{kind=link}

The US government shutdown officially became the longest in history today — 36 days and counting — yet markets found some relief in stronger-than-expected private data amid the lack of public releases.

The ISM Services PMI hit its highest level since February, and ADP employment came in at 42K vs. 25K expected, underscoring the economy’s resilience despite the political gridlock.

Equities staged a solid rebound after a rough weekly open, but sellers re-emerged late in the session, capping gains and reminding traders that volatility is here to stay.

Adding to the uncertainty, Trump’s tariffs are now being reviewed by the Supreme Court, injecting another layer of tension into an already fragile market mood.

With the December Fed rate cut still about 60% priced in despite Powell’s recent hawkish return, elevated volatility looks set to persist.

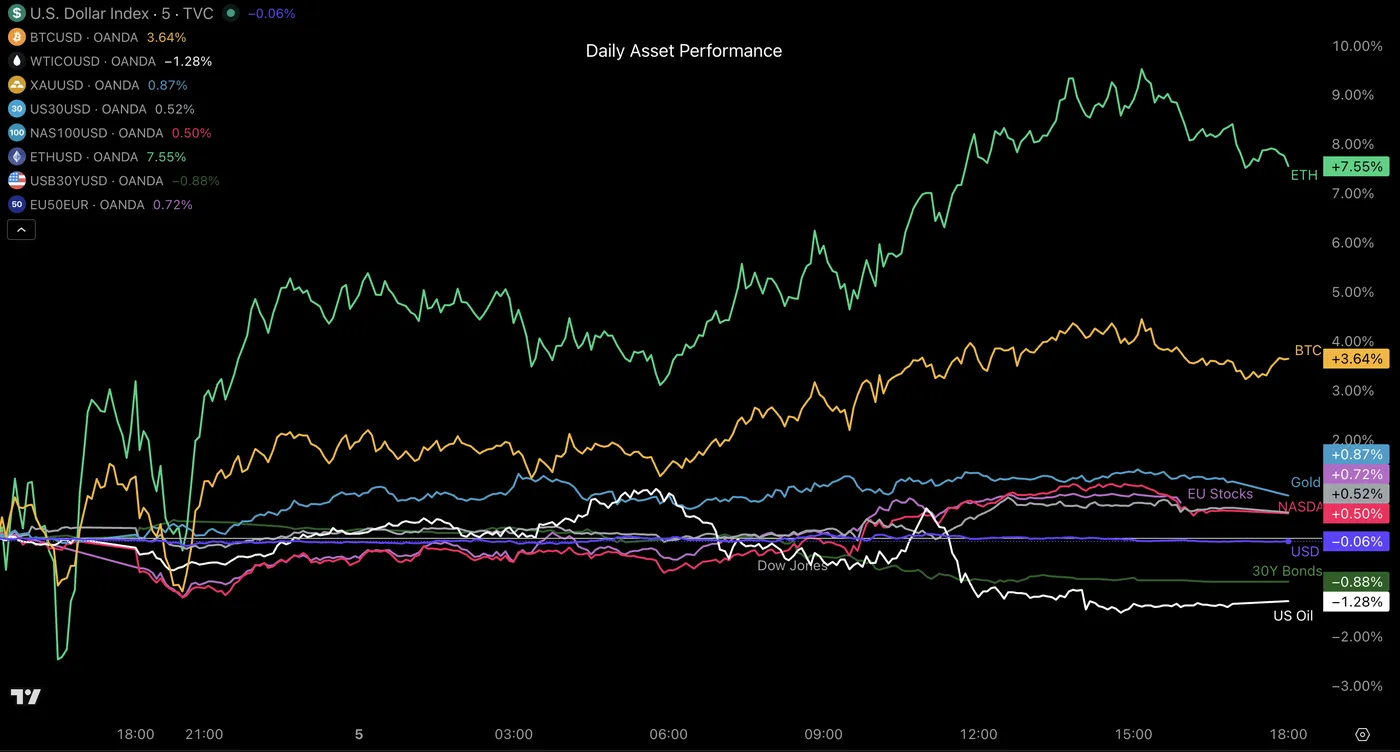

Cross-Assets Daily Performance

Cross-Asset Daily Performance, November 5, 2025 – Source: TradingView

Today’s flows got right back to the 2025 regular flows: Risk-assets rallying among gold (Cryptos largely overperformed) and the losing combo being US Treasuries and Oil.

Despite the better US-China relations and very decent numbers, oversupply from OPEC+ and Russia keep on dragging oil prices lower after every rebound.

