Summary

- The first half of 2024 has seen a gradual, but clearly perceptible, improvement in U.K. economic momentum. Q1 GDP rose 0.7% quarter-over-quarter, while more recent sentiment and activity data point to ongoing growth in Q2. The outlook for the U.K. consumer continues to improve, although the outlook for U.K. businesses is perhaps not quite as robust. Overall, however, we see U.K. GDP growth firming to 0.8% in 2024 and 1.5% in 2025, from just 0.1% in 2023.

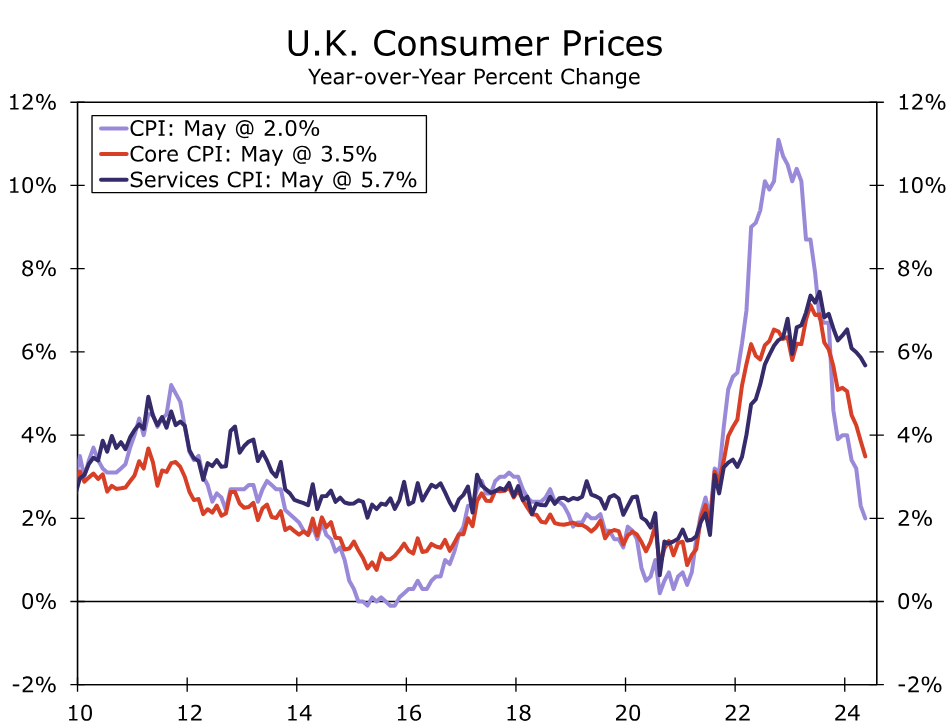

- The progress on the disinflation front arguably remains mildly frustrating. While headline inflation slowed to the Bank of England’s (BoE) 2% target in May, underlying inflation measures and wage growth have slowed more gradually, and remain elevated by historical standards. Given still-elevated wage and price trends, we expect the BoE will initially proceed cautiously with its monetary easing.

- We see just two 25 bps rate cuts this year, in August and November, and forecast the BoE’s policy rate to end 2024 at 4.75%. We expect a slightly faster pace of easing in 2025 as underlying inflation returns closer to the central bank’s 2% inflation target. Altogether, we see a further cumulative 125 bps of BoE policy rate cuts in 2025, which would see the central bank’s policy rate end next year at 3.50%.

- The Labour Party led by new Prime Minister Keir Starmer won a landslide victory in last week’s election, securing 412 of the 650 seats in the House of Commons. Despite the landslide victory, we do not anticipate a significant impact on the U.K. economy or financial markets in the immediate period ahead. Should the new government be more cautious than expected on the fiscal front, it could if anything be less supportive of the growth outlook in 2025 than generally expected.

