. Uncertainty over the extent and timing of future rate cuts didn’t stop the S&P 500 from briefly notching a new all-time high but pared those gains towards the end of the week. The yield curve steepened by roughly 10 bps, with the 10-year currently sitting at 4.19%.){kind=link}

Canadian Highlights

- The Bank of Canada kept interest rates unchanged, signaling caution about recent resilience in the Canadian economy in light of the ongoing trade uncertainty.

- The policy rate looks set to remain steady next year. Soft demand is likely to lean against inflationary pressures from increased costs associated with trade adjustments, netting out to keep inflation near target.

- Canada’s trade position improved in September, although most industries still lag be-hind last year’s performance.

U.S. Highlights

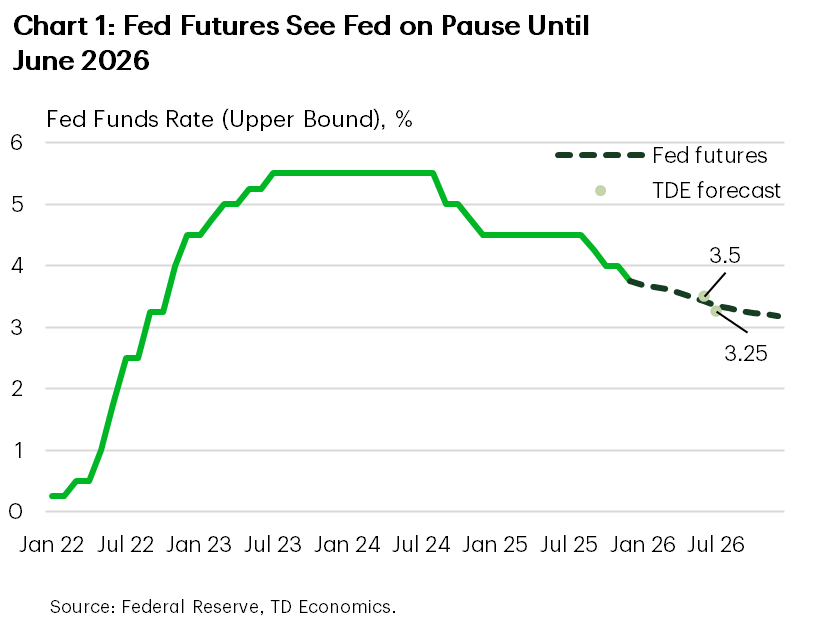

- The Federal Reserve delivered a third consecutive quarter-point rate cut this week, bringing the target range to 3.50%-3.75%.

- Three voters dissented on December’s decision and there was considerable dispersion on the expected rate path for 2026, underscoring the growing divide among FOMC members.

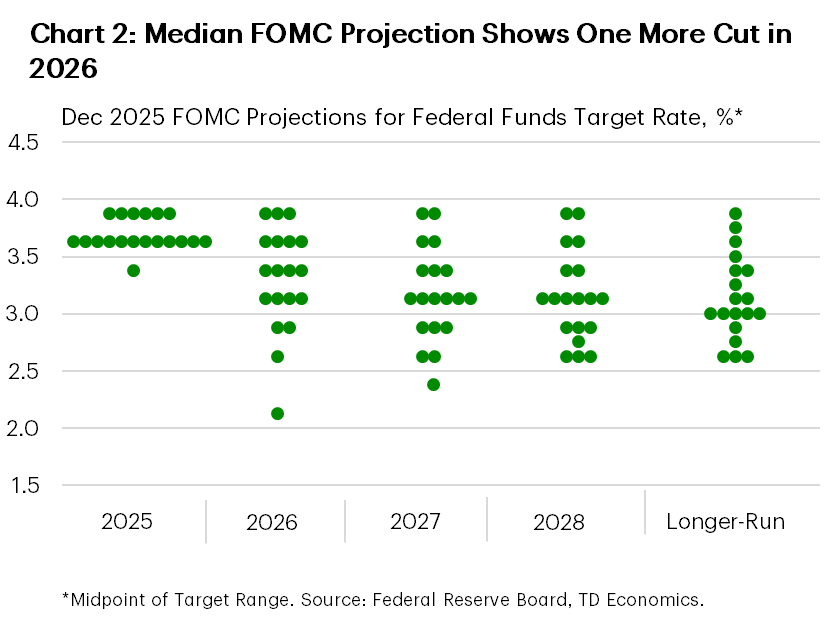

- The median FOMC projection on the federal funds rate suggests just one additional cut in 2026. For now, we think the Fed is on hold until June.

