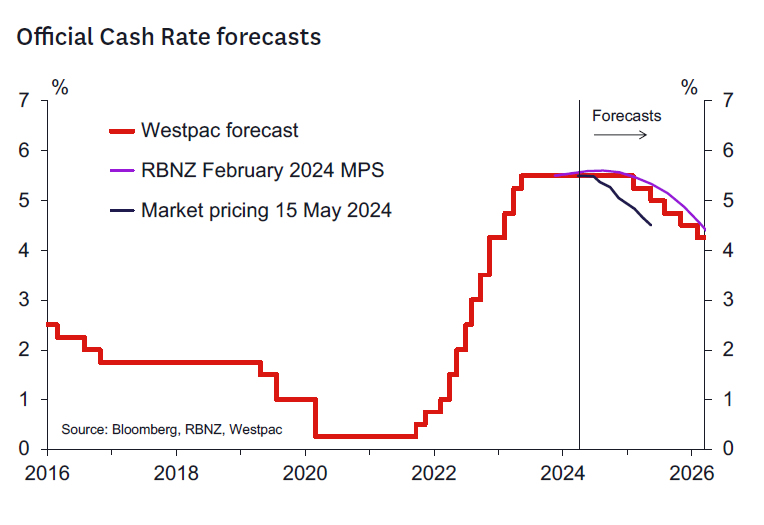

- We expect the RBNZ will leave the OCR at 5.5% at its May Monetary Policy Statement.

- The RBNZ will likely remain comfortable with the forward outlook communicated in the February Monetary Policy Statement.

- We don’t see a significant change in the RBNZ’s projections for the OCR – easing still looks like a 2025 affair.

- Weaker than expected GDP growth and numerous indications of a flat economy should trigger a downward adjustment in the 2024 growth profile.

- But the inflation outlook remains challenging as a non-tradables driven upward inflation surprise in Q1 2024 likely implies a still elevated near-term inflation outlook.

- Market views of OCR easing as early as October are unlikely to find support.

RBNZ decision and associated communication.

We don’t expect any significant change to the RBNZ’s “Watch, Worry and Wait” strategy it has been following since the May 2023 Monetary Policy Statement.

We expect the RBNZ to keep the OCR at 5.5% and reiterate its view that the OCR will need to remain at 5.5% for “a sustained period” to bring inflation back within the 1-3% target range. We expect the RBNZ to reiterate that while economic growth remains weak, inflation pressures remain elevated.

The RBNZ will continue to forecast inflation returning close to 2% by end 2025 contingent on a forward OCR profile as presented in the February Statement (which implied around a 40 percent chance of a further OCR increase in 2024 but an initial cut to the OCR to 5.25% by mid-2025).

Key developments since the February Monetary Policy Statement.

We noted at the time of the April Monetary Policy Review that relatively little data has come to light since the February Statement to disturb the RBNZ’s view on the inflation outlook. We think that the general tone of activity and sentiment data since the February meeting will have helped balance the very strong inflation data which indicate unexpectedly persistent inflation pressures. It’s likely still the case that there is little to support the idea that interest rates can be cut earlier than the RBNZ previously assumed (early to mid-2025). We think the RBNZ will be reluctant to reduce the pressure on the economy to adjust while inflation remains elevated.

Key developments since the February Statement have been:

- Slightly weaker Q4 2023 GDP (↓) and associated revisions. GDP growth in Q4 was slightly weaker than forecast (-0.1%q/q vs 0% forecast) and cumulative revisions mean that the economy was 0.2% smaller than forecast. This will likely reduce the RBNZ’s starting point output gap very modestly.

- Weak forward indicators for GDP growth in H1 2024 (↓↓). Retail spending indicators remain weak, and the PMIs, business and consumer confidence have taken a step lower after a boost in January and February 2024. It’s plausible the RBNZ will be looking at revising down their 2024 growth projection (1.6%y/y for 2024) to better reflect the current apparently weak growth momentum. Treasury have also indicated they have revised down their growth forecasts in recent months.

