Summary

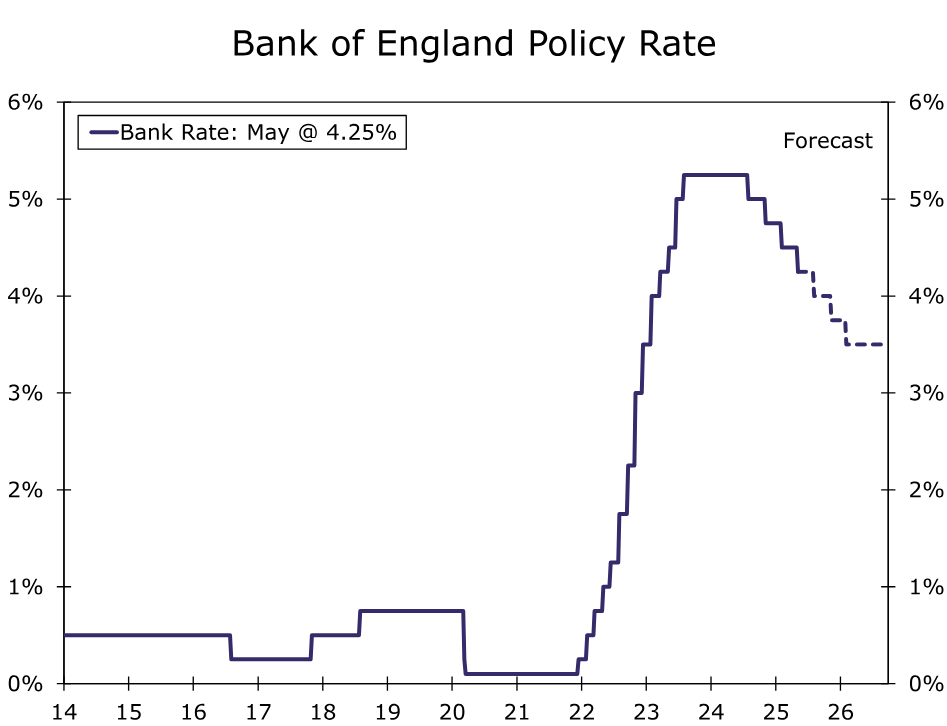

- The Bank of England (BoE) delivered a widely anticipated 25 bps rate cut at today’s announcement, bringing the policy rate down to 4.25%. Between the somewhat balanced policymaker vote split, mixed commentary on economic trends, and updated economic projections that did not contain any major surprises, we view the decision as broadly neutral. In terms of forward guidance, BoE officials communicated a desire to maintain a gradual and cautious approach towards further easing.

- In terms of recent economic trends in the United Kingdom, we have yet to see data that would suggest a deviation from this gradual rate cut path. The U.K. economy started 2025 in reasonably good shape, and we see relatively limited impact on the U.K. economy from higher U.S. tariffs. There are areas of caution—such as some degree of fiscal consolidation and a mixed picture for business investment—but we believe policymakers would likely only adopt a shift in stance if these developments were to result in sharply slower overall economic growth.

- As for wage and price growth developments, the picture is somewhat mixed. While in our view the direction of wage and labor cost pressures is broadly favorable, some measures of pay growth are still elevated. On the price front, the news has been more encouraging, with March CPI inflation surprising to the downside. While disinflation progress is noticeable, services inflation is persisting for now, which we see as consistent with a more gradual pace of rate cuts.

- We maintain our view for a once-per-quarter BoE rate cut pace through Q1-2026. We see 25 bps rate cuts in August, November, and February, with the policy rate expected to reach a low of 3.50% by early next year. Given our expectation for only gradual BoE easing, combined with anticipated U.S. economic weakness later this year, we see limited pound weakness against the dollar through the end of this year. However, more pound weakness could be seen in 2026, as the Fed concludes its easing cycle and the U.S. economy recovers.

Bank of England Takes Further Step Along Its Monetary Easing Path

The Bank of England (BoE) delivered a widely anticipated 25 bps rate cut at today’s announcement, bringing the policy rate down to 4.25%. The accompanying statement and updated projections were relatively balanced, which we view as consistent with the BoE maintaining a gradual pace of rate cuts for the time being.

