U.S. Highlights

- The Federal Reserve Senior Loan Officer Opinion Survey showed that most banks tightened lending standards further in the first quarter, with demand for loans falling in concert.

- Growth in U.S. consumer credit slowed materially in March as the upward trend in rates through the first quarter weighed on volumes.

- Federal Reserve officials reiterated their expectations that interest rates would need to remain higher for longer to ensure inflation returns sustainably to their 2% target.

Canadian Highlights

April’s jobs report defied expectations with the largest job gain in 15 months. Equally strong labour force growth left the unemployment rate steady. This supports our view that the Bank of Canada can wait until July to cut interest rates.

The Bank of Canada’s Financial Stability Report noted ongoing concerns about debt serviceability amidst high interest rates and renters experiencing high delinquency rates.

The economic challenges are more acute for small businesses, where insolvencies have risen due to higher borrowing costs, slower economic activity and the end of pandemic support.

U.S. – Credit Conditions Tighten as Fed Remains Vigilant

After last week’s Federal Reserve decision and employment report, the second week of May was comparatively lighter on data releases. First quarter reports for lending activity and consumer credit showed that tighter lending standards continue to weigh on credit demand. However, financial markets were more attentive to the comments of Federal Reserve officials as they sought insights on the potential path of monetary policy moving forward. As of the time of writing, the S&P 500 was up 2.1% on the week, while Treasury yields were roughly unchanged.

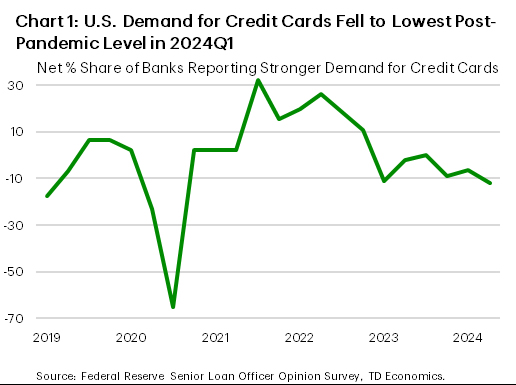

Starting things off on Monday, we received the updated Federal Reserve Senior Loan Officer Opinion Survey (SLOOS) for the first quarter. Survey responses showed that banks continued to tighten lending standards and report weaker demand for loans across all business and consumer loan categories. Relative to the fourth quarter of 2023, more banks tightened lending standards for consumer credit, fewer tightened commercial and residential real estate credit, and roughly the same number of banks tightened commercial & industrial credit. Within consumer credit, tighter lending standards pushed the net share of banks reporting stronger demand for credit cards to its lowest level since mid-2020 (Chart 1).

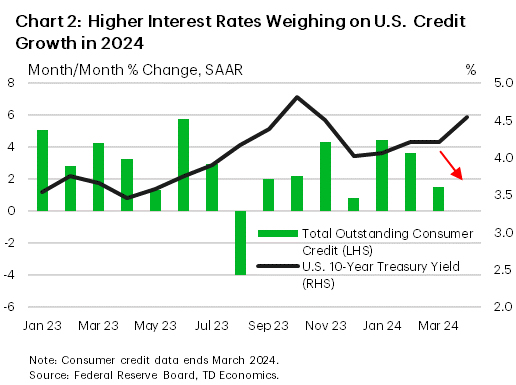

Looking at the monthly breakdown for consumer credit, the March data showed consumer credit growth decelerated considerably through the first quarter as interest rates trended higher (Chart 2). While consumer credit still expanded 3.2% (annualized) in the first quarter, the gains were largely front-loaded in the earlier months and tapered off as financial conditions tightened. With interest rates continuing to push higher through the first half of the second quarter, it seems likely that a further softening in consumer credit growth will occur over the coming months. Combined with depleted pandemic excess savings, weakening consumer credit growth is expected to lead to moderating consumption growth in 2024. While this should aid the Federal Reserve in their attempts to return inflation to their 2% target, officials emphasized their vigilance in recent remarks.

Vice Chair and New York Fed President John Williams noted this week that monetary “policy is in a very good place, and we have the time to collect more [data], so steady as she goes”. This sentiment was echoed by Richmond Fed President Barkin who stated his optimism that “today’s restrictive level of rates can take the edge off demand in order to bring inflation back to our target”. Most members noted that they did not expect further policy tightening to be necessary, with Minneapolis Fed President Kashkari stating that “the bar for us raising is quite high, but it’s not infinite”. While the prospect for higher rates is unlikely at this time, Fed officials are expected to remain vigilant against the potential for upside risks to inflation.

