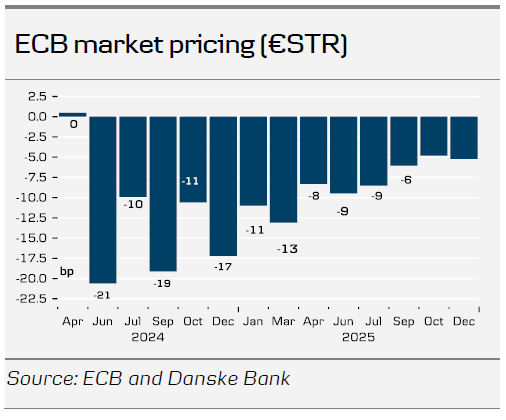

Today, the ECB decided to leave policy rates unchanged as unanimously expected. A rate cut looks set to come in June, subject to further confidence on the three criteria that have guided ECB policy making through the past year.

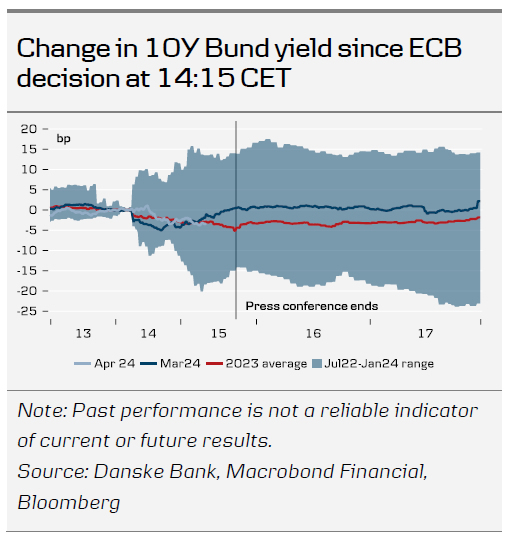

The next to no new policy signals left markets largely unchanged.

Limited new signals

The ECB meeting today was relatively uneventful in terms of policy signals and consequently didn’t leave a mark on the market. The key sentence of the policy statement was ‘If the Governing Council’s updated assessment of the inflation outlook, the dynamics of underlying inflation and the strength of monetary policy transmission were to further increase its confidence that inflation is converging to the target in a sustained manner, it would be appropriate to reduce the current level of monetary policy restriction.’ while still calling for its ‘data-dependent and meeting-by-meeting’ approach to monetary policy setting and ‘not pre-committing to a particular rate path’.

Given that the ECB meeting went basically as expected, see also our ECB Preview – An intention to cut, 5 April 2024, with the ECB guiding for a June rate cut subject to confirmation of the three factors that have guided the ECB’s monetary policy setting in the past year (namely the ‘updated assessment of the inflation outlook, the dynamics of underlying inflation and the strength of monetary policy transmission’), we continue to like our ECB rate call of a 25bp rate cut call in June, followed by further 25bp rate cuts once per quarter through the end of 2025. That said, and zooming into 2024, we see risks skewed to less than three rate cuts this year, due to the sticky domestic inflation.

No change in the ECB’s view on inflation and growth

The ECB has not changed its view on inflation and growth since the March meeting. Lagarde noted that incoming information has broadly confirmed the Governing Council’s previous assessment of the medium-term inflation outlook. Indicators of underlying inflation are easing, while wage growth is gradually moderating. However, robust domestic price pressures persist, particularly in the services sector, keeping inflation elevated in that area, posing an upside risk for the inflation outlook. However, firms are absorbing part of the increased labour costs through their profits. Financial conditions remain tight, and previous interest rate hikes continue to dampen demand, contributing to the downward pressure on inflation.

Lagarde said that the economy remains weak, especially due to the manufacturing sector. The ECB expects a gradual recovery in growth led by the service sector, supported by rising real incomes and improved terms of trade. Export growth should pick up as the global economy recovers and spending shifts to goods. Risks to the growth outlook remain tilted to the downside.

Muted market reaction

As expected, the market impact was very limited. EUR/USD initially declined slightly on the announcement, reaching around the 1.0715 mark, as the ECB essentially communicated that a cut in June is coming. Shortly after, US PPI figures came out slightly lower than expected, providing some support to EUR/USD and bringing the cross back to the mid 1.07-1.08 range, which is status quo for the day. There were no significant market moves during Lagarde’s press conference.

At the current juncture, US data remains the primary driver of EUR/USD. Positioning data has recently shown a significant uptick in long USD positions, now in stretched long territory. This could suggest a potential asymmetric outcome favouring a weaker USD in the short term, especially in response to softer US data. That could potentially give EUR/USD some support in the next couple of months. However, over the full year, we still expect EUR/USD to trend lower. We believe the US economy is fundamentally in a stronger position relative to the euro area, based on factors such as relative terms of trade, real rates, and relative unit labour costs. Additionally, there are clear signs that underlying inflation appears more persistent in the US compared with the euro area. A strong USD, coupled with tighter financial conditions, is necessary for the Fed to sustainably achieve its inflation target of 2%. Our forecast for EUR/USD on a 12M horizon is 1.05.

{kind=link}