Looking more closely at the statement itself, the first balanced element was the 5-2-2 vote split. That is, five policymakers voted for the 25 bps rate reduction, while two policymakers voted for a larger 50 bps cut and two voted for no change. In terms of the other elements of the statement, the BoE said “underlying UK GDP growth is judged to have slowed since the middle of 2024, and the labor market has continued to loosen.” The central bank also observed that “progress on disinflation in domestic price and wage pressures is generally continuing … although indicators of pay growth remain elevated, a significant slowing is still expected over the rest of the year.”

Importantly, the BoE did not offer any significant adjustment to its future policy guidance. The central bank reiterated that a “gradual and careful approach” to the further withdrawal of monetary policy restraint remains appropriate. Additionally, the BoE also said monetary policy will need to “remain restrictive for sufficiently long” until the risks to inflation returning sustainably to the 2% target in the medium term have dissipated further.

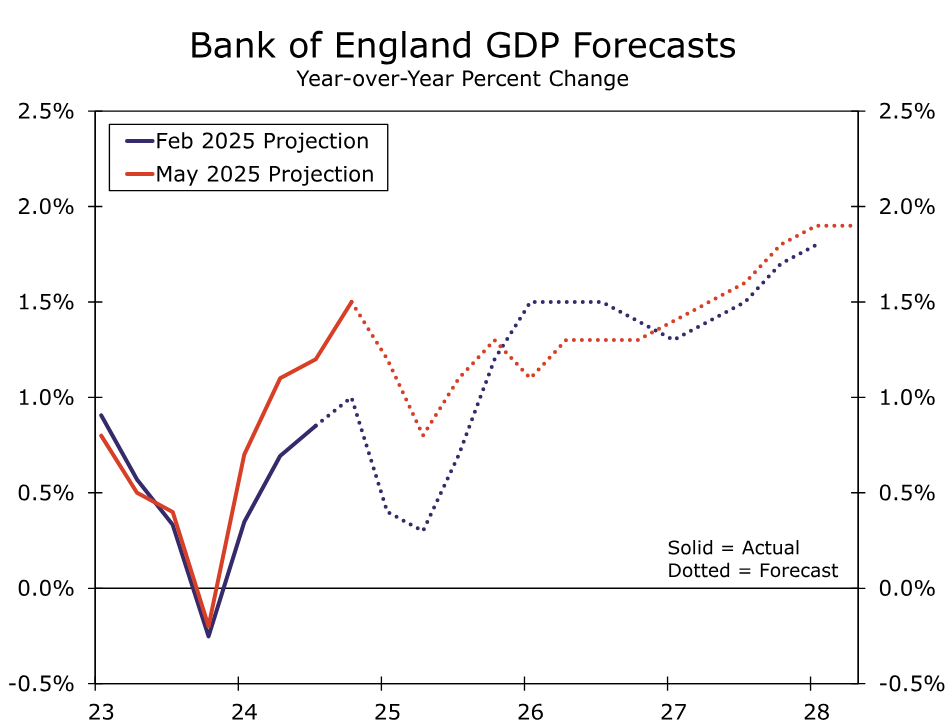

Turning to the BoE’s updated economic projections, there is little to suggest an acceleration in the pace of rate cuts. The forecasts are based on an assumption that the BoE’s policy rate will decline gradually to 3.50% by Q2-2026. With respect to economic growth, U.K. GDP is expected to jump 0.6% quarter-over-quarter in Q1-2025 before slowing sharply thereafter. In terms of its overall GDP forecasts, the BoE raised its growth forecast for 2025 to 1% (previously ¾%), lowered its growth forecast for 2026 to 1¼% (previously 1½%), and kept its 2027 growth forecast at 1½%.