April’s Consumer Price Index report next week will offer the next barometer on inflation trends as the Fed prepares to update their Summary of Economic Projections ahead of their next meeting on June 11-12th.

Canada – Jobs Surge Delays Rate Cut Bets

This week’s economic update is centered on the jobs report released earlier today. April saw an unexpectedly large gain of 90k jobs, but since the labour force expanded by an equally substantial amount, the unemployment rate held steady. Wage growth slowed relative to March but was slightly above the consensus estimate. The Canadian dollar saw an uptick on the news as markets pared back bets on the extent of rate cuts this year.

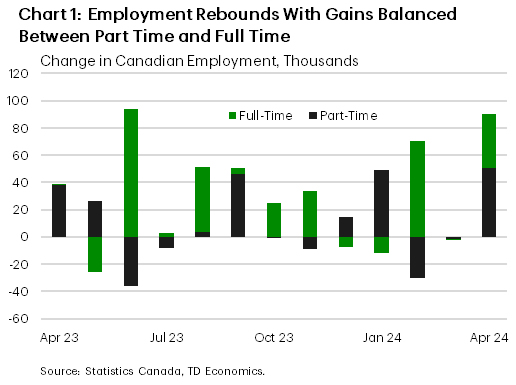

Today’s employment surge exceeded expectations by a sizeable margin after March’s setback, marking the largest gain in 15 months. Notably, the jump was driven by the private sector and with relatively balanced gains between part-time and full-time employment (Chart 1). This signals robust second quarter GDP potential, contrary to consensus forecasts. Such labour market strength may heighten inflation concerns, potentially influencing consumer spending and complicating the Bank of Canada’s (BoC) strategy.

The blockbuster jobs report makes the BoC’s annual Financial Stability Report (FSR), which typically focuses attention on risks to the financial system, seem less worrisome. However, the unemployment rate has risen above the pre-pandemic average. The FSR highlighted that unforeseen increases in unemployment as a potential risk that could destabilize the currently smooth transition to higher interest rates. The Bank continues to express concerns regarding debt serviceability, especially as borrowers face renewals at higher rates.

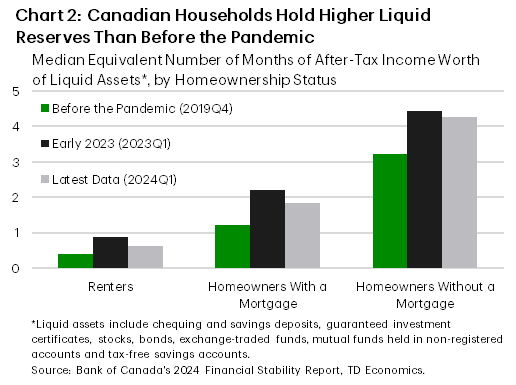

As it stands today, renters are a particularly vulnerable group. They are experiencing elevated delinquency rates, with the Senior Deputy Governor pointing out that high inflation over the past few years have strained budgets. The good news is that Canadian households still have “financial flexibility” in the form of liquid reserves that could help them absorb higher mortgage payments or cushion them in case of an economic downturn (Chart 2).

Chart 1 shows the month-on-month change in employment, broken down by full-time and part time jobs. April’s 90,400 change in employment was balanced between by part-time (+50,300) and full-time (40,100) gains.

The disparity between large and small businesses was also called out by the FSR, with smaller entities feeling the brunt of rising rates more severely. The recent spike in business insolvencies is concentrated among small businesses and partially reflects the phase out of pandemic support programs. Given that these businesses employed nearly 47% of Canada’s workforce in 2022, their struggles could impact the labor market.

At the press conference following the FSR release, Governor Macklem noted a still-healthy level of business creation within this segment but emphasized continued vigilance for signs of stress. When questioned about the possibility of an interest rate cut given these pressures, the Governor remained noncommittal. In light of today’s strong jobs gain, we continue to expect that the BoC can afford to wait until July to cut rates. Financial markets seem to have aligned with our view, with the inflation report on May 21st likely to be the next key influence on rate expecations ahead of the June 5th decision.

{kind=link}