Summary

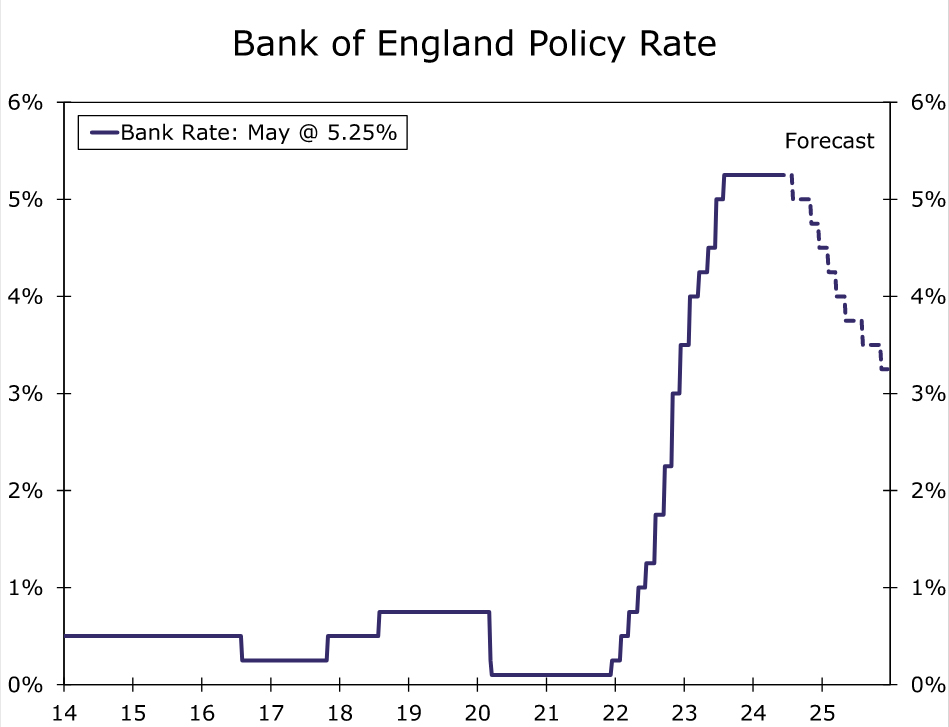

- The Bank of England (BoE) held its policy rate at 5.25% at today’s monetary policy announcement, but offered a dovish outlook that suggests rate cuts are now approaching.

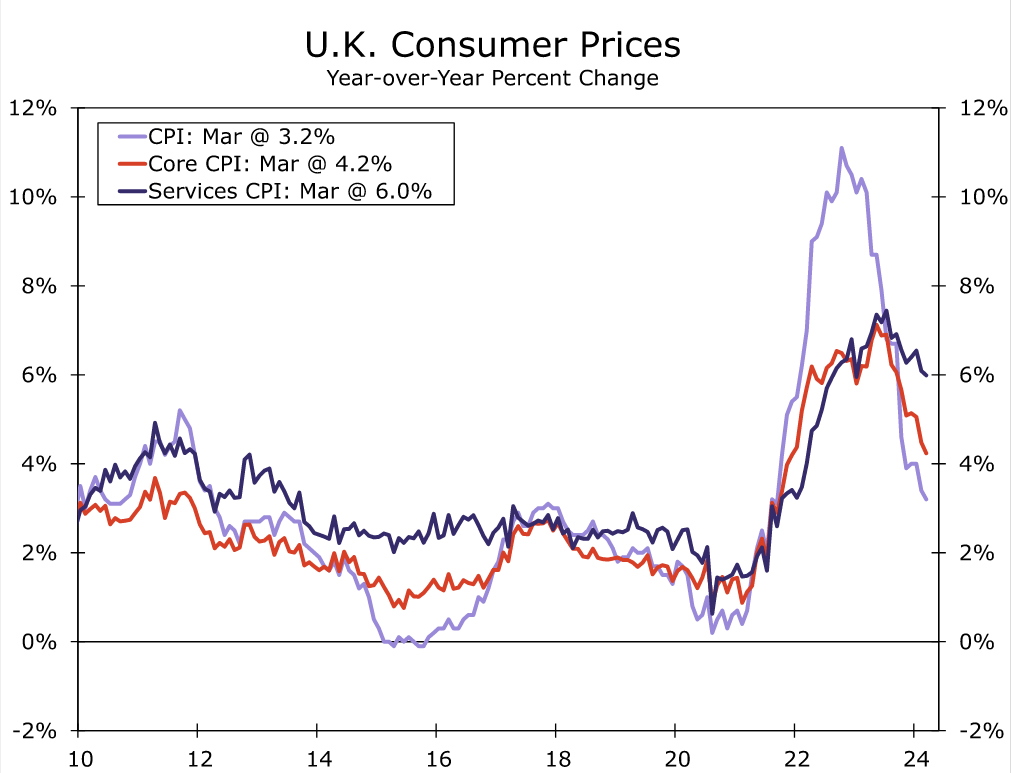

- The BoE said restrictive monetary policy is weighing on activity in the real economy, is leading to a looser labor market and is bearing down on inflationary pressures. That is reflected in the BoE’s updated economic projections. The inflation forecast of 1.9% in two years’ time suggests the BoE is very close to easing, in our view, while the inflation forecast of 1.6% in three years suggests the BoE might lower interest rates more quickly than markets currently expect.

