{kind=link}

- We expect the Bank of England (BoE) to cut the Bank Rate to 4.25% on Thursday 8 May in line with consensus and market pricing.

- Inflation has surprised to the downside over the past months and combined with elevated uncertainty and downside risks to growth from the trade war, we expect the MPC to deliver a slightly dovish twist.

- We expect EUR/GBP to end the meeting higher on dovish commentary. We stay negative on GBP.

We expect the Bank of England to cut the Bank Rate to 4.25% on Thursday 8 May in line with consensus and market pricing. We expect the vote split to be 8-1 with the majority voting for a 25bp cut and dove Dhingra voting for a larger 50bp cut. Note, this meeting will include updated projections and a press conference following the release of the statement.

We expect the BoE to deliver a dovish twist to its guidance on Thursday signalling that the bar for consecutive rate cuts has been lowered. We think they will stick to the formal guidance repeating that a “gradual and careful approach to removing monetary policy restraint remains appropriate“. Removing the notion of a “gradual” cutting cycle would be a strong signal of the MPC considering consecutive cuts. Inflation has surprised to the downside and with energy prices moving lower since the February meeting, the inflation forecast will likely be revised downwards although the conditional market implied rate path is significantly lower than in the February forecast. Wage growth has likewise been slightly lower than expected with private sector regular wage growth coming in at 5.9% (vs Boe forecast of 6.2% for Q1). Growth has been slightly better than expected and retail sales point to improvement in private consumption but the impact from tariffs poses a downward risk. We think the former will lift the 2025 forecast and the latter will be reflected in a downward revision of the GDP forecast in 2026. PMIs have shown tentative signs of a more stagflationary backdrop with price pressures accelerating and growth being more muted.

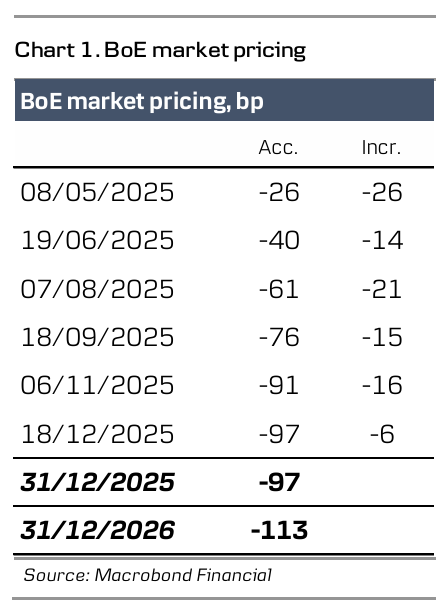

BoE call. We expect the BoE to stick to quarterly cuts, leaving the Bank Rate at 3.75% by YE 2025, which is a higher level than markets are expecting. Markets are pricing around 97bp for the remainder of the year. However, we highlight that the risk is skewed towards a swifter cutting cycle in 2025 given the downside risks to growth from the trade war.

Market reaction. We expect markets to react by sending UK yields lower and EUR/GBP higher on the dovish twist to the BoE’s communication. More broadly, while we see domestic factors as GBP positives, we think the global investment environment will be in the driver’s seat for EUR/GBP in the coming months. An investment environment characterised by elevated uncertainty, widening credit spreads and a positive correlation to a USD negative environment, in our view, favours a weaker GBP. We therefore expect EUR/GBP to move higher towards 0.88 on a 6-12-month horizon.