U.K. Shows More Encouraging Economic Growth Trends

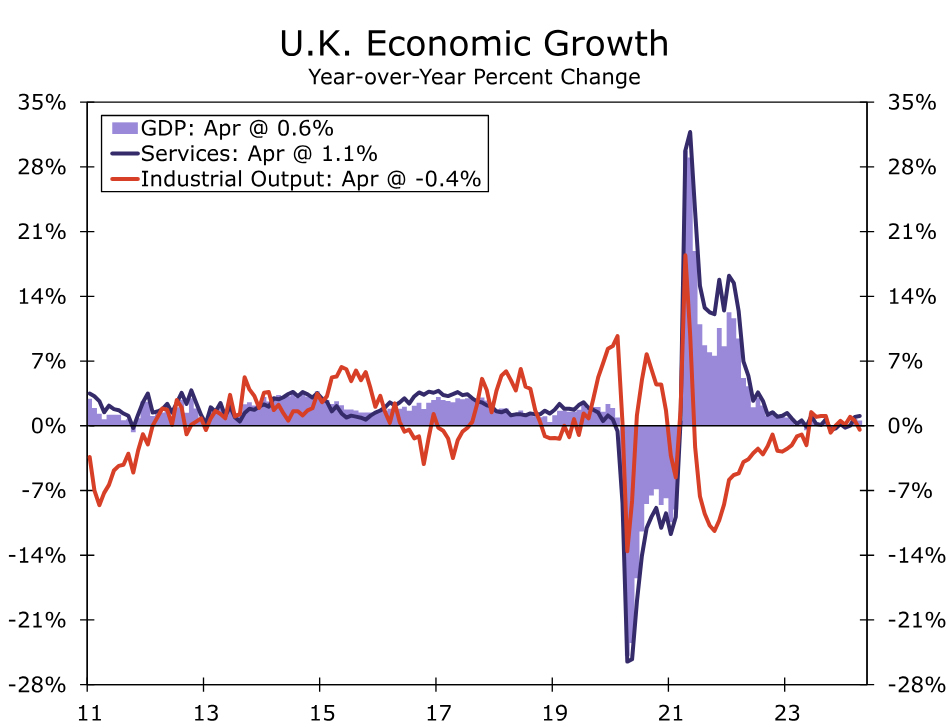

The first half of 2024 has seen a gradual, but clearly perceptible, improvement in U.K. economic momentum. After a mild technical recession in the second half of last year as GDP contracted for two straight quarters, the United Kingdom returned to a positive growth path early this year as Q1 GDP jumped 0.7% quarter-over-quarter and rose by 0.3% year-over-year. Among the details, the composition of first quarter growth was also somewhat encouraging and led mainly by the private sector, as private consumption rose 0.4% quarter-over-quarter and business investment rose 0.5% quarter-over-quarter.