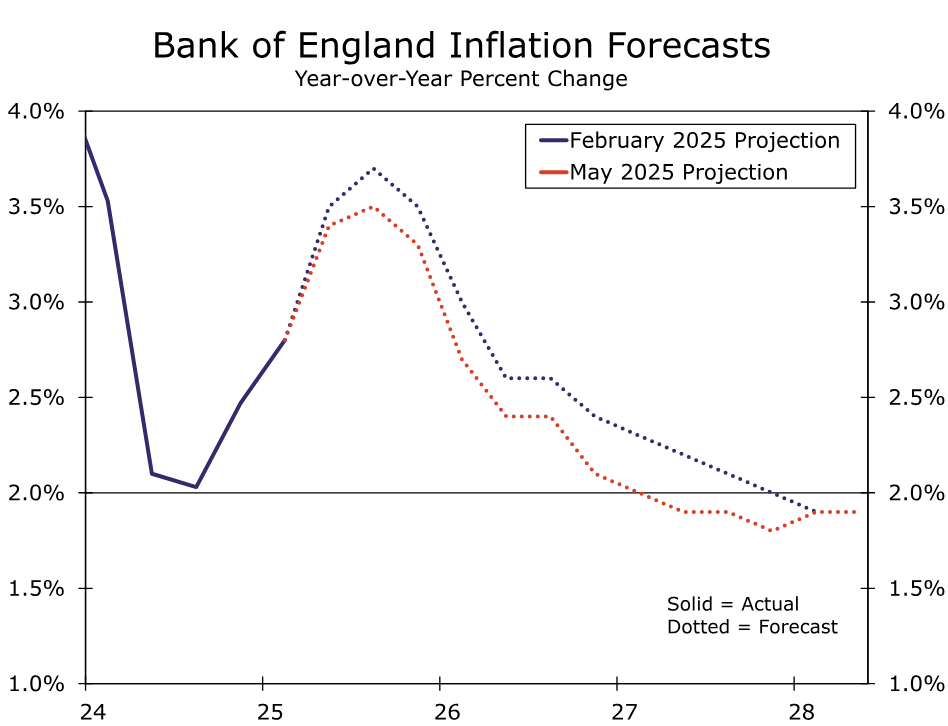

Meanwhile, the central bank lowered its CPI inflation forecast for 2025, 2026 and 2027. For a start, the BoE now sees a lower inflation peak of 3.5% in Q3-2025, compared to a previous forecast peak of 3.7%. CPI inflation is expected to return to the 2% target by early 2027, and to fall slightly below that target at 1.9% in both Q2-2027 and Q2-2028. The slowdown of inflation is predicated, in part, on a significant slowing in wage growth over the rest of this year.

A Slowdown in U.K. Growth Could Allow For Faster Rate Cuts…

Overall, today’s BoE announcement was broadly neutral and, so far, the central bank has not deviated from its once-per-quarter rate cut pace. Looking forward and thinking about what could prompt a shift in approach from the central bank, we think that growth dynamics have the most potential to prompt a shift to a faster pace of BoE easing, though probably not for some time.