- A June rate cut would likely require consistently favorable price and wage data, and for three more BoE policymakers to switch their vote from “hold” to “cut” within one meeting. While those outcomes are possible, they are perhaps not probable. For now, therefore, we remain comfortable with our current outlook which sees the Bank of England delivering an initial 25 bps rate cut to 5.00% at its August meeting, an outcome that is fully priced by market participants. We also forecast 25 bps rate cuts in November and December, for a cumulative 75 bps of easing this year, more than the 60 bps currently reflected in market pricing.

Bank of England Holds Steady, Offers A Dovish Outlook

The Bank of England (BoE) held its policy rate steady at 5.25% at today’s monetary policy announcement, an outcome that was unanimously expected by economists. While the Bank of England did not explicitly signal near-term easing in its accompanying statement, there were several dovish elements that suggest rate cuts are approaching. For now, we maintain our call for an initial 25 bps BoE rate cut in August, while acknowledging that the risk of an earlier June move has increased.

Among the key elements of the Bank of England’s announcement:

- the restrictive stance of monetary policy is weighing on activity in the real economy, is leading to a looser labor market, and is bearing down on inflationary pressures.

- key indicators of inflation persistence are moderating broadly as expected, although they remain elevated.

- importantly, the BoE repeated that “monetary policy will need to remain restrictive for sufficiently long to return inflation to the 2% target sustainably in the medium term” and that it “will keep under review for how long Bank Rate should be maintained at its current level.”

- policymakers voted 7-2 to hold rates steady compared to the 8-1 vote split at the previous meeting. A second policymaker joining the rate cut camp represents a dovish development.

The Bank of England’s updated economic projections are also informative, in our view. Based on market-implied interest rates, the BoE sees inflation slowing close to 2% in Q2-2024 before rebounding close to around 2.5% later this year. The BoE forecasts inflation at 1.9% in two years’ time, and 1.6% in three years. The forecast of inflation close to target in two years suggests to us that the BoE is very close to beginning its rate cut cycle, while the forecast of below-target inflation in three years suggests the BoE may lower interest rates more quickly than markets currently anticipate.

The overall dovish message was reinforced by BoE Governor Bailey who said he was optimistic things are moving in the right direction, that more evidence was needed regarding inflation staying low before a rate cut, and that he expected inflation to fall close to target in the next two months. Bailey said that a June rate cut is not ruled out or a done deal, and more broadly that interest rates may fall more sharply than markets expect.

In terms of reviewing how long the policy rate should stay at its current level, the Bank of England said it will continue to monitor closely indications of persistent inflationary pressures and resilience in the economy as a whole, including a range of measures of the underlying tightness of labor market conditions, wage growth and services price inflation. In that context, we expect the key upcoming U.K. data releases ahead of the Bank of England’s next monetary policy announcement on 20 June will be March wage data (14 May), April CPI (22 May), April wage data (11 June) and the May CPI (19 June). Should those wage and price data prove to be consistently favorable, which is clearly a distinct possibility, we expect the Bank of England would be comfortable beginning a rate cut cycle in June. That said, U.K. price and wage data have had some tendency to disappoint during the current disinflation process. Moreover, a June rate cut would require three policymakers to switch their vote from “hold” to “cut” within one meeting, a not insignificant shift. For now, therefore, we remain comfortable with our current outlook which sees the Bank of England delivering an initial 25 bps rate cut to 5.00% at its August meeting, an outcome that is fully priced by market participants. We also forecast 25 bps rate cuts in November and December, for a cumulative 75 bps of easing this year, more than the 60 bps currently reflected in market pricing. That outlook is also consistent with the Bank of England’s signal that rates might be lowered more quickly than markets expect.

held its policy rate steady at 5.25% at today's monetary policy announcement, an outcome that was unanimously expected by economists. While the Bank of England did not explicitly signal near-term easing in its accompanying statement, there were several dovish elements that suggest rate cuts are approaching. For now, we maintain our call for an initial 25 bps BoE rate cut in August, while acknowledging that the risk of an earlier June move has increased.){kind=link}