Thursday November 9: Five things the markets are talking about

With little data on the docket this week investor’s attention has focused on Asia, where Trump has embarked on an 11-day tour.

Overnight, it was no surprise that Trump said China is taking advantage of U.S workers and companies with unfair trade practices, but he managed to blame his predecessor rather than China for allowing the massive U.S. trade deficit to grow.

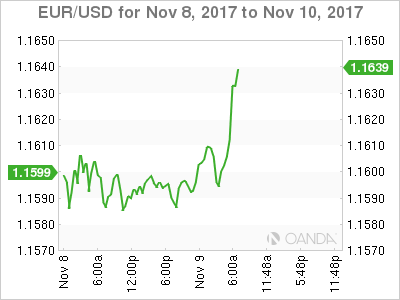

Elsewhere, Brexit talks resume this morning in Brussels with no indication that a breakthrough is anywhere close, while stateside, tax reform discussions remain ongoing and the broad uncertainty around the bill has the ‘mighty’ dollar again under pressure.

Note: E.U officials are said to be planning for a ‘no deal’ on Brexit or reversal of the decision before 2018 amid U.K PM May’s more ‘fragile’ leadership position.

1. Stocks wild swings

In Japan, equities ended down overnight after intraday swings took the Nikkei and Topix indexes to multi-decade highs only to plummet in afternoon trading. The Nikkei ended down -0.2%, while the broader Topix lost -0.3%.

In Hong Kong, stocks hit another decade-peak Thursday, with investor sentiment underpinned by China’s strong inflation data that pointed to economic resilience. The Hang Seng index rallied +0.8%, while the China Enterprises Index jumped +1.5%.

In China, regional stocks rose on Thursday, led by the blue-chip index scaling a fresh two-year high, as investors were encouraged by strong inflation data that showed economic momentum remains robust. The blue-chip CSI300 index rose +0.7%, while the Shanghai Composite Index closed up +0.4%.

In Europe, indices are trading mixed with notable out performance in Italy as Banks outperform on comments from ECB’s Nouy being open to delaying new rules on non-performing loans. Elsewhere, corporate earnings continue to be the focal point.

U.S socks are set to open in the ‘red’ (-0.1%).

Indices: Stoxx600 -0.1% at 394.2, FTSE flat at 7528, DAX +0.1% at 13389, CAC-40 +0.1% at 5474, IBEX-35 +0.1% at 10236, FTSE MIB +0.5% at 22950, SMI flat at 9259, S&P 500 Futures -0.1%

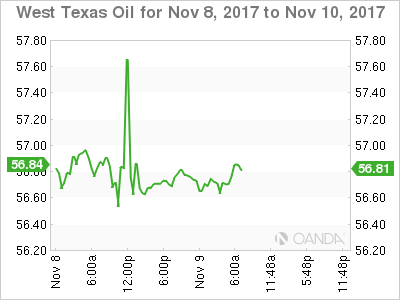

2. Oil prices stabilize, gold higher

Oil prices have steadied just below their two-year highs on Thursday, supported by supply cuts by OPEC and other major exporters including Russia.

Benchmark Brent crude is unchanged at +$63.49 a barrel. On Tuesday, Brent reached an intra-day high of $64.65; it’s highest since June 2015. U.S light crude is also steady at +$56.81, not too far off this week’s more than two-year high of +$57.69 a barrel.

Crude ‘bears’ that this week’s push higher – Brent is up by more than +40% since July – may have run its course due to increases in U.S supplies and some indicators of a demand slowdown.

Prices are still supported by efforts led by OPEC and Russia to withhold supplies in order to tighten the market and prop up prices.

Note: OPEC will discuss output during a meeting on Nov. 30, and is expected to extend the limits beyond their expiry in March 2018.

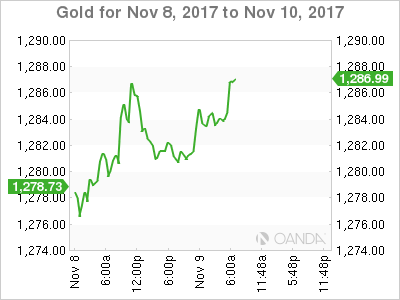

Ahead of the U.S open, gold prices have edged a tad higher overnight, one day after marking an intraday three-week high, as the dollar eased. Spot gold has rallied +0.2% at +$1,283.91 per ounce. Yesterday, it rose +0.4% and touched it’s highest since Oct. 20 at +$1,287.13 an ounce.

3. Sovereign yield curves remain tight

Sovereign and U.S Treasury prices have barely moved, with curves consolidating at their flattest levels in nearly a decade.

The yield on U.S 10’s have sank -2 bps to +2.31%, the lowest in more than three-weeks. In Germany, 10-year Bund yields are unchanged at +0.33%, the lowest in two-months, while in the U.K, the 10-year Gilt yield has declined less than -1 bps to +1.223%, the lowest in two-months.

Note: Yesterday’s U.S Treasury +$24B 10-year note auction came down at +2.314% with a bid-to-cover of 2.48 vs. 2.23 prior and 2.27 over the las ten auctions.

The Reserve Bank of New Zealand kept policy unchanged in its Thursday decision but indicated an interest rate hike could come sooner thanks to a pick-up in inflation. The kiwi surged. The RBNZ left Cash Rate (OCR) unchanged at +1.75% and noted that Kiwi employment growth had been strong.

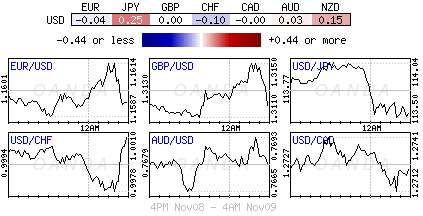

4. The Dollar’s mixed fortunes

On the whole, the FX market remains relatively subdued, but the USD is beginning to face some headwinds as the US-lead Republican tax-reform plan is coming under some heavy scrutiny.

GBP/USD (£1.3096) is a tad lower outright, as market focus now shifts back to the sixth round of monthly Brexit talks between the U.K and E.U officials. There are some doubts beginning to fester on whether the E.U would feel comfortable in moving to the second phase of talks when E.U leaders meet again next month. Again, U.K political and economic uncertainty leaves the pound vulnerable.

Note: PM May has suffered the second resignation in a week from her cabinet Wednesday as Priti Patel resigned as international development secretary.

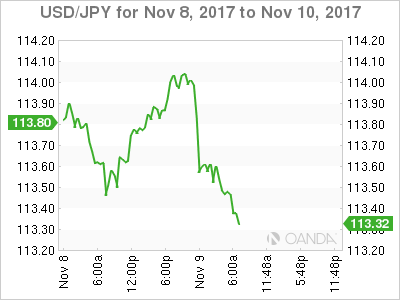

USD/JPY (¥113.46) is also lower as the Yen firmed following the Nikkei Stock Average reversal of its wild intraday +2% gain overnight. The index ended the session -0.2% lower, after breaching 23,000 for the first time in 25-years.

5. China inflation data suggest economy strong

Data overnight showed that China’s producer prices were surprisingly strong in October, while consumer inflation picked up pace, suggesting the world’s second largest economy remains robust, easing market concerns of a slowdown.

Chinas price pressures remain strong on the back of still rapid economic growth, a tight labour market, capacity cuts and temporary disruptions to industrial production

China OCT CPI m/m: +0.1% vs. +0.2%e; y/y: +1.9% (highest since Jan reading of +2.5%) vs. +1.8%e. PPI y/y: +6.9% vs. +6.6%e.