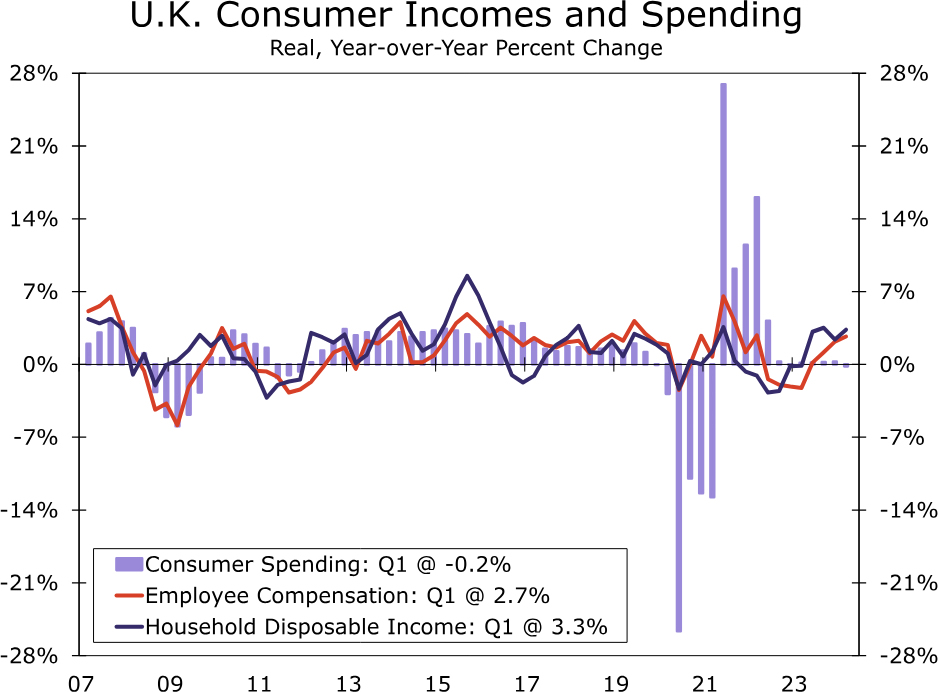

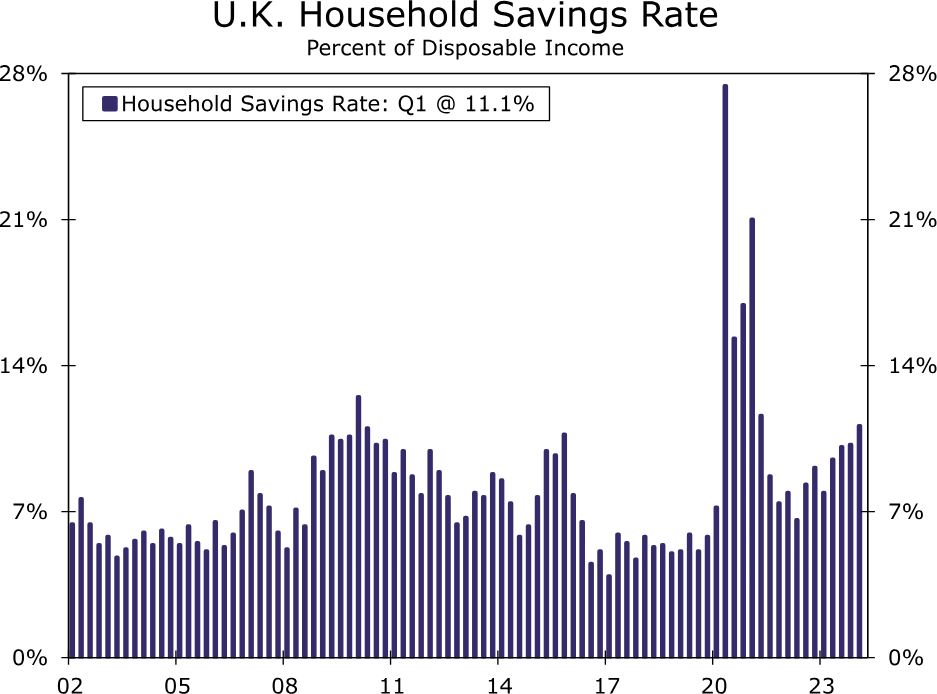

The outlook for the U.K. consumer in particular continues to improve. While wage growth has slowed moderately over the past several months the pace of wage growth is still elevated by historical standards. As a result, real household disposable income growth firmed further in Q1-2024 to 3.3% year-over-year, near the high for the post-pandemic upswing. The household saving rate also rose to 11.1% of disposable income, indicating that consumers have something of a buffer to support spending going forward. The main cautionary note for the consumer is the impact of the Bank of England’s past monetary tightening, which has seen interest costs rise to 5.8% of disposable income by Q1-2024, up from just 1.4% of income in Q3-2021, before the Bank of England rate hike cycle began. In contrast to the consumer, the outlook for U.K. business is perhaps not quite as robust. In Q1-2024, the gross operating surplus of U.K. private non-financial corporates fell 9.2% year-over-year. That actually exceeded the largest decline seen during the pandemic and, indeed, is the largest fall in the U.K. gross operating surplus since Q4-2009, surrounding the global financial crisis. The same elevated wage growth—relative to inflation—that is supporting the consumer outlook could be weighing on corporate margins and business profitability, likely a restraining factor for business investment through the rest of 2024. That said, we believe consumer optimism will likely outweigh corporate caution as an economic driver over the next several quarters. We forecast U.K. GDP growth of 0.8% in 2024 and 1.5% in 2025, up from just 0.1% in 2023.