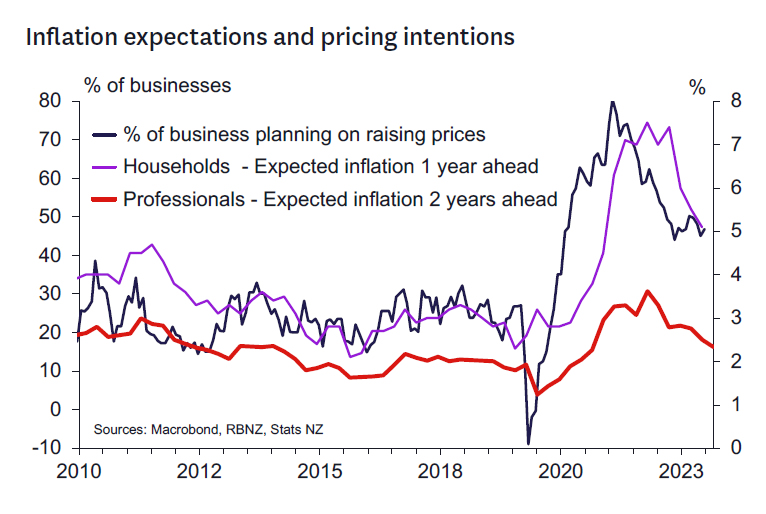

- Lower business inflation expectations but still elevated household inflation expectations and sticky price intentions indicators (→?). The RBNZ will have been encouraged by falling inflation expectations – especially in the April 2024 business survey – which show inflation expectations either at or very near long term average levels (the more important household survey will be available immediately before the MPC meets and is still quite elevated). On the other hand, pricing intentions indicators remain sticky and not consistent with sub-3% inflation. The record of meeting in the April Review indicated the MPC would need to see all these indicators at more normal levels to be comfortable with policy easing – even with headline inflation below 3%.

- A slightly weaker labour market in Q1 (→). The unemployment rate printed 0.1% higher than forecast and the Labour Cost Index was in line with projections.

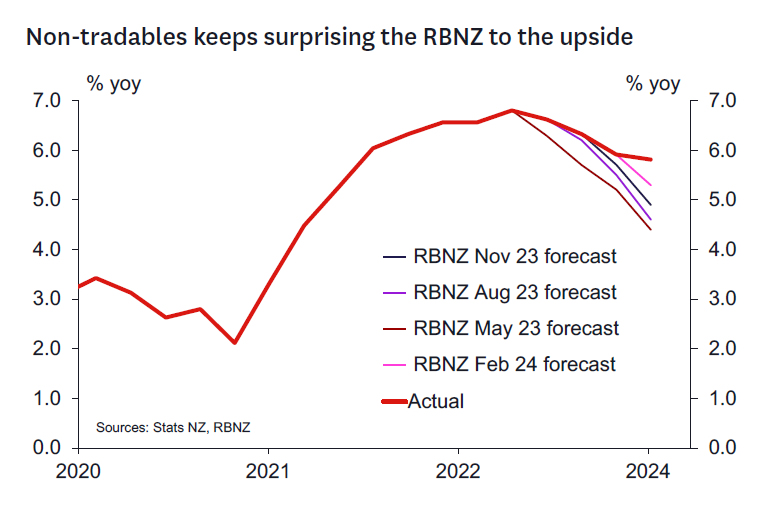

- Stronger CPI inflation components (↑↑). the RBNZ forecast a low 0.4% quarterly outcome for the Q1 CPI (3.8% y/y) in its February Statement versus the outcome of 0.6% for the quarter (4.0% y/y). Importantly, non-tradable inflation drove the forecast miss (1.6% q/q vs 1.1% q/q forecast by the RBNZ) indicating the potential for more persistent inflation looking ahead.

