{kind=link}

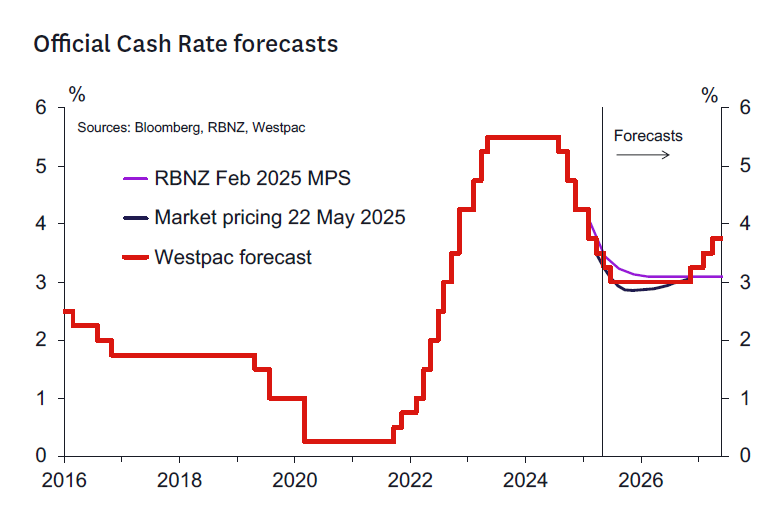

- We expect the RBNZ to cut the OCR by 25bp to 3.25%.

- We see the RBNZ’s OCR profile being revised down by around 20bp to around 2.9% by the end of 2025.

- Beyond this meeting a data dependent easing bias seems likely.

- The RBNZ may be open to a pause in July depending on events.

- We expect downside and upside scenarios to be canvassed. The downside scenario will likely imply more policy adjustment than the upside scenario.

- We expect to see evidence of increased debate among MPC members the amount of weight placed on high near-term inflation and rising expectations versus lower medium- term forecasts.

RBNZ decision and communication.

We expect the RBNZ to cut the OCR by 25bp to 3.25% and signal a data dependent easing bias looking ahead. We see the RBNZ’s OCR profile being revised down by around 20bp to around 2.9% by the end of 2025. A broadly flat profile beyond 2025 seems likely. The very shortterm assumption for Q3 2025 is likely to leave the RBNZ the option to cut the OCR in either of July or August. Arithmetically, a 3.1% OCR projection for Q3 would split the difference between the two meetings and signal the intention to assess the next move carefully with reference to emerging data and global developments.

We don’t see either an unchanged OCR or a 50bp cut as likely outcomes and put around 5% probabilities on each (although there is debate among the team on whether one is slightly more likely than the other).

The RBNZ will likely assess the economy as still being on a recovering trend. However, it will probably view the recovery in domestic activity as somewhat weaker than hoped (consumer spending/consumption and investment), but stronger than expected in externally focused sectors (tourism, primary sector, services exports). The labour market outlook will remain the same – we suspect they won’t need to revise down their peak unemployment rate given it was already at a low level of 5.2% in the February Monetary Policy Statement. The starting point for the output gap will be revised modestly upwards (less slack in the economy) but the more muted short-term outlook may mean little net change if evaluated over all of 2025.

The RBNZ may modestly upgrade their short-term inflation outlook given the Q1 CPI and subsequent Selected Price Indices. Previously, the RBNZ expected the CPI to peak around 2.7% in 2025 – that might push up to 2.8 or 2.9% at the peak. This uncomfortable short term inflation outlook will likely temper at least somewhat the dovish implications of the slightly weaker domestic growth outlook. Rising inflation expectations, and still robust pricing intentions on some measures, will likely rate a mention on the hawkish side of the ledger.

The RBNZ is very likely to make a decent sized downgrade in their trading partner GDP outlook – perhaps in the order of 0.5% over 2025. This will depress GDP and the output gap over the medium term – although the final impact on the interest rate projections will depend somewhat on their assumptions on the impact of the terms of trade. The RBNZ will upgrade the starting point for the terms of trade (export prices have been stronger and import prices weaker than expected) which will offset downgrades made to future export price assumptions.

The RBNZ will likely emphasize the uncertainty and downside risks associated with global economic developments. We expect the RBNZ to present an alternative scenario based on an outlook where the world steps back to global tariffs closer to those presented by the US authorities on “Liberation Day” with some escalation on some bilateral tariff rates (although not to the full extent reached in the aftermath of April 8). We expect this scenario to assume at least a degree of retaliation – although not to the extremes assumed by the Reserve Bank of Australia in their Statement on Monetary Policy this week.

This downside scenario may also feature heightened uncertainty over a longer period. The implication would be downward adjustments to investment and consumption and a higher unemployment rate. The presented scenario may not include an implied OCR profile but might focus on the implications for key variables such as GDP growth, the unemployment rate and CPI inflation. It’s hard to be definitive on the size of the scenario shock, but it will likely leave the implication that in a downside scenario the OCR could move down towards 2-2.5%.

An upside scenario may also be presented that could feature a faster resolution of uncertainty on the global trade outlook and hence a stronger short term growth profile. The scenario might imply some reduction in the 10% tariff the US has imposed on New Zealand exports. This scenario would imply little additional need to ease policy further.

The RBNZ’s commentary will likely emphasize that it is navigating difficult waters between an uncomfortably high short term inflation outlook and downside medium term growth and inflation risks. We expect them to signal a data dependent easing bias that leaves open the option to pause in future meetings. The Summary Record of Meeting is likely to reflect a potentially vigorous debate on the weight the MPC should put on the uncomfortably high near-term inflation outlook versus hopes for lower inflation in 2026 and beyond. Some members are likely to argue for a much slower and more data dependent pace of easing going forward.