Canada – Bank of Canada Brings Tidings of Comfort (But Not Joy)

We are in the home stretch before Canadian economy watchers can kick back with a festive beverage and reflect on 2025. This past week featured the Bank of Canada’s last interest rate decision of the year and an overdue report on Canada’s trade picture. Overall, the week’s events confirm that Canada’s economy is holding up well despite global uncertainties. This was echoed in the Bank of Canada’s (BoC) interest rate announcement, which brought tidings of comfort, if not exactly joy.

Governor Macklem did not bring any surprises down the chimney, leaving the policy rate unchanged as expected. The central bank acknowledges ongoing concerns about tariffs and trade uncertainty, which continue to dampen business investment intentions. Despite improvements in the labor market, hiring remains subdued, signaling that employers are not yet eager to expand their workforce.

Inflation also remains a key focus for the BoC. While some volatility is anticipated in the coming months, the Bank expects underlying inflation to remain steady near 2.5%. The Governing Council believes that the current interest rate is appropriate to keep inflation close to target and to help the economy adapt to ongoing shifts.

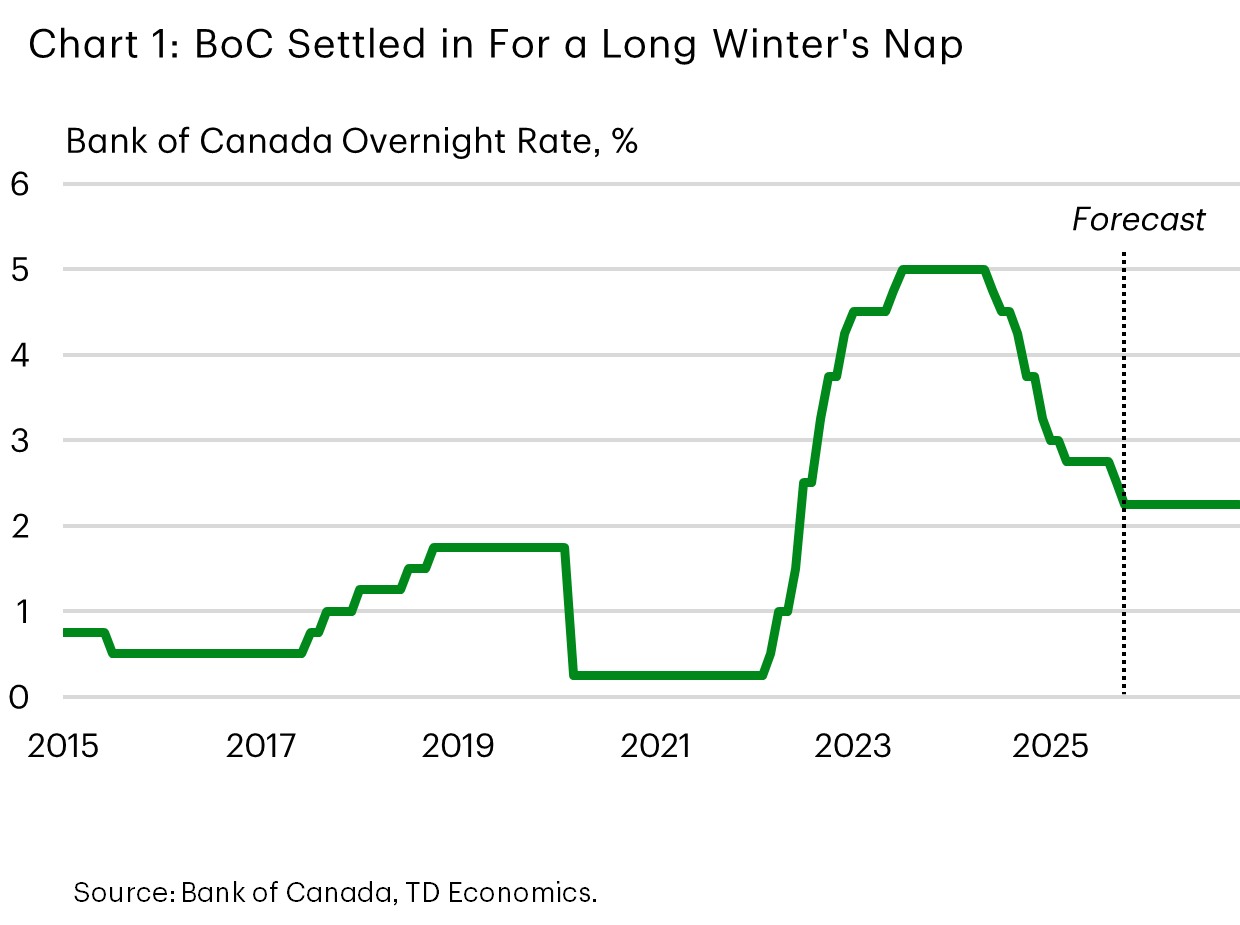

Looking ahead, recently robust employment reports have prompted markets to price in the likelihood of one rate hike next year. However, with trade uncertainties persisting and the review of the CUSMA (USMCA) trade agreement approaching, the BoC is committed to a data-driven approach. For now, Canadians should expect the policy rate to be settled in for a long winter’s nap, unless significant changes in economic indicators warrant a shift (Chart 1).