A picture of today’s performance for major currencies

Currency Performance, November 5 – Source: OANDA Labs

Today’s trading saw low amplitude in Forex movement. Nonetheless, the US stopped its multi-week ascent (which didn’t leave much space for other majors).

The Japanese yen continues to underperform since PM’s Takaichi got appointed, with USD/JPY trading in the 154.00 handle, up 4.56% since beginning October.

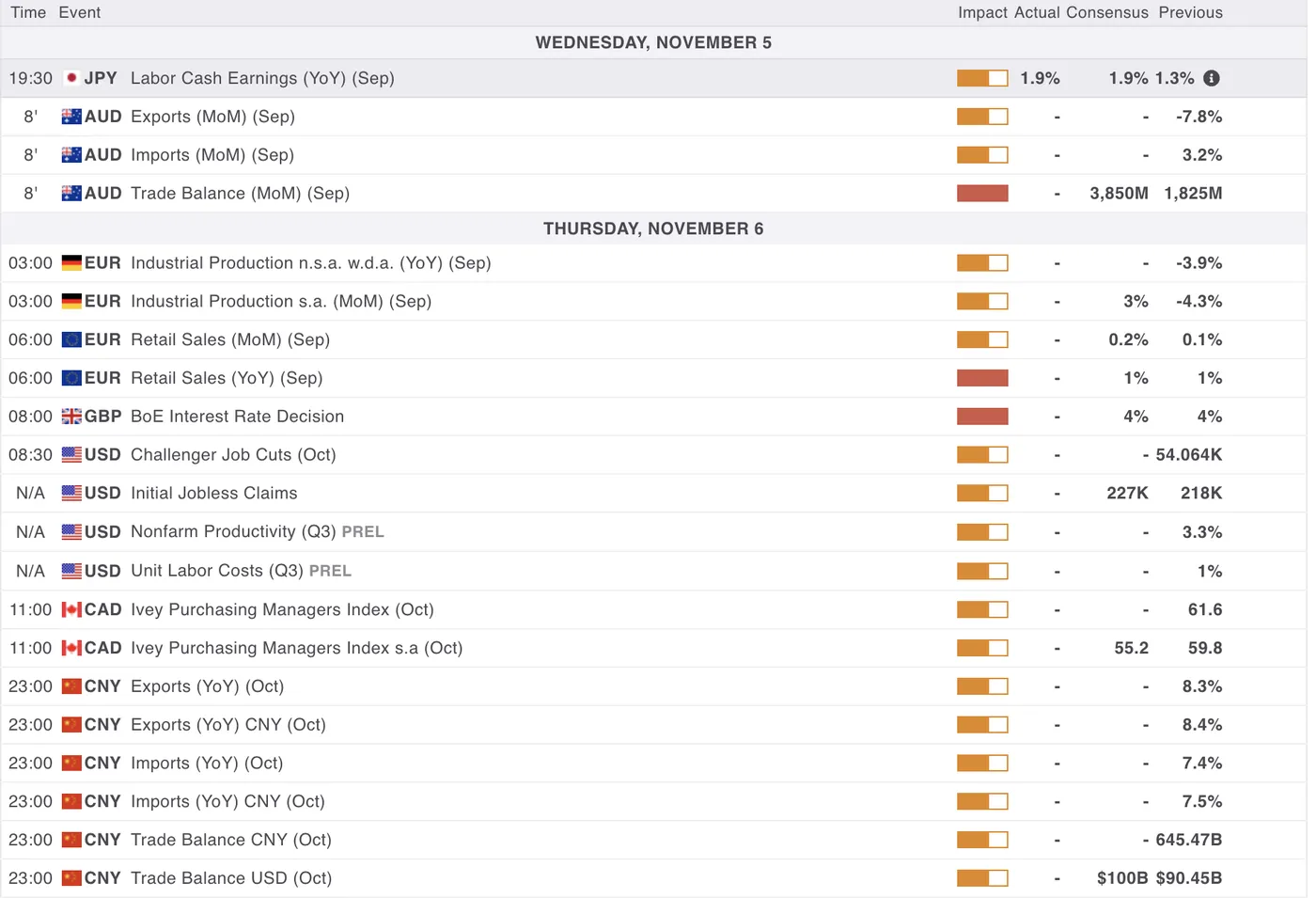

A look at Economic data releasing through tonight and tomorrow’s session

For all market-moving economic releases and events, see the MarketPulse Economic Calendar.

