Summary

- Canadian economic trends have been mixed, but softer on balance. GDP shrank in Q3 but appears to have rebounded in Q4. Still, given a softening labor market, modest growth in household income and rising interest rates, and a subdued outlook for business and investment spending, we expect Canadian GDP growth to slow moderately to 0.9% in 2024.

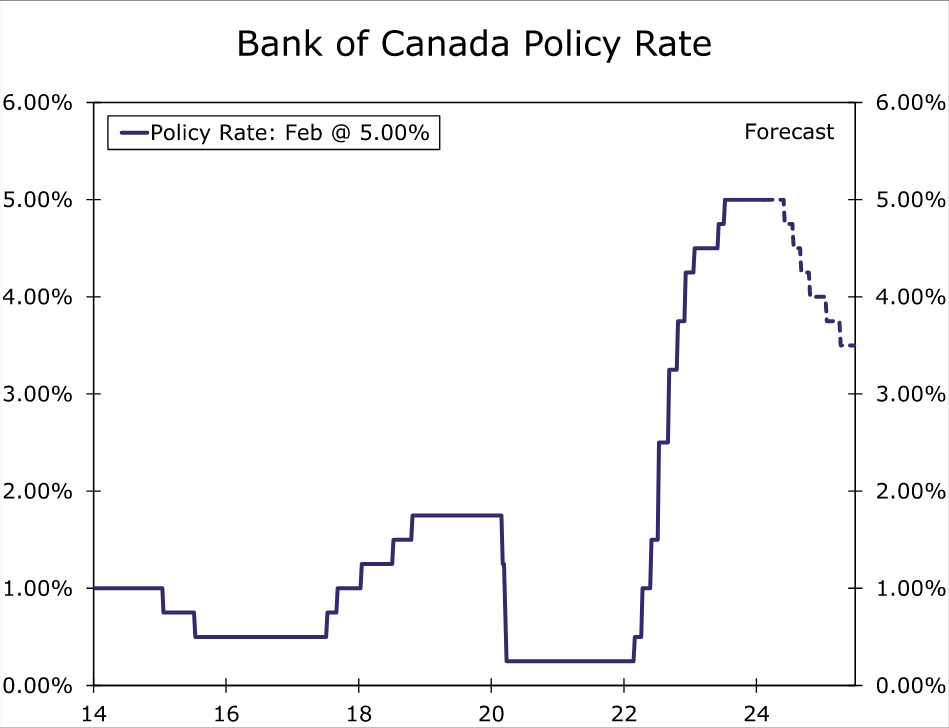

- With the economy downshifting to a lower gear, the Bank of Canada shifted focus at their January monetary policy announcement. The central bank held rates steady and, acknowledging slower growth and some improvement in inflation, said it has shifted from discussing whether the policy rate is restrictive enough to restore price stability, to how long it needs to stay at the current level.

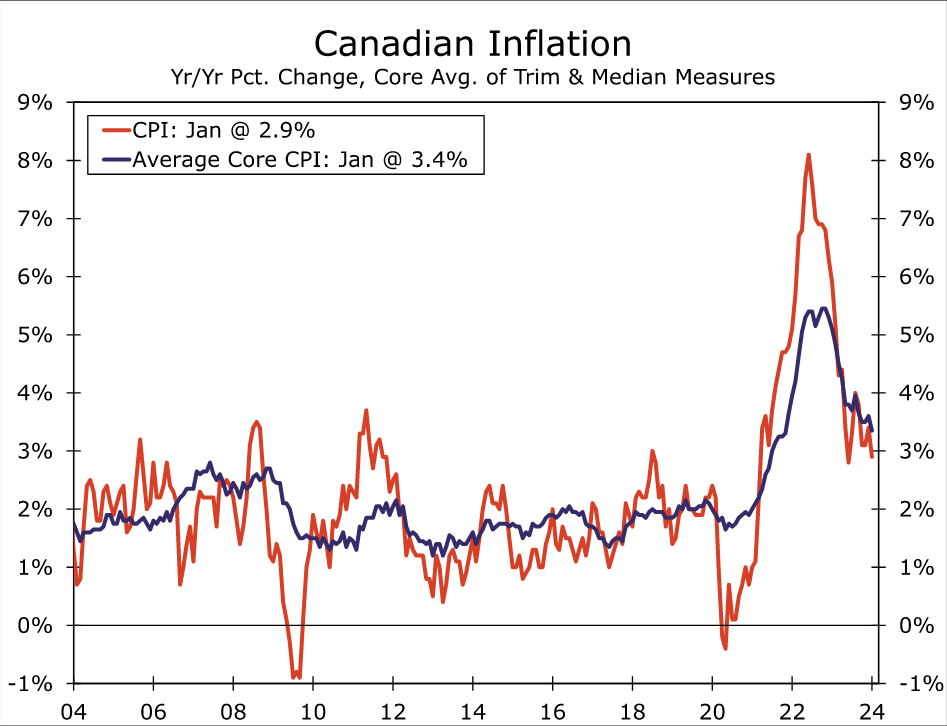

- The Bank of Canada received encouraging news from the January CPI, which showed both core and headline inflation slowing more than expected. However, some measures of services inflation remain elevated, while the three-month annualized change of the core CPI is still some way above the 2% inflation target.

- We still think it is too early for the central bank to cut rates just yet. While an April move is potentially in play if growth softens further and inflation slows further, we still view June as the more likely timing for an initial 25 bps rate cut. More broadly, we forecast a cumulative 100 bps of rate cuts this year, which would see the policy rate finish 2024 at 4.00%.

