- A summer rate cut by the Fed hangs in the balance amid persistent inflation

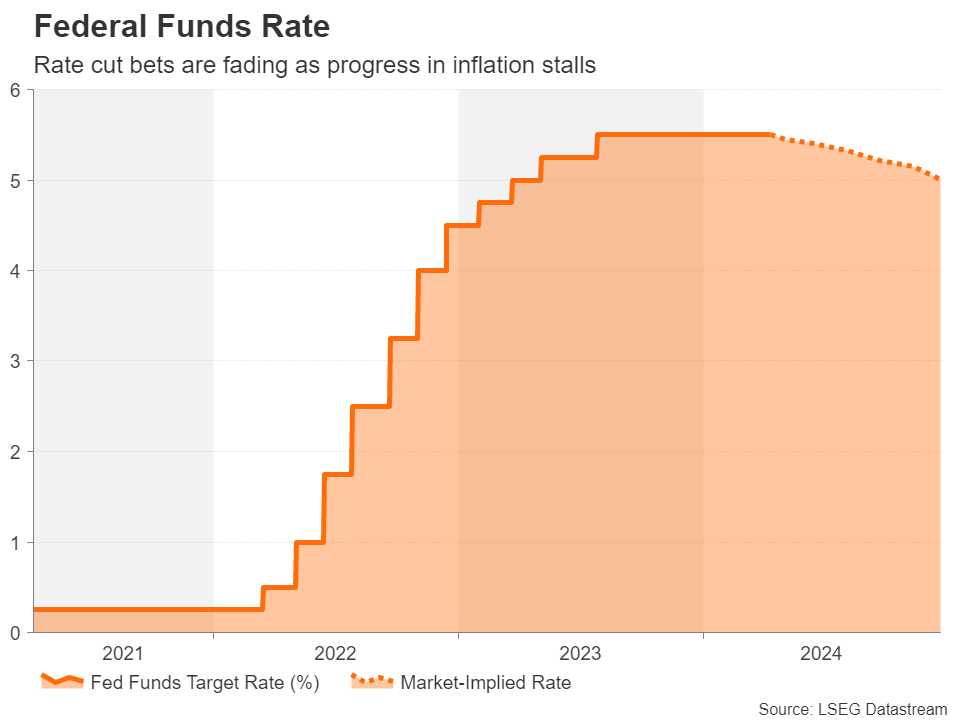

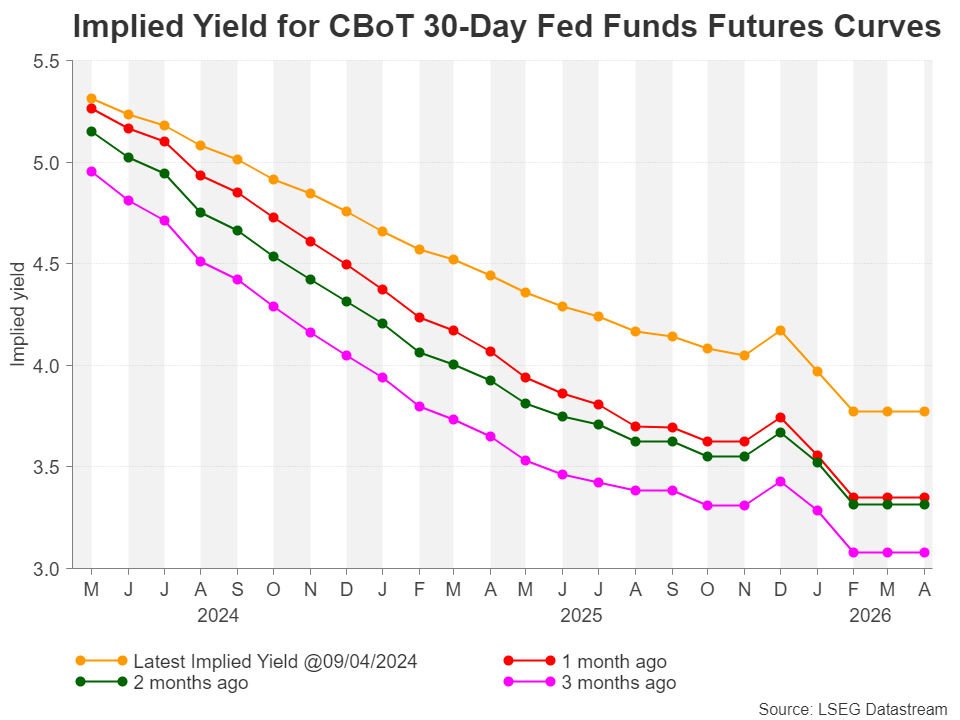

- Rate cut bets have been scaled back from more than six to around two

- But limited fallout on Wall Street; can the risk rally survive no rate cuts?

