Economic data in the coming week will continue to highlight how trade disruptions in its early stages are impacting the Canadian and U.S. economies.

Inflation reports in the U.S. so far have failed to show the impact of tariffs on consumer prices. Core goods inflation in April was the first positive yearly reading since December 2023, mostly due to larger monthly increases earlier this year with a relatively subdued 0.06% month-over-month rise in April.

Nevertheless, tensions are brewing. Used car prices in the U.S. rose 4.4% from a year ago in May, according to the Manheim Used Vehicle Value Index—but it may be taking some time to appear in official consumer price index. Factoring in a slightly firmer monthly increase in core goods prices, we expect headline and core CPI in May to tick up 2.5% from 2.3% in April, and to 2.9% from 2.8%, respectively. Food and energy inflation likely held near the same levels with energy still below year-ago prices and food prices up almost 3%.

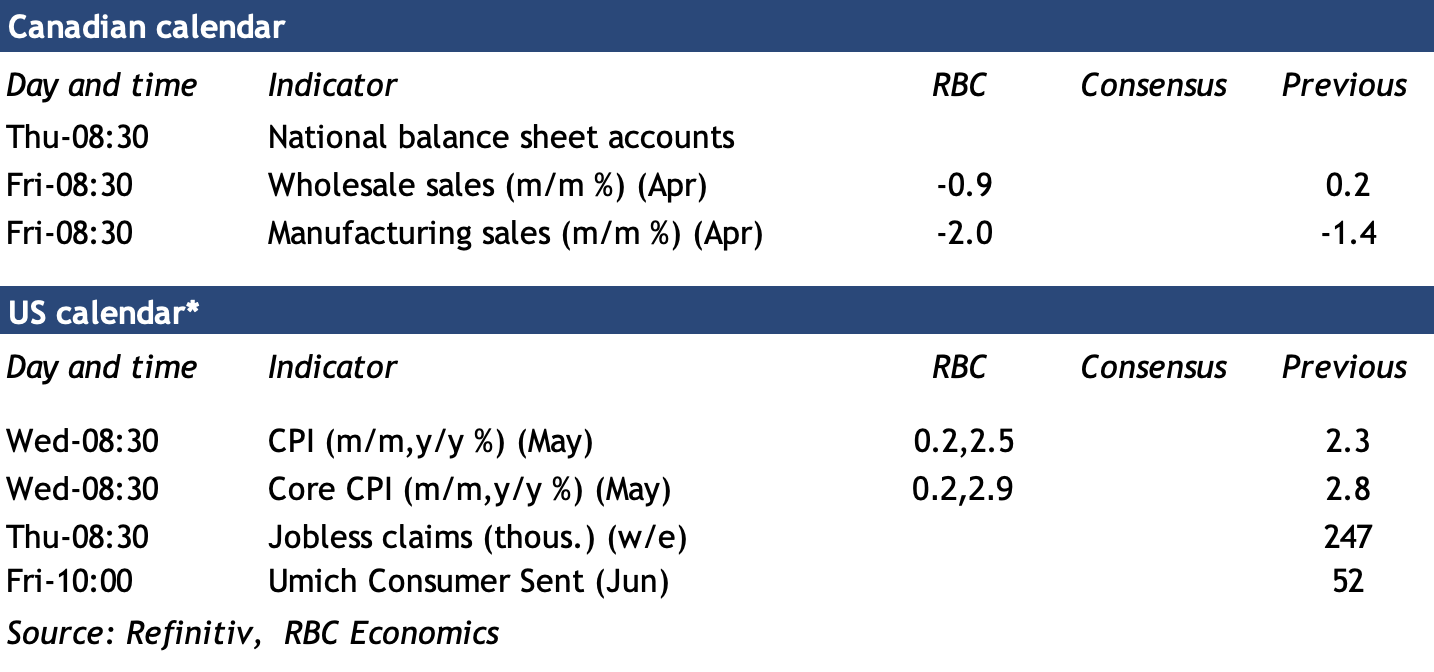

In Canada, early reports from Statistics Canada indicate manufacturing sales contracted by 2% in April. Separately reported industry price data shows that three quarters of that decline was likely price related. Oil prices were lower, reducing the nominal value of petroleum sales. But, the early estimate also flagged a softening in auto manufacturing. The decline coincides with 55k, or 2.9% job losses in the sector since January.

Wholesale sales in Canada were also estimated to have declined in April, but retail sales rose by 0.5%, according to StatsCan’s advanced estimate. Going forward, we expect additional softening in Canadian industrial sectors as tariffs reduce U.S. demand for Canadian exports, especially for auto and parts, steel, and aluminum products that are disproportionately targeted by U.S. tariffs. Offsetting some of that weakness will be resilience in domestic services consumption that has broadly held up.

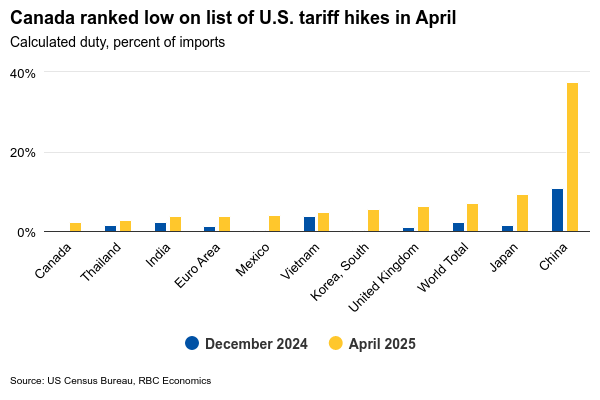

Overall, April’s international trade data confirmed that U.S. tariff increases on Canada, while significant, have been smaller than for other major U.S. trade partners. Barring more significant changes to existing U.S. tariffs, we expect growth in both Canada and the U.S. to slow this year, but expect both to avoid a recession. We anticipate a more pronounced impact on inflation in the U.S. where the average import tariff rate is now substantially higher than in Canada.

Week ahead data watch

We expect Canadian household net worth was little-changed in Q1 with both debt and asset levels holding around levels at the end of 2024. A pullback in equity markets in Q1 likely weighed on household financial asset holdings but house prices edged higher. Household debt service ratios (ratio of debt payments to household disposable income) likely remained elevated, but with little change from Q4/2024 at 14.4%, and still below the 15.1% peak in Q3 2023.

{kind=link}