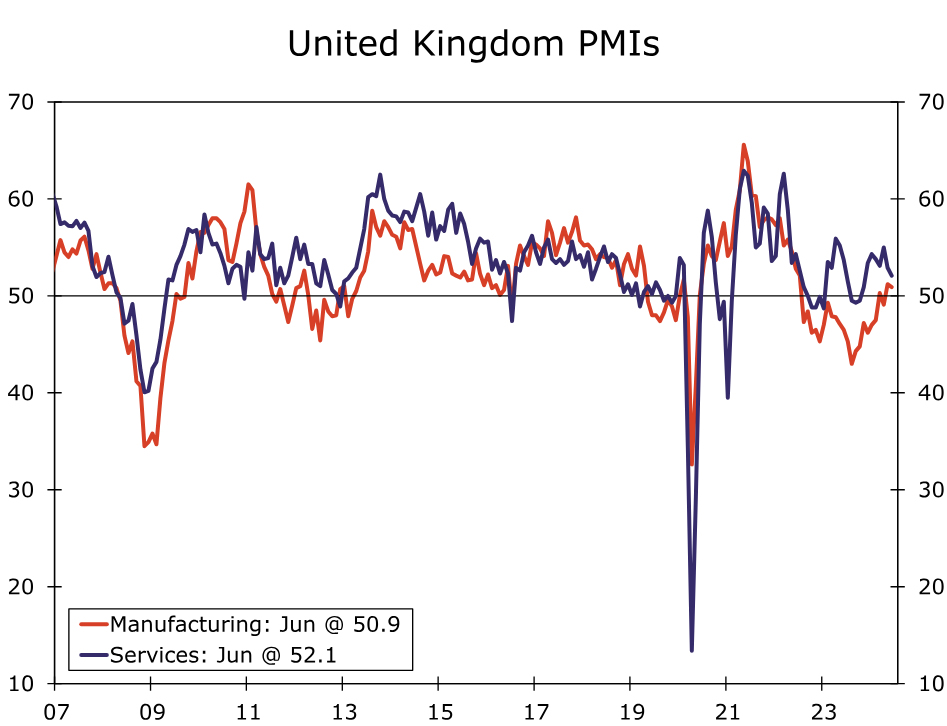

Certainly, economic figures from more recent months suggest a gradual U.K. economic upswing has continued. April GDP was unchanged on the month, holding steady after the large 0.4% gain seen in March. April services activity rose 0.2% month-over-month, on top of the 0.5% gain seen in March, while industrial output fell 0.9% month-over-month. The steady overall GDP result means U.K. April GDP is around 0.4% above its Q1 average, indicating the economy is on track for another quarter of positive growth. Sentiment surveys, while mixed, are also consistent with ongoing expansion. The U.K. services PMI fell for a second month in June to 52.1, but remains above the breakeven 50 level that indicates continued service sector growth. Meanwhile, the June manufacturing PMI also eased slightly to 50.9, but is also at a level consistent with expansion in the manufacturing sector. Finally, while the labor market appears to be softening with employment down by 139,000 for the February-April period compared to the November-January period, there remain some questions about the robustness of the labor market figures given the low survey response rates of late.

U.K. Inflation Concerns Still Lingering

While progress on the economic recovery front has perhaps been a bit more encouraging than expected, the progress on the disinflation front arguably remains mildly frustrating. The latest CPI reading, for May, did show a deceleration in headline inflation to 2.0% year-over-year, matching the Bank of England’s (BoE) inflation target. That deceleration has however been concentrated in goods prices, which fell 1.3% year-over-year in May. Measures of underlying inflation have shown slower progress toward the central bank’s target. Core inflation, which excludes food, energy, alcohol and tobacco, rose 3.5% in May, still some way above the central bank’s target. And services inflation remains stubbornly persistent, rising 5.7% in May, above both the consensus and BoE forecast.

