Westpac economics sees the RBNZ leaving the OCR at 5.5% at the February Monetary Policy Statement and adopting a hawkish outlook for the OCR.

Hawkish hold expected

- We expect the RBNZ will leave the OCR unchanged at 5.5% at its February policy meeting.

- The RBNZ’s short term forward profile for the OCR is likely to be little changed and continue to suggest a chance of a further lift in the OCR perhaps at the May Monetary Policy Statement.

- The longer-term OCR profile may be revised up – especially if another adjustment of the neutral OCR occurs.

- More hawkish scenarios are realistic – but we see a 25bp tightening as just a 25% probability.

- Future data on non-tradables inflation, the labour market, the housing market and the Budget will be key in making the case for any further tightening – but in May, not at the current time.

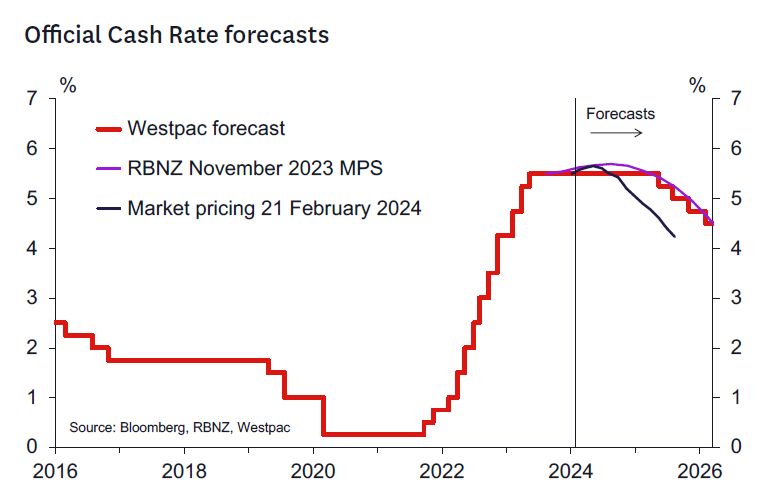

- We continue to expect the OCR to remain at 5.5% until early 2025.

The RBNZ’s decision and forward track.

We expect the RBNZ to leave the OCR at 5.5% at its February policy meeting and think that most interest will centre on the profile for interest rates in 2024 and beyond. A hike in the OCR is main alternative outcome with a 25% probability.

We think the RBNZ’s objective will be to try to maintain the recent repricing in financial markets which has removed the expectation of rate cuts until at least the end of this year. The RBNZ will also leave open the option to tighten at the May Monetary Policy Statement, should the data warrant.

We think the RBNZ will be on edge due to some aspects of the recent data flow – even though a straight read of the entirety of that flow probably shouldn’t increase concerns that inflation will move back inside the target range. Our recent “Hawks, Doves and Kiwis” note includes a number of charts that illustrate the issues discussed here. The key issues raising those concerns will be:

- the slower than expected increase in the unemployment rate (which will likely require a further adjustment of their labour market forecasts to push out the period over which the labour market adjusts).

- the higher-than-expected non-tradables inflation outcome – that comes after a string of similar disappointments on this score. If the RBNZ adjusts up its Q1 2024 non-tradables forecast to Westpac’s own level (Westpac forecast +1.4% q/q, 5.6% y/y vs. RBNZ November Statement 1.0% q/q, 4.9% y/y) this will further amplify their concerns that non-tradables inflation won’t subside quickly this year.

Market views will likely be best anchored around an expectation of no easing in 2024 by leaving the shortterm OCR forecast track unchanged from November. As noted below, a straight read of the data that has emerged since November might suggest a lower OCR track. This is because those more concerning inflation factors have been balanced to some extent by the significantly lower headline inflation outcome and much weaker GDP and economic momentum (among others – see below).

But we think the RBNZ will down-weight those more comforting factors and keep open the option of tightening in May and leave the short-term OCR forecast track unchanged. Further out, we see potential for increased in the OCR track (through 2025 and beyond) as they may further revise up their estimate for the neutral OCR (which has been revised twice in the last 6 months). The increased medium term inflation pressure coming from the required adjustments to their labour market forecasts may require an offset in terms of the length of time the OCR remains around 5.5%. This approach would be consistent with continuing with the “longer” rather than “higher” strategy in place since May 2023.

Key developments.

A straight read of the data flow since the November Statement might imply a more comforting inflation outlook – although we suspect the RBNZ will put more weight on the more concerning data points. Below, we discuss key data developments since the November MPS (arrows in brackets give our assessment of the likely first-round impact of this data on the RBNZ’s assessment of the OCR):

Most important factors.

- GDP (↓↓↓): The Q3 GDP report suggested the economy was 1.8% smaller than the RBNZ forecast in November. Recent economic momentum was weaker than expected, (-1% surprise in the last six months). The RBNZ will assume that some of this surprise reflects weaker productivity growth and potential supply. But most of the more recent weakness is likely indicative of a lower output gap profile and hence less medium-term inflation pressure.

- Headline inflation and inflation expectations (↓): Annual CPI inflation was 0.3% lower than the RBNZ expected in Q4. The RBNZ will see this as helping lower inflation expectations which will dampen future inflation pressures. Lower business sector inflation expectations will have confirmed this.