- Higher oil prices (↑) – Oil prices are around 4% higher than the level assumed for Q2 2024 in the February Statement (Dubai spot oil at USD 80.80) which will lift the RBNZ’s near-term CPI forecasts, all else equal.

- Weaker terms of trade in Q4 2023 (↓) – these data came in notably weaker than expectations, although in large part this reflects timing effects that will likely unwind in coming quarters.

- A lower NZD TWI (↑) – the TWI is now around 1.5% below the H1 24 level that had been assumed. The lower exchange rate probably broadly balances the impact of the weaker terms of trade.

The RBNZ’s formal projections will continue to be based on those in the Treasury’s Half Year Economic and Fiscal Update (HYEFU) as Budget 2024 is not tabled until 30 May. That said, the Treasury will have briefed the RBNZ on the key macro features of Budget 2024, so any deviations from expectations will feed into the rhetoric the RBNZ chooses to describe the policy outlook.

It is worth recalling that the February Statement included a special topic in which the RBNZ reached a preliminary verdict on the impact of the Government’s proposed policies on monetary policy. The RBNZ’s analysis concluded that it was unclear whether the net effect of the new Government’s policies would be inflationary or deflationary. As we don’t expect any big surprises in Budget 2024, the RBNZ should continue with this line in the May Statement.

We anticipate that a more definitive quantitative assessment of the impact of Budget 2024 on the RBNZ’s projections will occur in the August Statement. By then, Budget 2024 will be public and the reaction of the economy to government policy changes – such as the income tax cuts and investor housing policy – will be clearer.

The communications objective.

We think the RBNZ will be happy with the current level of financial conditions. Markets have backed off the nearterm easing expectations they held early in 2024 but similarly are not pricing in OCR increases either. They will want the market to respond to the data – especially the inflation data – that emerges over the next 6 months. We don’t think they will want to give the market a sense that their strategy has changed from that of holding the OCR at current levels for the foreseeable future.

We also don’t think the RBNZ will want to fan expectations of near-term policy easing (as we think they will want to see a couple of quarters of well-behaved inflation data at the very least before considering moving to a less restrictive stance). In the April Review the RBNZ signalled that their views hadn’t changed much by issuing a very short press release. We see similar potential this time around.

The bottom line is that we are not expecting significant shifts to the RBNZ’s projections for the OCR. In February, these had been reduced slightly but still implied a 40% chance of an OCR increase in 2024. We think the mix of weaker activity indicators, but still-strong domestic inflation will leave the RBNZ in a similar space. Hence there will be more of the “Watch, Wait and Worry” message this time around.

Scenarios.

We see three main scenarios:

- Baseline case (70% probability): the RBNZ retains a similar OCR track as in the February MPS i.e., a peak OCR in Q3 consistent with 40% chance of an OCR increase to 5.75%. The forward profile in 2025 would also be similar with current persistence in domestic inflation balanced by weaker growth.

- Hawkish case (20% probability): the OCR profile returns to where it was in November 2023 which implied around a 75% chance of a rate hike in Q3 2024. This would occur if the RBNZ concludes that domestic inflation is sufficiently sticky such that a return of inflation close to 2% in 2025 now looks remote (for example moving in the direction of the hawkish scenario depicted in our recent Hawks and Doves note that showed a scenario where recent upside surprises to non-tradables inflation continue leaving overall inflation at a low of 2.7%y/y in late 2025).

- Dovish case (10% probability): the RBNZ downgrades its outlook for growth and dismisses concerns about non-tradable inflation concerns. The OCR profile shifts to bring forward an easing to Q1 2025. The earlier start to easing could imply an OCR at 4.5% by year end 2025. This would occur if the RBNZ is confident that weak growth momentum and a widening output gap will generate lower nontradable inflation outcomes as the year progresses. The RBNZ would implicitly leave open the possibility of a November easing should their expected low nontradable CPI outcomes eventuate in Q2 (data released July) and Q3 (data released October) and if further downside risks to growth emerge.

{kind=link}