Concerns about sticky services inflation are reinforced by still-elevated wage growth. The latest wage data showed average weekly earnings holding steady at 5.9% year-over-year in the three months to April, and average weekly earnings excluding bonuses holding steady at 6.0%. Another measure closely followed by Bank of England policymakers, private sector regular average weekly earnings, eased only marginally to 5.8%. While pay growth has slowed from its peak, all of these wage growth measures remain above levels that prevailed prior to the pandemic and, for now, are also higher than generally viewed as consistent with sustainably achieving the BoE’s 2% inflation target.

It is against this backdrop of gradually improving economic growth and gradually receding inflation that we believe the Bank of England will proceed cautiously in moving to a less restrictive monetary policy stance. To be sure, central bank policymakers have offered hints that it might start lowering interest rates soon. The BoE held its policy rate steady at 5.25% in June, but offered several comments that suggested an inclination to ease monetary policy:

- It said the recent strength in services inflation was due in part to prices that are index-linked or regulated, which are typically changed only annually, and volatile components.

- Key indicators of inflation persistence have continued to moderate, although they remain elevated.

- As part of the August forecast round, members of the Committee will consider all the information available and how this affects the assessment that the risks from inflation persistence are receding. On that basis, the Committee will keep under review for how long Bank Rate should be maintained at its current level.

Given those hints from policymakers, and so long as upcoming data suggest some moderation in wage and price growth, our view remains for the BoE to deliver an initial 25 bps policy rate cut to 5.00% at the August monetary policy meeting. Given still-elevated wage and price trends, we expect the BoE will initially proceed cautiously thereafter. We expect the BoE to pause in September, reduce its policy rate by 25 bps in November, and to pause again in December, for a cumulative 50 bps of rate cuts this year, which would see the policy interest rate end 2024 at 4.75%. We expect a slightly faster pace of easing in 2025 as underlying inflation returns closer to the central bank’s 2% inflation target. Altogether, we see a further cumulative 125 bps of BoE policy rate cuts in 2025, which would see the central bank’s policy rate end next year at 3.50%. We view the risks around our forecast for the Bank of England policy rate as broadly balanced for 2024, but tilted toward a faster pace of easing in 2025 if wage and inflation trends were to slow more convincingly. Against this backdrop we anticipate only modest gains in the pound over the medium-term even if, as we forecast, the U.S. economy slows and the Fed eases monetary policy.

U.K. Election Should Have Limited Initial Impact On Economy And Markets

Last week also saw a historic election, as the Labour Party led by new Prime Minister Keir Starmer defeated the outgoing Conservative government in a landslide. Labour secured 412 of the 650 seats in the House of Commons, with the Conservative Party securing just 121 seats, their worst ever performance. Among the other parties to secure seats in parliament were the Liberal Democrats (72 seats), Scottish National Party (9 seats) Sinn Fein (7 seats) and Reform UK party (5 seats).

Despite the landslide victory by the Labour party, we do not anticipate a significant impact on the U.K. economy or financial markets in the immediate period ahead. Labour has suggested they wish to remain outside the Single Market and Customs Union, suggesting any significant re-working of the Brexit deal is unlikely. Labour has announced policy proposals that would entail increased spending, such as reducing National Health Service wait times or recruiting new teachers, but has also announced accompanying plans on how those policies would be funded. Moreover, Labour has also pledged to stand by the fiscal rule that public debt as a share of GDP should be falling over a five-year horizon.

Should Labour honor its pledge to stick within these fiscal parameters, we see limited room for significant fiscal expansion. In addition, it could take some time for the new government to fully formulate any increases in spending or revenue plans. For these reasons, we suspect the immediate impact on financial markets will be limited. In fact, should these fiscal parameters prompt the new government to be more cautious than expected on the fiscal front, perhaps through unexpected tax increases or if it shows particular discipline with respect to any spending increases, it could if anything be less supportive of the growth outlook in 2025 than generally expected. While our view of initially cautious Bank of England monetary easing would remain unchanged, any unexpected fiscal caution on the part of the new government in 2025 could potentially reinforce the direction of risks toward a faster pace of rate cuts next year.

2% target in May, underlying inflation measures and wage growth have slowed more gradually, and remain elevated by historical standards. Given still-elevated wage and price trends, we expect the BoE will initially proceed cautiously with its monetary easing.){kind=link}