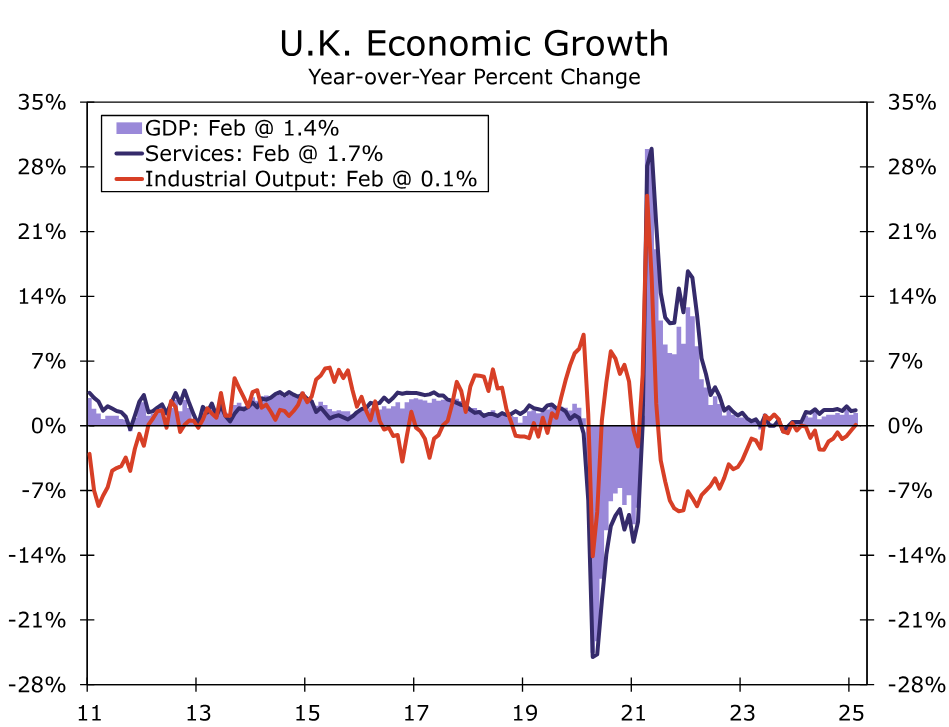

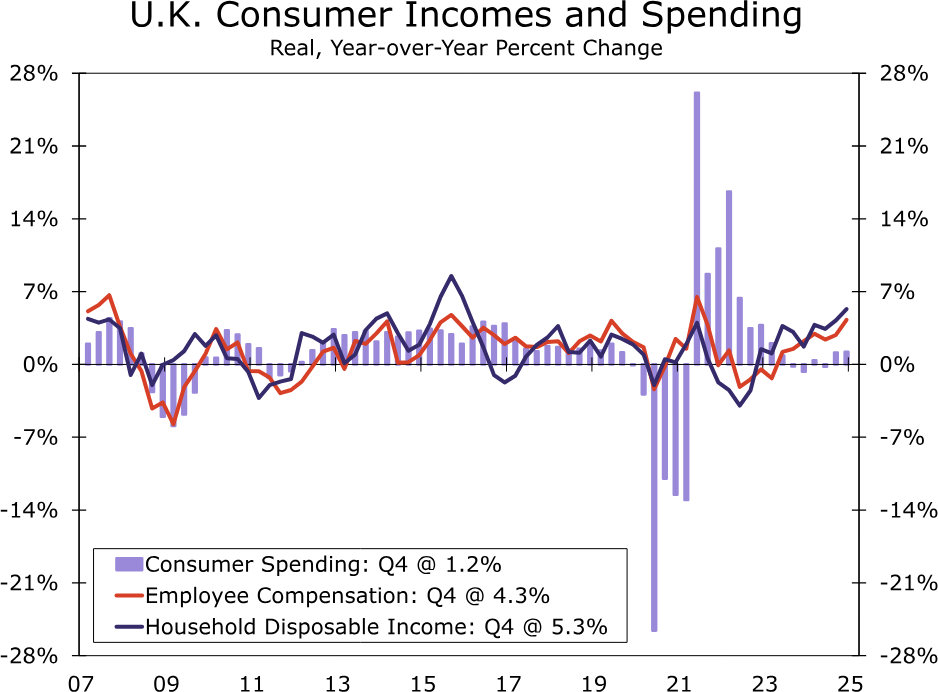

The U.K. economy started 2025 on a relatively solid footing. Retail sales rose every month during the first quarter, and February GDP registered a sizable 0.5% month-over-month gain. Considering the gains during the January-February period, the United Kingdom appears on track for Q1 GDP growth of around 0.5% overall. Some underlying dynamics behind the recent U.K growth details also appear favorable. Notably, the latest available data show real household disposable income grew 5.3% year-over-year in Q4-2024, well in excess of growth in consumer spending. Coupled with early-year advances seen in both services output and retail sales, this suggests that the U.K. consumer could provide some support for activity this year. That said, there are some cautionary factors to watch for. One concern on the consumer front is the increase in National Insurance Contributions that took effect in April, a factor that could lead some firms to adjust employment or wages, which could offer some headwinds to real income growth. Finally, while higher U.S. tariffs are certainly not a positive for the United Kingdom, the British economy could be less negatively impacted by U.S. tariffs than some other regions. We would argue the United Kingdom’s direct exposure to higher U.S. tariffs is somewhat limited. U.K. exports of goods the United States (which are subject to tariffs) accounted for a relatively modest 2.1% of U.K. GDP in 2024, while U.K. exports of services to the United States (which for now are not subject to tariffs) accounted for a more sizable 4.8% of U.K. GDP last year.