Once again, participants won’t be able to access the normally weekly Jobless Claims release (the 6th consecutively not released) amid the ongoing shutdown.

The FX program is expected to be quite filled with Australian trade data releasing tonight, and overnight’s EU retail sales data.

The North American session will first welcome the Bank of England Rate decision with the release of the Monetary Policy Report (Very important for the GBP).

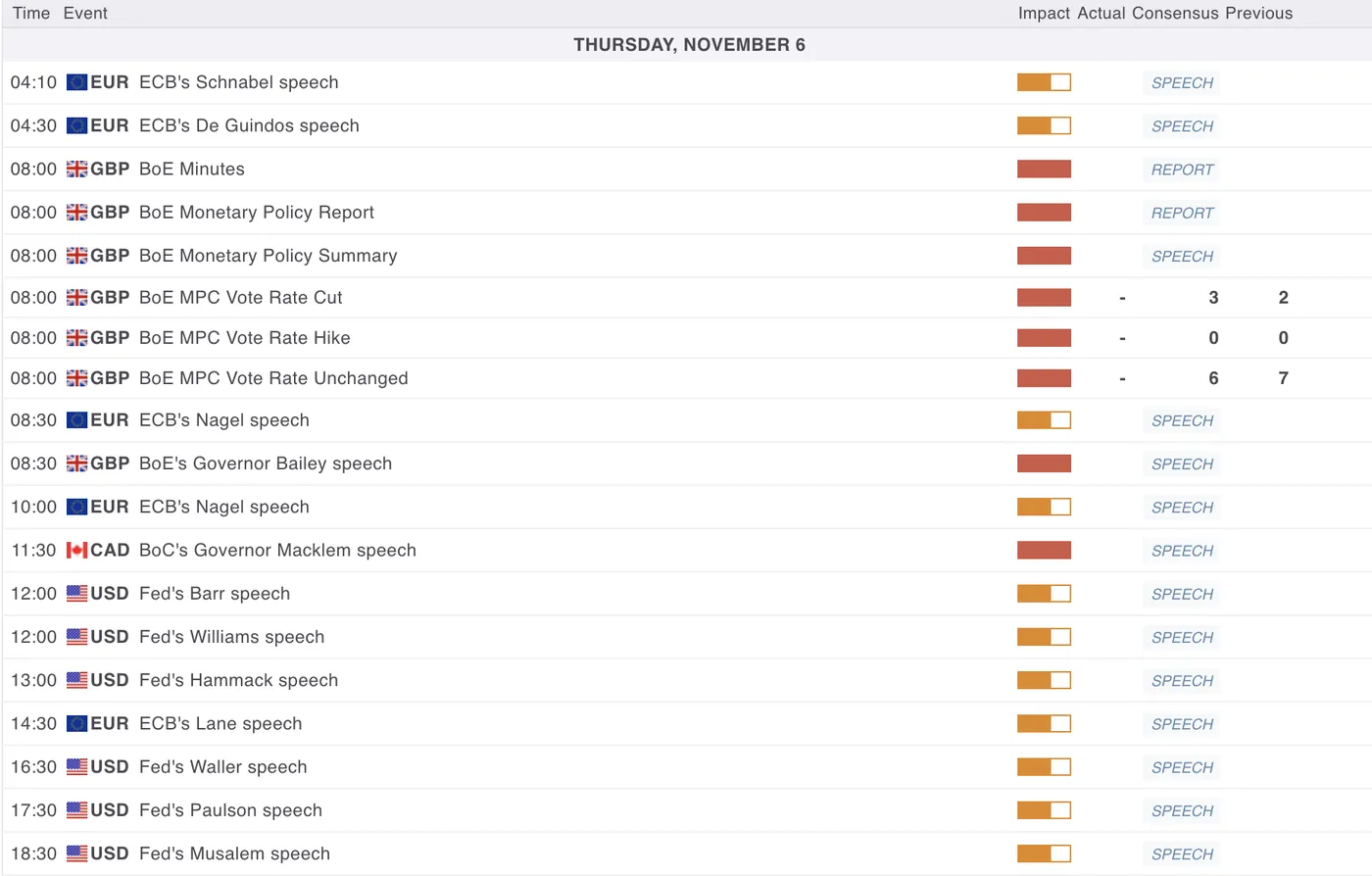

Throughout the rest of the session, expect a flurry of speakers from the Bank of England, Bank of Canada, the usual heavy FEDspeak and a few from the ECB.

All speeches from Central bank speakers in tomorrow’s session

Safe Trades!