Waiting for the elusive rate cut

Ever since the Fed signalled it was done hiking rates in November last year, the focus swiftly turned to rate cuts, with the timing and scope of policy easing consuming investors’ attention. Subsequently, markets have been abuzz with rate cut speculation all year and that theme looks set to dominate for some time yet as the timing keeps getting pushed back.

The stalling of the progress to lower inflation to the Fed’s 2% target could soon go from being a minor setback to a major policy headache for Federal Open Market Committee (FOMC) members, which set interest rates. The Fed is still reeling from its policy error in 2021 when it misjudged the surge in inflation to be transitory.

Resilient economy keeping Fed on its toes

Keen on avoiding making the same mistake twice, Chair Jerome Powell has been careful not to pre-commit to any rate cuts before inflation has moved a lot closer to the target. Central banks tend to take their foot off the brake well in advance of inflation reaching their goal, but it’s also usually the case that economic growth has slowed down substantially by then.

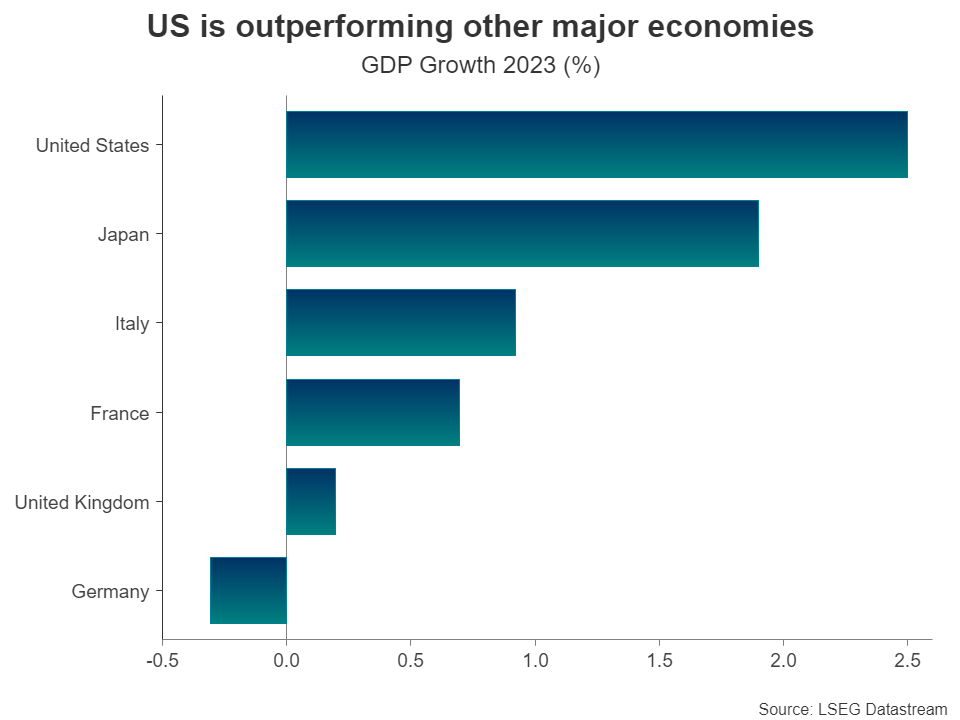

That is certainly not the case with the US economy at the moment, which continues to confound expectations of a slowdown. Full year GDP growth accelerated to 2.5% in 2023 even as borrowing costs hit the highest in two decades, and the economy likely grew by a similar rate in the first quarter of 2024.

Not slowing down

At the heart of the ‘problem’ of an overly strong economy is the tight labour market. Jobs growth has quickened in recent months, with nonfarm payrolls gains exceeding 250k since December, and the unemployment rate has held near decade lows below 4.0%. Fortunately for policymakers, wage growth has been steadily moderating over the past two years, in a sign that the strong demand for workers is being matched by a rise in the supply of labour.