In many respects, the August Statement may be a more natural time to take the next step lower in the OCR if required. By then the trading partner outlook may be clearer (noting 8 July is the US authorities’ self-imposed deadline to conclude trade negotiations – just a day before the July MPR). Also, the RBNZ will have key CPI data (21 July) and labour market reports (6 August). We don’t expect the outcome of this week’s Budget to feature prominently in the MPCs discussions. The MPC will likely remain comfortable that government consumption as a proportion of GDP will continue to decline and hence not hinder the goal of moving inflation back closer to 2%. Some alternative scenarios for the outcome of this meeting include:

- Hawkish scenario – a 25bp cut with a clear intent to pause in July. The RBNZ would note an intent to review things again in August and with the possibility of one final cut to 3% if required.

- Dovish scenario – a 25bp cut with a presumption of a further cut to 3% by August and a further cut to 2.75% later in 2025. The possibilities of a move lower still in the OCR towards 2-2.5% might also be discussed as a risk scenario. The RBNZ would be putting more weight on the downside growth and inflation scenario and less regard for the short-term inflation picture.

Key developments since the February Monetary Policy Statement.

Aside from the US tariff announcement, the main data developments since the RBNZ’s February policy statement have been:

GDP: Activity rose by 0.7% in the December 2024 quarter, ahead of the RBNZ’s estimate of 0.3%. Given their usual approach, the RBNZ will likely now assess that the negative output gap is narrower than the 1.7% of GDP that had been estimated for Q4.

Business confidence: Indicators have been mixed, but consistent with an improving but still sub-trend growth outlook. The NZIER survey for the March quarter showed firms becoming more optimistic in the outlook for the months ahead, but the assessment of current conditions remained subdued. The monthly ANZ survey has seen confidence hold up at high levels, though responses in the second half of April – after the ‘Liberation Day’ announcement – were notably softer. However, this represents a small sample and coincides with when the commentary and market reaction to the tariffs was at its most negative. The indicator of firms’ activity compared to a year earlier lifted into positive territory in April.

Other activity indicators: High-frequency economic data have been mixed. The BusinessNZ manufacturing PMI has risen and held above the 50 mark since the start of the year, but the comparable index for services has softened again in the last few months. Retail card spending has slowed again after a strong end to 2024. Residential building consents have been broadly steady in recent months. Westpac’s GDP Nowcast suggests still sub-par GDP growth in Q1 and Q2 while the new RBNZ Nowcast remains consistent with the RBNZ’s February short term GDP growth profile.

Inflation: March quarter prices were a little firmer than the RBNZ expected, with annual inflation rising from 2.2% to 2.5% compared to their February forecast of 2.4%. A technical change to the measurement of tertiary education fees may have accounted for the upside surprise. The selected monthly prices up to April are showing mixed trends, with re-emerging upward pressure in food prices but slowing growth in rents. Increased vehicle licensing fees will likely lift their short term forecasts a tad.

Inflation expectations: The pricing intentions gauge in the ANZ’s business survey has increased in recent months and continues to sit at levels that historically have not been consistent with inflation remaining inside the target range. The RBNZ’s quarterly surveys shows that inflation expectations have increased at both the shortterm and long-term horizons.

Labour market: The unemployment rate held steady at 5.1% in the March quarter, against the RBNZ’s forecast of a slight rise to 5.2%. The level of employment rose by 0.1%. Wage growth was softer than the RBNZ expected, with the Labour Cost Index slowing from 3.3% yr to 2.9%yr. Job advertisements are yet to show a lift from the cyclical lows reached last year.

Housing market: Both house sales and mortgage approvals point to increasing levels of housing activity since the second half of last year, trending higher as mortgage rates have been progressively lowered. Mortgage approvals remain strong. House prices have risen gradually in the last six months, broadly in line with the RBNZ’s expectations.

Commodity prices: Export commodity prices have continued to improve in recent months, especially in meat and dairy. Oil prices are noticeably lower than the RBNZ’s February projections. The overall terms of trade (measured on a National Accounts basis) is running ahead of what the RBNZ assumed in February.

Exchange rate: The trade-weighted exchange rate index (TWI) is currently around 69, about 2% higher than what the RBNZ assumed in the February MPS (and the RBNZ will likely flatline its May forecast at this level). Higher export commodity prices provide some justification for the stronger currency.

Kelly’s take.

The easing at this meeting seems reasonable given the weaker global outlook that has eventuated since April (and certainly February). However, I think the MPC should be increasingly mindful of the amount of easing already delivered, and the lags to when the peak impact of that easing will take hold.

Uncertainty is high right now due to the trade outlook. But underneath that uncertainty there are factors that should underwrite economic recovery over time, and which could frustrate a timely return of inflation to 2%. Uncertainty is a transitory factor while the interest rates and terms of trade levels will be more enduring when the uncertainty resolves. I think there are encouraging signs that deals will be done on trade that resolves the uncertainty soon enough.

While there could be adverse outcomes that require a lot more easing, they remain just a possibility at this stage. Our terms of trade have strengthened in the last month or so as trade policy uncertainty has surged. Policy is well placed to respond if negative scenarios unfold. With inflation nudging 3% there’s no strong case for taking insurance by easing pre-emptively right now. Taking the time to assess the impact of the easing already delivered and the likelihood of future damage to the economy coming from a tougher global trade environment may be more prudent between now and August.