While the consumer outlook appears reasonably solid and the direct negative impact from tariffs could perhaps be limited, there are nonetheless still reasons for concern regarding the U.K. outlook. For one, the government’s fiscal stance has turned more cautious in recent months. Faced with a shortfall in tax revenues and increased debt interest costs, the Chancellor of the Exchequer Rachel Reeves announced in the Spring Budget Statement in late March a package of £8.4B of welfare reductions and day-to-day spending cuts, an extra £3.4B from higher revenues from planning reforms, and £2.2B from more efficient tax collection. Even with the measures, the government has only a slim £9.9B fiscal buffer, meaning slower economic growth and tax revenues, or alternatively, higher yields, could still lead to further consolidation measures ahead.

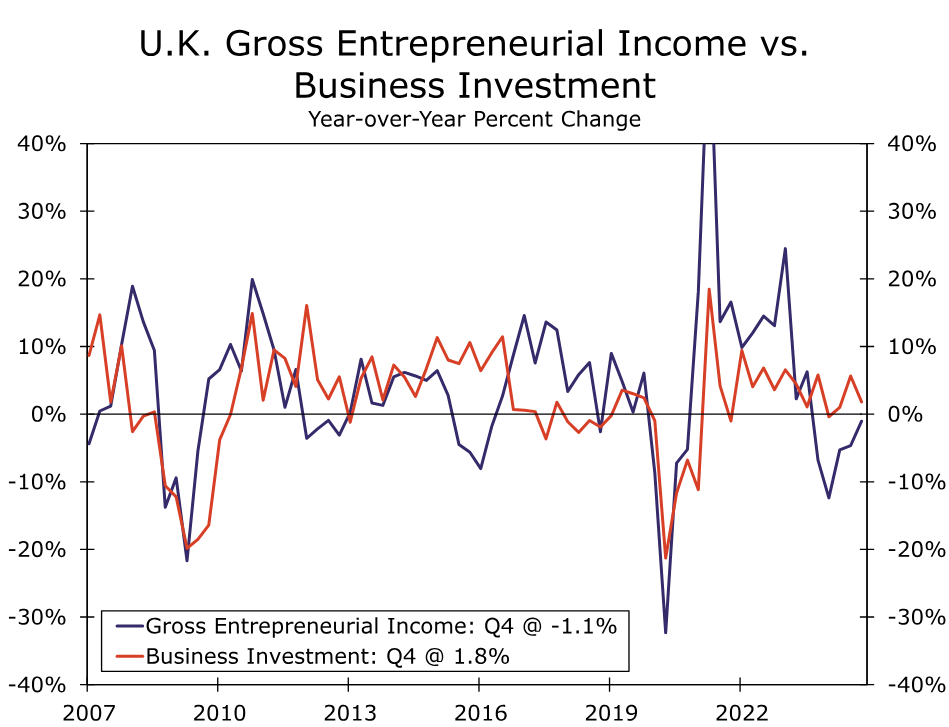

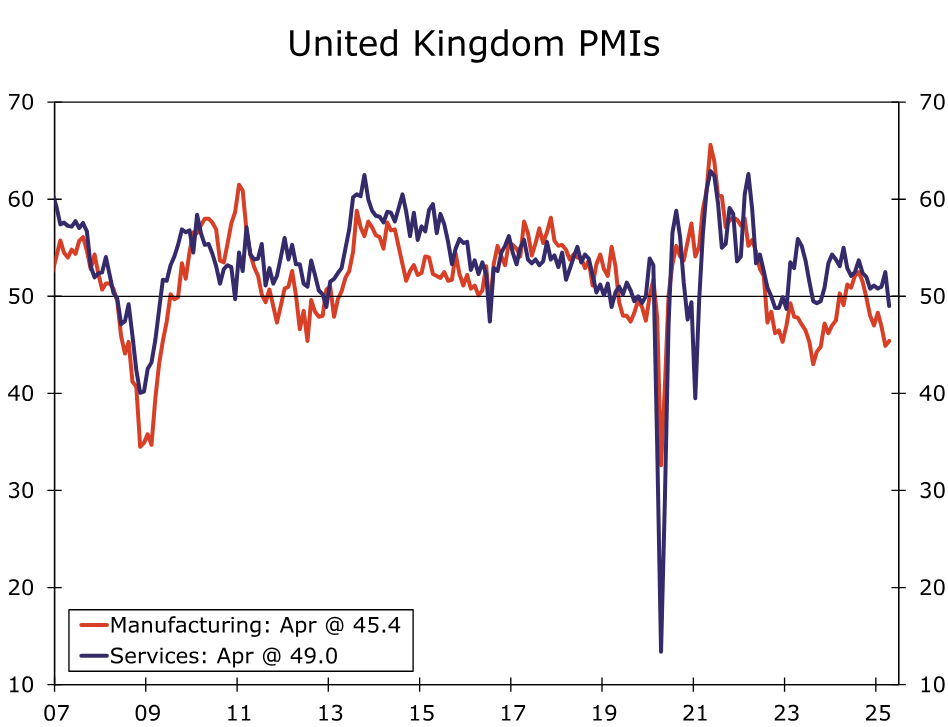

The business sector outlook also remains decidedly mixed. According to the OECD, gross entrepreneurial income of non-financial corporates fell 1.1% year-over-year in Q4-2024, a potential restraining influence on business investment moving forward. The increase in the employers’ National Insurance Contributions that took effect in April could also be a factor that weighs on profits, at the margin. More broadly, while the United Kingdom was spared the worst of the direct impact from higher U.S. tariffs, the indirect impact on the U.K. economy could still be significant. Given the likelihood of higher prices and/or lower growth across many major economies—including the United States, Eurozone and China—we have lowered our global GDP growth forecast to just 2.3% for both 2025 and 2026. The rather mixed outlook for U.K businesses is also reflected in the April PMI survey. It showed