An influx of migrants, as well as previously economically inactive workers being attracted into the labour market by higher wages are the likely causes of the boost in the size of the labour force. The question now is whether this trend is sustainable. Even if the US economy can maintain full employment without adding to wage pressures, consumer spending is unlikely to wane as long as the jobs market remains in such good shape, and that keeps the risks to inflation tilted to the upside.

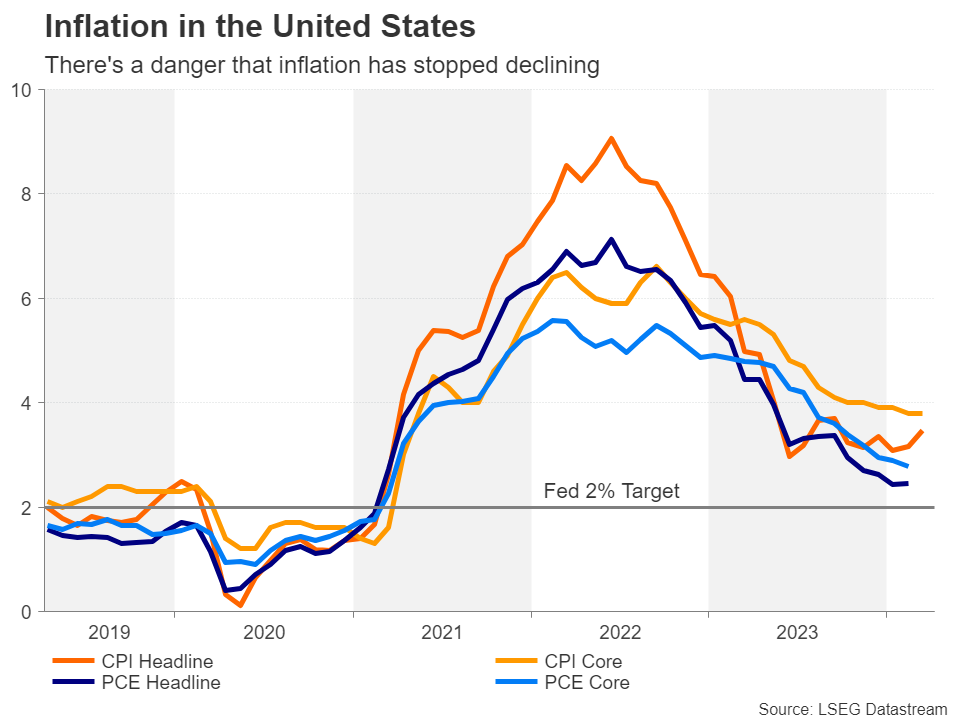

Inflation picture has become muddied

All this has led some analysts to question whether the Fed has tightened policy enough to prevent a resurgence in inflation let alone bring it down all the way down to 2%. Various price metrics for the American economy indicate that inflation has started to bottom out.

