Tuesday November 7: Five things the markets are talking about

It’s a very light week for the economic calendar.

In the U.S, today’s JOLTS data will update job openings, which have been far exceeding hiring’s. This is strong evidence that the U.S economy is at full employment.

Aside from a couple of central bank speeches (BoE’s Carney 12:55 pm EDT and Fed Chair Yellen at 2:30 pm EDT), investors’ focus returns to geopolitics as President Trump continues his tour of Asia and Saudi Arabia’s ongoing crackdown on corruption.

The U.S. president is currently in S. Korea for the second leg of his five-nation Asia trip, with North Korea’s nuclear threat at the heart of his agenda, which includes a bilateral meeting and joint press briefing with President Moon Jae-in and an address to South Korea’s parliament.

1. Stocks record highs continue

Continued optimism over the prospect of U.S tax reform is feeding into global sentiment.

In Japan, the Nikkei index jumped to a near 26-year-high overnight, as foreign investors piled in on expectations of strong earnings from Japanese corporations, while Wall Street’s strength supported this sentiment. The Nikkei share average closed +1.7% higher, while the broader Topix rallied +1.2%.

Down-under, commodities helped drive the Aussie stock indexes through its 2015 highs overnight. The S&P/ASX 200 rose +1%. While in South Korea, the market pulled back a bit further as Trump arrived. Early gains had faded and the Kospi closed out down -0.2%.

In Hong Kong, stocks hit a decade high on global optimism. The Hang Seng index rose +1.4%, while the China Enterprises Index gained +1.1%.

In China, blue chips scale a two- high, banking and energy firms lend support. The blue-chip CSI300 index rose +0.9%, the highest level since August 2015, while the Shanghai Composite Index closed up +0.7%.

In Europe, regional indices trade mixed coming off the earlier highs after a strong showing in Asia. Corporate earnings remain the dominant theme.

U.S stocks are set to open little changed (Flat).

Indices: Stoxx600 flat at 396.6, FTSE -0.2% at 7551, DAX +0.2% at 13491, CAC-40 flat at 5508, IBEX-35 -0.3% at 10291, FTSE MIB +0.2% at 23036, SMI -0.3% at 9258, S&P 500 Futures flat

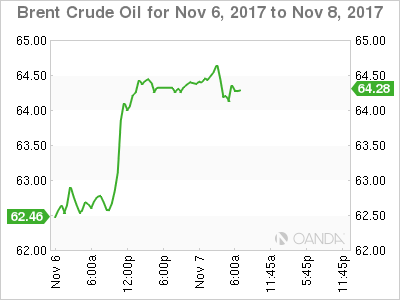

2. Oil hits highest level in two-years, gold lower

Oil prices hit their highest levels since July 2015 overnight as markets tightened, while Saudi Arabia’s crown prince tightened his power through an anti-corruption crackdown that included high-profile arrests.

Brent crude futures are currently down -19c at +$64.08, having closed +3.5% higher yesterday, marking the biggest percentage gain in about six weeks. U.S West Texas Intermediate (WTI) crude is down -7c at +$57.28 a barrel.

Saudi Crown Prince Mohammed bin Salman has tightened his grip on power through an anti-corruption purge by arresting royals, ministers and investors. In the short term, no immediate change is expected in the oil policy of Saudi Arabia, which is the world’s biggest exporter of crude oil. The Prince seems strongly committed to anchoring the OPEC agreement deep into 2018.

Elsewhere, there are ongoing signs of tightening market conditions. In the U.S, energy companies cut eight oilrigs last week, to 729, in the biggest reduction since May 2016. While there seems to be growing consensus amongst OPEC members to extend their pledge to hold back about -1.8m bpd beyond next March’s deadline.

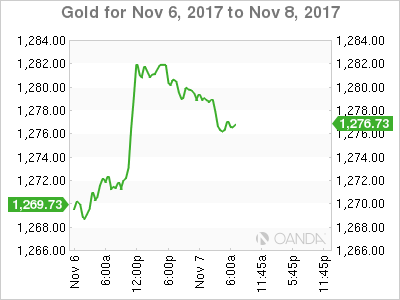

Ahead of the U.S open, gold prices have inched down as investors sell the ‘yellow’ metal to lock in some profits after it gained nearly +1% in yesterday’s previous session on safe-haven buying following concerns over the arrests of some Saudi royal family members and ministers on corruption charges. Spot gold is down -0.2% at +$1,278.75 per ounce.

3. Sovereign yields in a tight range

NY Fed President Dudley (FOMC voter) is to retire in mid-2018 (as speculated over weekend). His 10-year term was scheduled to end in Jan 2019 and it now leaves four potential vacancies in 2018.

President Trump announced last week that Fed Governor Jerome Powell would be nominated to replace Janet Yellen when her term expires in February.

Note: Vice-Chairman Stanley Fischer retired in mid-October.

The yield on U.S 10-years has fallen-1 bps to +2.32%, the lowest in more than two weeks. In Germany, the 10-year Bund yield fell -2 bps to +0.34%, the lowest in eight weeks, while in the U.K, the 10-year Gilt yield declined – 2bps to +1.245%, the lowest in more than seven weeks.

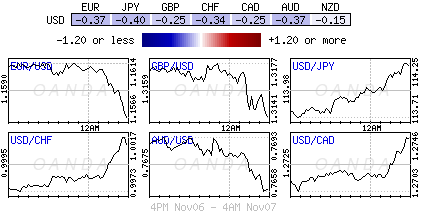

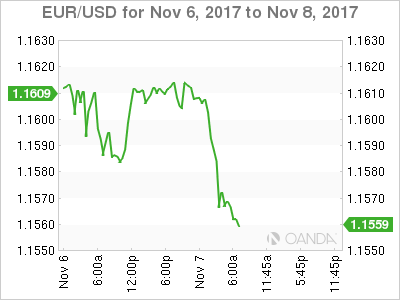

4. Dollar rises on Tax optimism

The ‘mighty’ USD continues to find support aided by investor optimism over the prospect of U.S tax reform. The EUR/USD hit a four-month low as the pair tested below €1.1570 as dealers cited low euro zone bond yields as one factor weighing upon the ‘single’ unit.

Note: Last month’s the ECB decided to extend bond buying until at least September 2018, while the Fed by contrast is expected to raise interest rates next month.

USD/JPY is trading North of ¥114.25 aided by the highest close in the Nikkei in over 25-years.

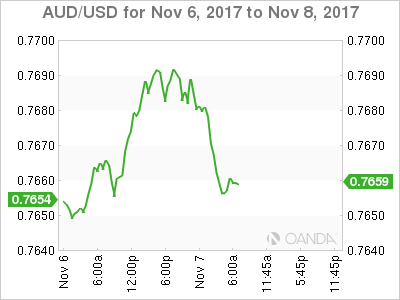

Down-under, the AUD (A$0.7656) ultimately weakened after last nights RBA statement. As expected, they left the O/N Cash Rate Target unchanged at +1.50%. Rates are continuing to support the economy, but higher exchange rate is expected to contribute to continued subdued price pressures – inflation is likely to remain low for some time. The RBA remains in wait-and-see mode.

5. Eurozone retail sales stronger than expected

Data this morning shows that Eurozone retail sales came in stronger than expected in September, up +0.7% on the month and +3.7% on the year.

Digging deeper, there was also a big revision that left July and August essentially flat, having previously been quite a bit lower.

Today’s print is further proof that consumer spending is once again supporting robust growth in Q3. However, despite a long period of rising spending, there are as yet few signs of a sustained pickup in inflation, which again is confounding most Tier I Central Banks.