a modest improvement in the manufacturing PMI to 45.4, a reading that nonetheless remains very much in contraction territory. Meanwhile, the services PMI fell sharply to 49.0 from 52.5 in March, also entering contraction territory. Especially as this year progresses, and the full impact of higher U.S. tariffs and slower global growth takes effect, we expect the U.K. economy to underperform. Indeed, we forecast U.K. GDP growth of just 0.7% in 2025, rising to 1.5% in 2026. Our outlook for 2025 GDP growth is modestly below the BoE’s own forecast, and cumulatively, our growth forecast is also below the central bank’s estimates of potential growth, which it sees as around 1.5% over the medium term. Against this backdrop, we view our subpar U.K growth outlook as consistent with slowing employment growth, rising unemployment, and some easing in wage pressures—trends that could eventually be consistent with a more accelerated pace of Bank of England monetary easing.

…But Wage And Price Trends Will Hold The Key To Whether Faster Easing Occurs

While the U.K. growth outlook in isolation might suggest scope for an eventual faster pace of easing, whether the Bank of England ultimately pursues that approach will in large part depend on whether wage and inflation trends show clearer and more decisive deceleration. The BoE has been regularly surprised in recent years, during and following the pandemic, initially by how quickly wages and inflation spiked surrounding the pandemic, and subsequently by how persistent and stubborn wage and price pressures have been in the years since. Thus, although the BoE’s analysis and modeling might suggest an expected slowdown in wage and prices, the central bank might need to see more evidence of that slowdown before transitioning to a more frequent cadence of rate cuts.