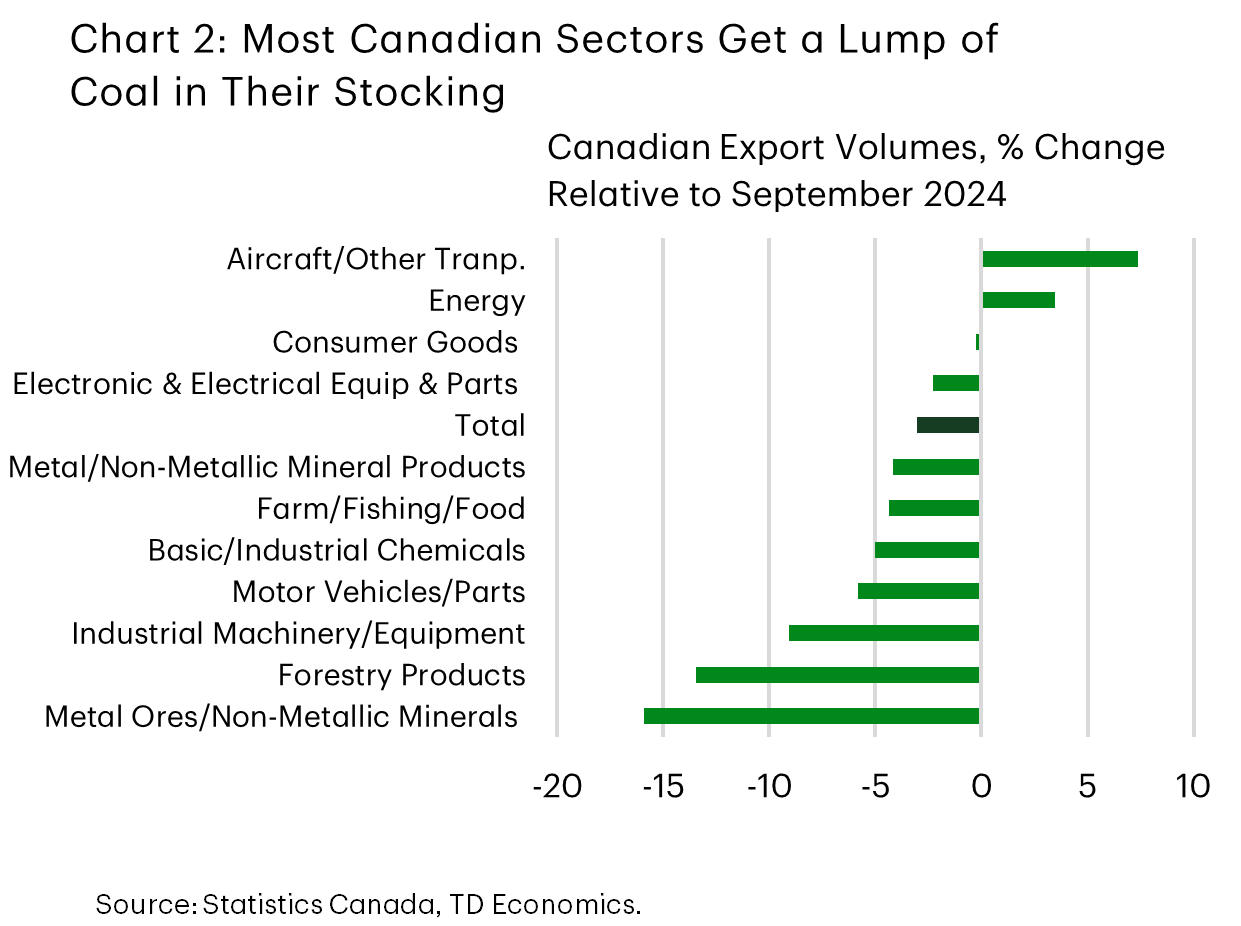

The key piece of data this week was international trade data for September, which had been delayed by the U.S. government shutdown. Canada’s trade position strengthened notably, moving from a $6.4 billion deficit in August to a $153 million surplus. Exports surged by 6.3% month-over-month, with gains distributed across most product categories, especially unwrought gold, crude oil, and aircraft/transportation equipment. That is good news, but looking at exports relative to a year ago, most industries are still in the not-so-festive red (Chart 2).

The latest figures confirm that net trade contributed positively to real GDP growth in the third quarter and suggest a potential upward revision to Q3 GDP figure. While some volatility may remain, the most severe impacts of tariffs appear to be in the rearview, though the future of trade relations will depend on the outcome of the USMCA review.

As Canadians get ready to sip some egg nogg and reflect on 2025, what stands out is the economy’s continued resilience despite global uncertainties. Interest rates have stabilized at a lower level and trade is recovering. The trajectory will depend on how these trends evolve, but for now, the week brings tidings of cautious comfort, in the economy’s underlying strength.

U.S. – Fed Delivers on December Cut, But Signals Slower Pace Ahead

The main event this week was the Federal Reserve’s much anticipated interest rate announcement. While policymakers elected to push ahead with a third consecutive quarter-point rate cut – bringing the target range to 3.50%-3.75% – the move came amid an increasingly divided FOMC (Chart 1). Uncertainty over the extent and timing of future rate cuts didn’t stop the S&P 500 from briefly notching a new all-time high but pared those gains towards the end of the week. The yield curve steepened by roughly 10 bps, with the 10-year currently sitting at 4.19%.