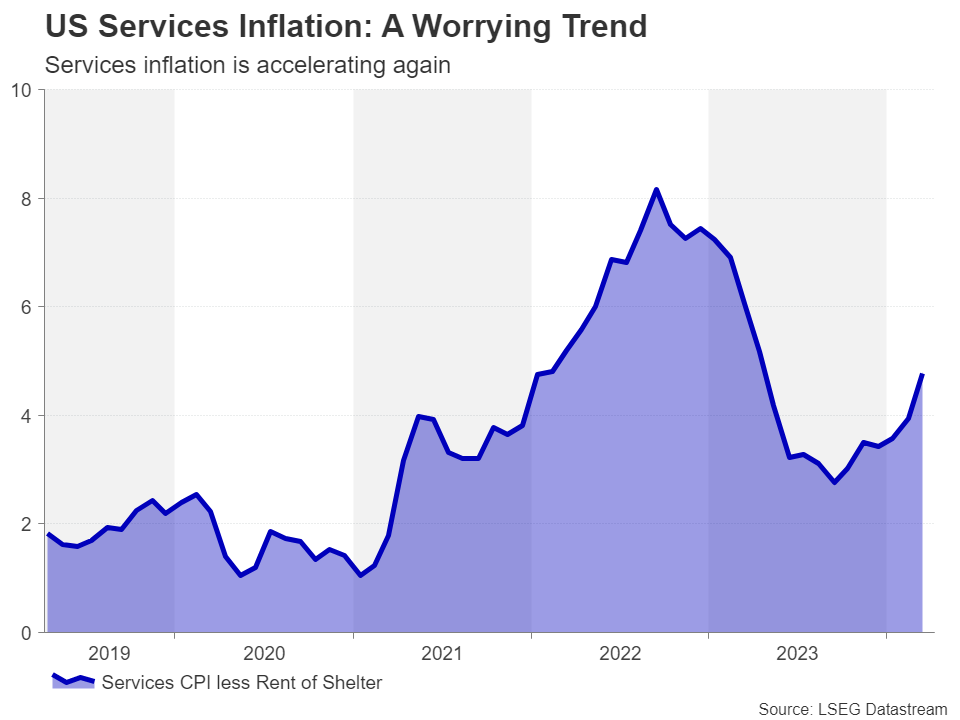

Headline inflation as measured by the consumer price index (CPI) has been moving sideways since June 2023 and so have producer prices. Moreover, a key gauge of services CPI jumped to 4.8% in March, far from abating. Services price pressures have been the stickiest and most problematic for the Fed in its fight against inflation.

There’s been better progress with the Fed’s preferred PCE measure of inflation. The all-important core PCE price index eased to 2.8% in February – the lowest in nearly three years.

Are price pressures simmering again?

However, there are plenty of risks that could yet scupper central banks’ hopes of reining in inflation once and for all. Energy prices are rising again – WTI oil is up about 19% in the year-to-date – amid heightened geopolitical tensions globally. The fighting between Israel and Hamas in the Middle East threatens to embroil the United States and Iran, while the ongoing war between Ukraine and Russia is showing no sign of de-escalating.

Aside from crude oil, other commodity prices, such as copper and cocoa, have also soared. Meanwhile, the disinflation in goods prices appears to be levelling off.

Hoping for the best

From the Fed’s perspective, there’s still good reason to believe that inflation will fall further in the coming months, allowing it to begin cutting rates at some point later in the year. But against the current inflation backdrop, the projected three rate cuts in 2024 are looking increasingly optimistic.

Several Fed officials have already hinted that they see scenarios with fewer than three rate cuts and some are also not sure if inflation will have cooled enough by June to proceed with the first 25-basis-point reduction.

What’s surprising, though, is how well market expectations have aligned with both the data and the Fed’s rhetoric in recent weeks. With expectations for June easing fading and a July move hanging in the balance, a 25-bps cut might be delayed until September. In addition, total rate cut bets for 2024 have been dialled back to fewer than 50 bps.

No panic yet

This suggests that a further hawkish tilt by the Fed in the run up to the May and June policy meetings won’t come as much of a shock for investors. Until recently, equity markets had been taking this steady repricing in their stride. Shares on Wall Street have been scaling all-time highs alongside Treasury yields that have been climbing to fresh yearly highs.

The soft-landing narrative whereby the economy can keep growing as interest rates remain high and inflation falls, has been propping up the risk rally. Even the struggling Eurozone economy may come out of this inflationary episode by evading a recession, while some green shoots of economic stabilization in China are also buoying investor sentiment.

Are markets ready for no rate cuts?

However, markets may now be starting to become more nervous about the prospect of later and fewer rate cuts if there’s a further pricing out of Fed easing in the coming weeks, especially if the 10-year yield continues to edge higher, surpassing 4.50% and pushing up long-term borrowing costs for firms.

At this stage, with US consumers still spending, and the artificial intelligence (AI) mania fuelling a rally in all related stocks, it’s hard to see what the trigger point for a sharp stock market correction would be. Judging by investors’ reaction to the latest paring back of rate cut bets, markets would probably be able to tolerate just two rate cuts in 2024. However, that might change if inflation does not recede further as expected over the next few months and the prospect of just one or even no rate cut becomes real.

Given how inflation has repeatedly surprised to the upside since its upsurge in 2021 and more importantly, how policymakers have again and again underestimated its persistence, the risk of no rate cuts this year and a potentially big market fallout cannot be dismissed.

{kind=link}