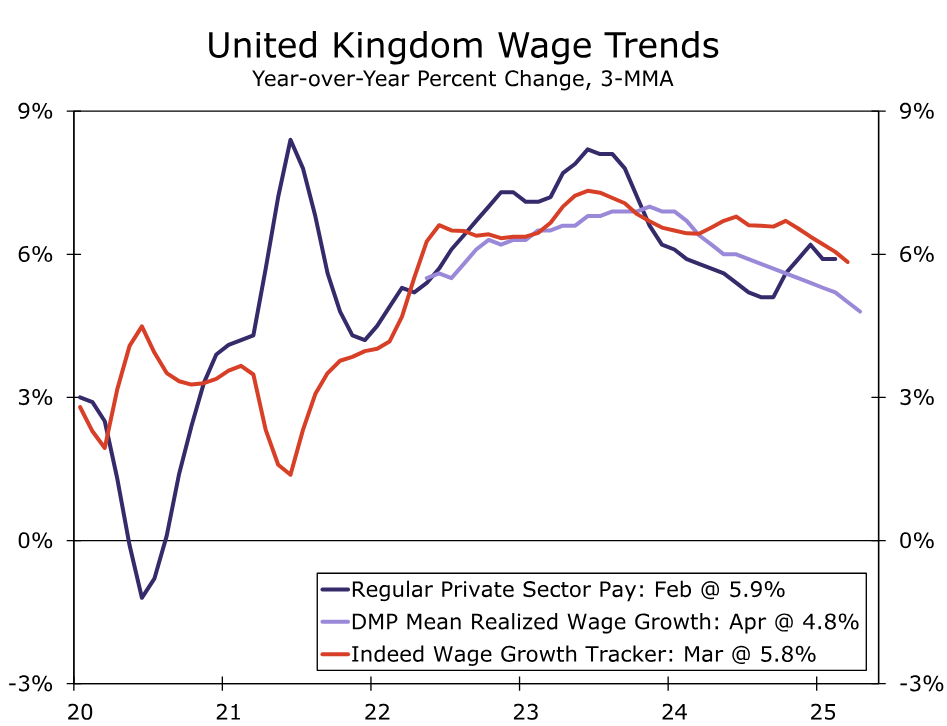

So far, the evidence on wage growth is mixed. For the December-February period, average weekly earnings for the private sector excluding bonuses—a measure closely watched by BoE policymakers—rose 5.9% year-over-year, in line with the consensus forecast and steady compared to the prior reading. This measure of wage growth has also quickened slightly since late 2024. Still, recent pay growth has come in somewhat below the BoE’s previous projections. Other indicators of wage growth hint at the potential for further deceleration ahead. For example, realized wage growth as reported by the BoE’s Decision Makers Panel slowed to 4.8% year-over-year in the three months to April. Similarly, the U.K. Indeed Wage Tracker has also slowed recently, though it remains elevated at 5.8% year-over-year in the three months to March. While somewhat dated, the most recent estimate of U.K. unit labor costs showed a gain of 4.5% year-over-year in Q3-2024, a level that we view as likely too high to be compatible with the BoE’s 2% inflation target on a sustained basis. A modest improvement in U.K. productivity since then may have seen unit labor costs soften a bit further. Altogether, our sense is that the direction of wage and labor cost pressures is broadly favorable from the BoE’s inflation targeting perspective. At the same time, we suspect that policymakers will want to see clearer evidence of a more pronounced slowdown in wage pressures before they would contemplate accelerating the pace of rate cuts.

