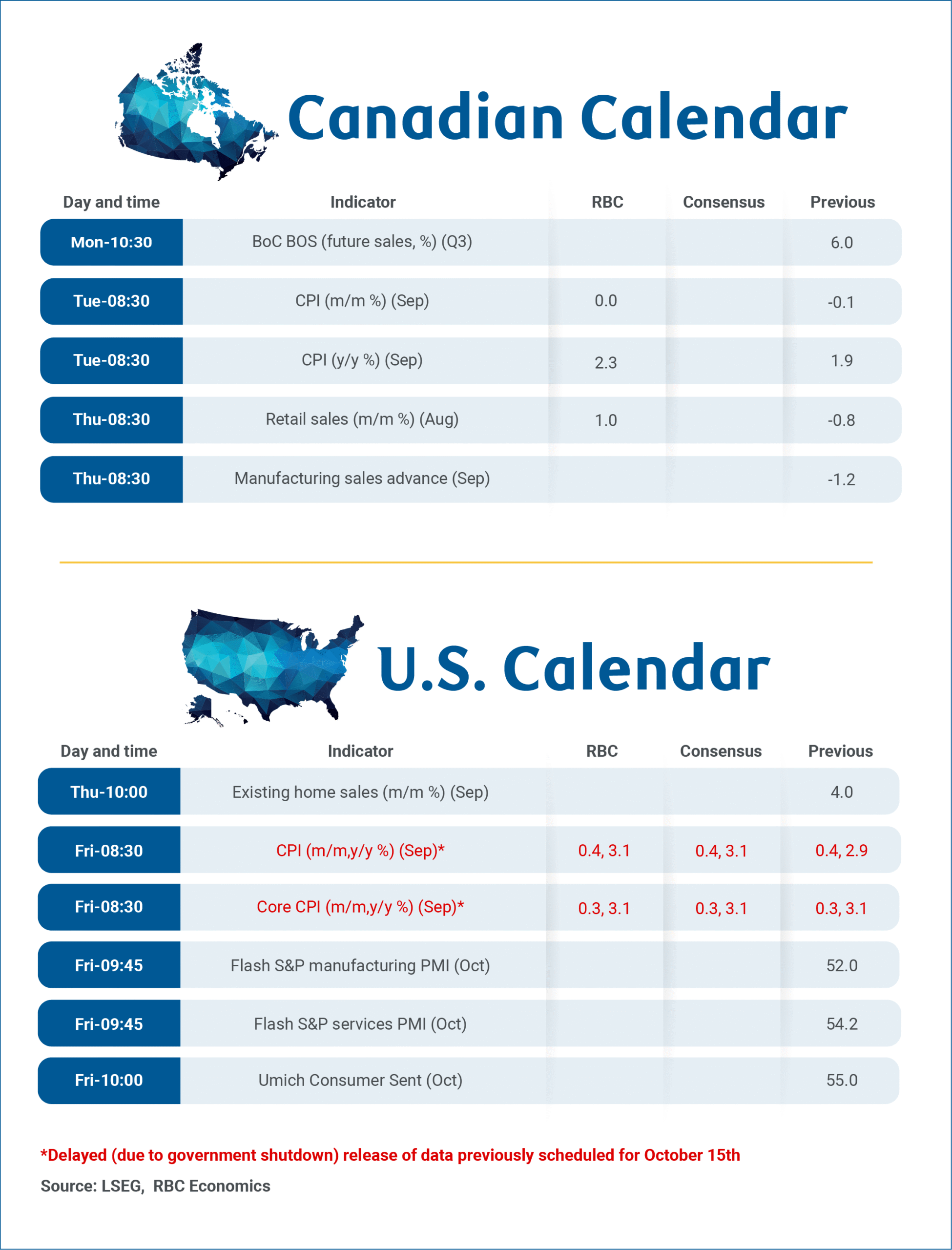

The Bank of Canada will be closely watching September’s consumer price index report, August’s retail sales data as well as its own Q3 Business Outlook Survey in the coming week ahead of an interest rate decision on Oct. 29.

It is unlikely that policymakers cut rates in September expecting that just one 25 basis point reduction would be sufficient. We expect them to follow with another 25 basis point cut in Q4, most likely later this month.

The BoC did leave additional rate reductions contingent on economic data, and inflation not surprising significantly to the upside. We don’t think details of a firmer-than-expected jobs report in September alone is enough to derail another rate cut, and we expect inflation trends look broadly similar in September to August.

We expect headline CPI growth of 2.3% year-over-year in September, up from 1.8% in August as the pace of energy price declines slowed. That would leave inflation tracking close to our Q3 base case assumption of a 2% quarterly average. Food price growth likely eased last month, but underlying price pressures appear to have firmed.

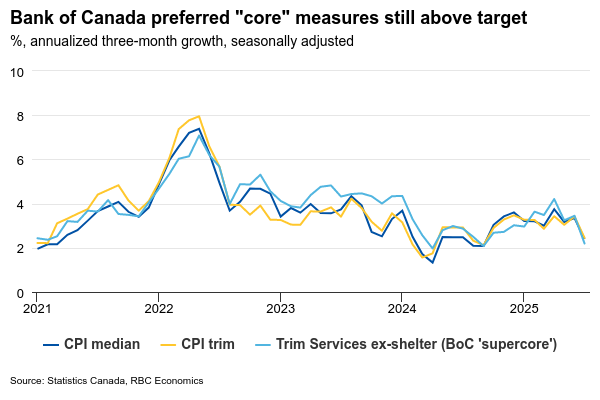

We look for inflation excluding food and energy to rise to 2.6% from 2.4% in August, suggesting modest upward pressure in other categories. The BoC’s preferred core inflation measures continue to hover near 3% year-over-year, and about 2.5% on a three-month rolling average. Both are still running above the BoC’s 2% inflation target, but are similar to the month earlier.

Stabilizing business sentiment

The Business Outlook Survey on Monday will offer a more qualitative check on the pulse of the economy. We expect it to show further signs of stabilizing business sentiment after a period of heightened uncertainty earlier this year when U.S. trade tensions were most intense. Earlier data from the Canadian Federation of Independent Business suggests the recovery is already underway. Their Small Business Confidence Index rose again in September, and now sits slightly above the breakeven threshold.

Meanwhile, a preliminary estimate of retail sales for August from Statistics Canada pointed to a 1% rebound following a July dip. September’s flash estimate on Thursday will be closely watched for signs of continued resilience in consumer spending. RBC’s card spending data showed relatively firm momentum in September, though Q3 quarterly spending growth has slowed from Q2.

Week ahead data watch:

The U.S. government shutdown is disrupting the release of several economic indicators, particularly from public sector agencies, but the Bureau of Labor Statistics has confirmed the CPI report will be released on Oct. 24. September CPI data is expected to show both headline and core inflation rising 3.1% year-over-year, reflecting the onset of core goods price pressures as tariff pass-through effects finally begin to emerge.

{kind=link}