- Non-tradables inflation (↑↑): Non-tradables inflation was again higher than expected by the RBNZ in Q4 (0.2ppts higher) and remained elevated at 5.9% y/y. This will be of concern as it follows a few quarters of surprises in the same direction and suggests that non-tradables inflation will only slowly fall from here.

- Labour market (↑↑): The unemployment rate rose 0.2ppts less than the RBNZ had expected in Q4 and private sector wage growth was also firmer than expected. This will likely force a further adjustment in the RBNZ’s labour market forecasts following on from similar adjustments in the last few Statements.

Secondary factors.

- Migration (←→): News regarding migration is likely to have been a wash for the RBNZ. While the peak in annual migration – in October – was slightly above the RBNZ’s expectations, there has been tentative evidence that the cycle has peaked. It remains to be seen how quickly the migrant inflow will ebb from here.

- Housing market (↓): Both housing turnover and house prices have been subdued in recent months and expectations of short-term house price growth have been accordingly scaled back a bit. The RBNZ should be more comfortable about this at the margin but may want to see how the market evolves in coming months to get a read on how the market will evolve over the year ahead.

- Global economy (←→): The US economy has continued to significantly outperform expectations with consensus forecasts of growth revised up accordingly. However, consensus forecasts of 2024 growth in the Asia-Pacific region – the most important region for New Zealand’s exports – are unchanged from those held in November (although actions taken by Chinese authorities have slightly moderated nearterm downside risks associated with that economy). Consensus forecasts for growth in Western Europe have been revised down modestly.

- Global policy context (↓): Importantly, policy makers now seem surer that official interest rates will be reduced at some point in the coming year. This likely raises the bar a bit for the RBNZ to diverge from the general direction of the global pack – although we think the timing of any RBNZ easing will reflect domestic economic factors and not offshore central bank actions.

- Export prices (↑↑): Some key export commodity prices have shown welcome improvement over recent months, notably the price of whole milk powder which has increased 11% since the November MPS. The improved outlook will nonetheless have come as a relief to the rural sector where a paring back of spending likely contributed to the weakness of the economy in the second half of last year.

- Exchange rate (↓↓): The trade-weighted exchange rate (TWI) is currently more than 2% stronger than the RBNZ had assumed in November. An upward revision to the RBNZ’s forecast will directly lower the RBNZ’s forecasts of inflation in the tradables sector over the coming year.

- Fiscal settings (←→): If the RBNZ takes the HYEFU forecasts at face value, the cumulative negative fiscal impulse over the forecast period is fractionally smaller than was depicted in the PREFU. However, the RBNZ will likely defer any strong judgment on the implications of fiscal policy for the economic outlook until the Government has published its Budget Policy Statement (27 March) and Budget 2024 (30 May).

The communications objective.

We think the RBNZ is likely to be happy with current market pricing. They will likely have been very uncomfortable with market views of near term easing that were held in December and January. Similarly, we suspect they were also not as hawkish as market views a week or so ago. We think the RBNZ will want to allow the option to tighten in May should data support that view. We don’t think the RBNZ will want to see markets price in rate cuts for at least 6 months.

We think the RBNZ will want to encourage markets to maintain current short-term pricing (i.e. a 50/50 chance of a hike at the May Statement) and drive home the view that the OCR is not moving lower in 2024. This will ensure retail lending rates don’t fall and will prepare markets for a hike should data in the next few months suggest reduced confidence that inflation will decline to 2% in the second half of 2025.

Scenarios.

We see three main scenarios:

- Baseline case (65% probability) the OCR is unchanged and the RBNZ retains a similar short term OCR track to November (peak OCR in Q3 – maybe bought forward to Q2 – at around 5.69%). Longer term OCR expectations could be revised up if the RBNZ makes another adjustment to its neutral OCR estimate or if the RBNZ sees increased medium term inflation risks from the slowly adjusting labour market. The RBNZ could hike at the May MPS should core inflation pressures not significantly abate (Q1 CPI due 17 April), if the labour market doesn’t sufficiently adjust (Q1 data due 1 May) or if the government’s fiscal stance appears insufficient to ameliorate inflation concerns (Budget 24 will be released after the MPS but we expect the RBNZ will have the key data before then).

- Hawkish case (25%) the OCR is hiked to 5.75% and the forecast track is revised up to convey a risk of a further rate hike in 2024. Easing might be pushed out to mid-2025. This would be linked to risks of housing strength, a slower rise in the unemployment rate from here and an ongoing sluggish response of core inflation to tighter monetary conditions.

- Dovish case (10%) the OCR remains at 5.5%. The OCR track is revised down slightly to be like that in the August MPS (i.e., around a one-third chance of a hike this year), but the OCR remains at 5.5% until early 2025. Upside risks to the OCR might be mentioned but be of a much lower profile – the core message would be one of OCR stability through 2024).

Our OCR view for 2024.

We expect the OCR to remain unchanged over 2024. There are certainly risks of another move higher – most likely around the middle of the year once further data on the extent of labour market adjustment, core inflation pressures, migration and housing market pressures and the fiscal stance become much clearer. But, more likely, as the year proceeds it will become more apparent that inflation is on the right track, implying the current level of the OCR is the right one, given sufficient time.

{kind=link}