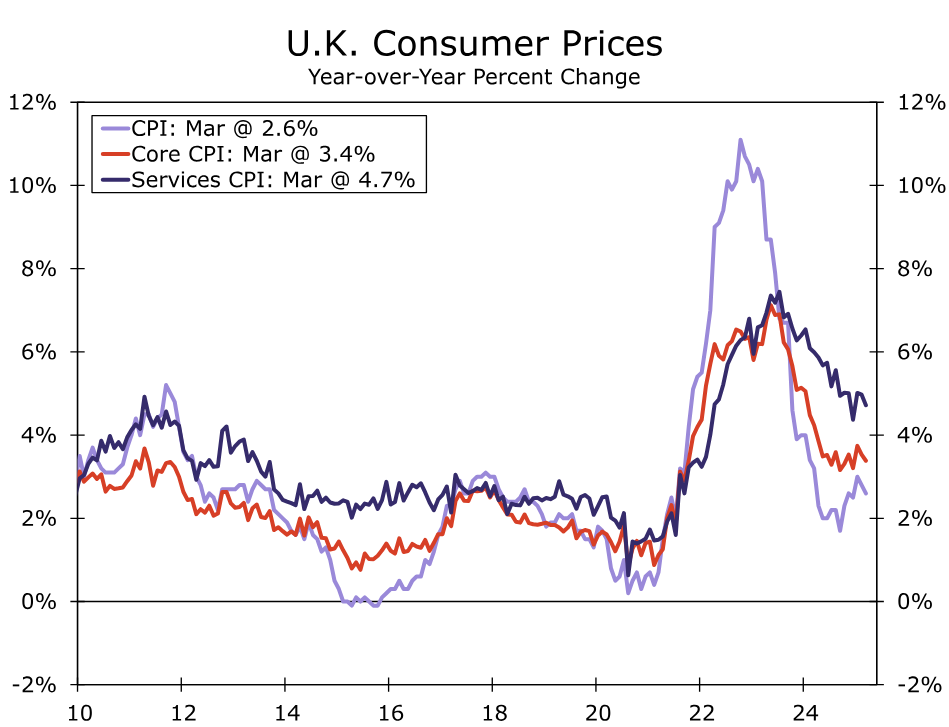

Regarding prices, the latest inflation news has been a bit more encouraging, with the March CPI surprising modestly to the downside. Headline inflation slowed to 2.6% year-over-year, and a sharp slump in oil prices since early April could help restrain headline inflation in the immediate months ahead. March core CPI inflation eased to 3.4%, and services inflation slowed a bit more than forecast to 4.7%. Specifically with respect to services prices, our own seasonally adjusted measures suggest that services inflation has advanced at around a 4.50%-4.75% annualized rate over the past six months. The key takeaway, in our view, is that while the recent price trends in U.K. core inflation and services inflation are encouraging, they remain more consistent with a steady rather than accelerated pace of monetary easing by the Bank of England at this stage.

Overall, we view today’s policy announcement as broadly neutral and are not yet convinced the Bank of England will shift to an accelerated rate cut path. For the time being, our base case remains for Bank of England easing to continue at a 25 bps rate cut per quarter pace. We forecast 25 bps rate cuts in August and November of this year, and February of next year, which would bring the policy rate to a low of 3.50%. While we view the growth outlook as potentially consistent with an eventual acceleration of monetary easing, we think policymakers will need to see more convincing evidence that wages and prices are indeed slowing in a manner that is more compatible with sustained convergence towards the 2% inflation target before adjusting rates more frequently. We think it will be several months, at the earliest, before sufficient evidence emerges on the wage and price front for BoE policymakers to be comfortable picking up the pace of easing. Moreover, we think it could be several months before the full effect of higher U.S. tariffs and weaker global growth are fully apparent, prompting the Federal Reserve to also begin lowering interest rates from later this year. Thus, while we would view the risks to our outlook as tilted toward faster and more pronounced rate cuts, that appears unlikely until late this year at the earliest. Indeed, we think the most plausible risk scenario would see the BoE deliver 25 bp rate cuts in August, November and also December this year, along with February of next year, for a policy rate low of 3.25%. However, that outcome would probably only happen if U.K. growth and inflation data surprise consistently to the downside. Finally, the relatively gradual easing we expect from the BoE, combined with the economic challenges the United States should face in the second half of this year, in our view, suggests only limited weakness in the pound through most of 2025. We see more potential for sterling to weaken in 2026, as U.S. economic growth recovers and as Fed easing comes to an end. Our medium-term outlook anticipates a GBP/USD exchange rate of $1.3100 by the end of 2025, declining to $1.2800 by late 2026.

delivered a widely anticipated 25 bps rate cut at today's announcement, bringing the policy rate down to 4.25%. Between the somewhat balanced policymaker vote split, mixed commentary on economic trends, and updated economic projections that did not contain any major surprises, we view the decision as broadly neutral. In terms of forward guidance, BoE officials communicated a desire to maintain a gradual and cautious approach towards further easing.){kind=link}