness in labour demand is emerging.

Outlook

All-in-all, the results from the January survey were broadly consistent with our expectations. Shifting seasonal dynamics likely played a role in some of January’s weakness, and similar to last year, this may give way to something of a rebound with respect to employment and hours worked in February.

That said, the underlying tone of the data continues to speak to a softening labour market, predominately presenting through a notably weak trend for hours worked, slowing employment growth, and a gradually rising unemployment rate.

Looking ahead, as labour demand and supply continue to move into balance, tightness in the labour market will continue to fade. Given just how sharp the turnaround in hours worked has been over the past six months – as businesses respond to a weakening backdrop for domestic demand – there is increasingly limited scope for labour demand adjustment to come purely from hours worked alone. This will likely lead to weakness in employment growth and a further rise in the unemployment rate, to a forecast 4.5% by year-end.

For the RBA, today’s update provides further confirmation that the labour market is indeed easing. That said, in its February Statement on Monetary Policy, the RBA continued to assess the labour market as “tight relative to what is consistent with full employment”. More updates on the state of the labour market will be necessary before any material adjustment to that assessment occurs, especially given the seasonality associated with January’s figures.

{kind=link}