Canadian Economy Softening, Slowly and Quite Surely

The news from Canada’s economy has been mixed in recent months but, we believe, remains consistent with an overall ebbing in the pace of economic expansion. Indeed, Canadian GDP shrank during the third quarter, before perking up a bit during Q4. In November, Canada’s GDP rose 0.2% month-over-month, a bit more than expected, while Statistics Canada advance estimate is for a further 0.3% gain in December. If realized, that would see Q4 GDP expand by around 1.2% quarter-over-quarter annualized, essentially reversing the decline in the third quarter.

The increase in fourth quarter GDP may, however, prove to be only a brief interruption to generally disappointing growth performance. Notably, the labor market still appears to be following a gradually softening trend. The latest jobs report for January did show a jump in employment, of 37,300, although the gain the was driven by part-time and public-sector jobs. Full-time employment actually fell by 11,600 in January, a second straight decline, while private-sector employees rose by a modest 7,400. The unemployment rate fell slightly to 5.7%, but is still up from a low of 4.9% in mid-2022. Thus, despite the flattering headlines, we still view the January report as consistent with a gradual softening in labor market conditions.

Other household finance fundamentals are also consistent with only moderate gains in consumer spending, in our view. Slower inflation has seen growth in real household disposable income return to positive territory although, at 1.5% year-over-year in Q3-2023, the growth in real income is only just keeping pace with a similar sized gain in consumer spending over the past four quarters. In addition, a significant rise in household debt servicing costs poses a potential headwind for consumer spending. By Q3-2023, interest costs as a proportion of household disposable income had risen to 9.3%, while total debt servicing costs had risen to 15.2%, both multi-year highs. Overall, we see few reasons to expect a strong upswing in consumer spending over the next several quarters.

Meanwhile, the outlook for businesses also continues to cool. In the Bank of Canada’s Q4 business survey, the central bank’s overall Business Outlook Indicator improved slightly, albeit remaining at depressed levels. In contrast, the Indicator of Future Sales softened further to a net balance of -10 which, apart from the pandemic, is the weakest reading since 2009. Elsewhere, growth in corporate profits remains on an overall slowing trend and industrial capacity utilization has dropped below 80%, factors which could restrain investment spending going forward. Given the consumer and business backdrop, and even with the prospect of a soft landing for the U.S. economy, we forecast Canadian GDP growth to slow slightly to 0.9% in 2024, from 1.1% in 2023.

Bank of Canada’s Monetary Policy Pivot Underway

With the Canadian economy downshifting to a lower gear, Bank of Canada (BoC) policymakers announced a shift in focus at their January monetary policy meeting. The BoC held its policy rate at 5.00% and said it would continue with its policy of quantitative tightening. Regarding activity, the central bank said that with “weak growth, supply has caught up with demand and the economy now looks to be operating in modest excess supply.” For 2024 the central bank forecasts GDP growth of 0.8%, slightly below our own forecast. The central bank also said that labor market conditions have eased, but that wage growth remains elevated.

The BoC’s inflation assessment was less sanguine. The central bank observed that shelter costs remain the biggest contributor to above target inflation and that, while corporate pricing behavior is normalizing and evidence of reduced price pressures is becoming more widespread, core measures of inflation are not showing sustained declines. Accordingly, the BoC said it is “still concerned about risks to the outlook for inflation, particularly the persistence in underlying inflation” and that it “wants to see further and sustained easing in core inflation.”

In a significant shift in policy guidance, the BoC removed its tightening bias at its January meeting, with its formal announcement no longer indicating the central bank “remains prepared to raise the policy rate further if needed.” BoC Governor Macklem described this as a shift in focus for policymakers from discussing whether the policy rate is restrictive enough to restore price stability, to how long it needs to stay at the current level. In other words, the conversation has shifted from “how high” the policy rate needs to go, to “how long” it needs to stay at an elevated level. Macklem added that monetary policy is working to relieve price pressures, and that the central bank needs to “stay the course.”

Following the Bank of Canada’s pivot, the latest news on the inflation front offers some encouragement that a policy rate cut might be coming closer in the months ahead. The latest inflation news was a favorable surprise, as the headline CPI slowed more than expected to 2.9% year-over-year, and the average core CPI also slowed more than forecast to 3.4%. That said, some other measures of services sector inflation continue to show some persistence, as shelter costs rose 6.2% and services inflation rose 4.2%. Meanwhile, the three-month annualized gain in the average core CPI, an important metric that is closely followed by the Bank of Canada, rose at a 3.2% pace. That was down from the 3.6% reading in December, but still ways above the central bank’s 2% inflation target. As a result, we still think it is too early for the Bank of Canada to lower interest rates just yet. We expect the BoC to stay on hold through March and April, and do not see a rate cut coming before June. We believe Bank of Canada rate cuts will be contingent on continued soft economic growth, as well as labor market trends that begin to weigh more noticeably on wage and price growth. We also think the Bank of Canada will be more comfortable considering rate cuts if core inflation is trending more convincingly in a 2.5%-3.0% range, and once wage growth slows nearer 4%.

While it’s possible those conditions could transpire by April, we believe it is more likely those conditions will be met by June, and our view remain for an initial 25 bps rate cut to be delivered at the June announcement. For all of 2024, we expect a cumulative 100 bps of rate cuts from the Bank of Canada, just a little less than the cumulative 125 bps of rate cuts from the Federal Reserve over the same period. Moreover, in both Canada and the United States we anticipate subdued economic growth, but no recession. Canada’s economic and monetary policy backdrop has restrained the Canadian currency during the early part of 2024, a trend that could continue for the time being. Given a broadly similar growth and monetary policy outlook for Canada and the United States, its also possible the Canadian dollar could be an underwhelming performer over the medium-term. In fact, even by the end of 2024 we see only modest gains in the Canadian currency, forecasting a USD/CAD exchange rate CAD1.3300 by the end of this year.

{kind=link}