Accompanying the statement, the FOMC also released a revised set of economic forecasts, known as the Summary of Economic Projections (SEP). The SEP represents the median of the individual forecasts submitted by FOMC participant. Relative to the September projection, economic growth for 2025 saw a very modest upgrade (1.7% vs. 1.6%), while there was a notable upward revision to 2026 (2.3% vs. 1.8%). The expected trajectory for the unemployment rate was unchanged, while the inflation forecast is expected to remain above the 2% target through 2027 despite being nudged a tick lower in both 2025 and 2026. Importantly, the median projection on the federal funds rate remained unchanged at 3.6% for 2026 and 3.1% for 2027 – suggesting just one additional cut in each of the next two years (Chart 2). However, there was considerable dispersion across those projections, with the range of estimates for the appropriate level of the policy rate by the end of 2026 spanning 175 bps – a wider range than in September.

The growing divide among policymakers was further underscored by the fact that three participants dissented against December’s decision. Regional Fed Presidents Schmid and Goolsbee favored keeping the policy rate unchanged, while Governor Miran voted for a larger 50 bps cut. But as seen in Chart 2, there were a total of four Fed members who came into the meeting thinking a cut was not required.

The subtle shift in the dots wasn’t lost on market participants. Come January, the four regional presidents who are currently voting FOMC members (Goolsbee, Schmid, Collins, and Musalem) will be replaced by Paulson of Philadelphia, Hammack of Cleveland, Kashkari of Minneapolis and Logan of Dallas. While we don’t know for certain if any of the incoming Fed Presidents ‘quietly’ opposed the December cut, recent speeches by both Logan and Hammack have struck a more hawkish tone. Moreover, Kashkari had advocated for a pause on rate cuts ahead of the October meeting. This suggests that the hawkish tilt from Fed presidents isn’t going away despite the turnover in voting members.

However, this needs to be balanced against a new Fed Chair, who will be in seat May 2026, and is likely to have a more dovish policy stance. Moreover, should Chair Powell elect to not serve out the remaining two years of his term on the board of governors, it will create another vacancy for which President Trump can appoint a new board member. The takeaway from all this is that the division among FOMC members is only likely to deepen next year, putting in question both the timing and extent of further policy easing.