{kind=link}

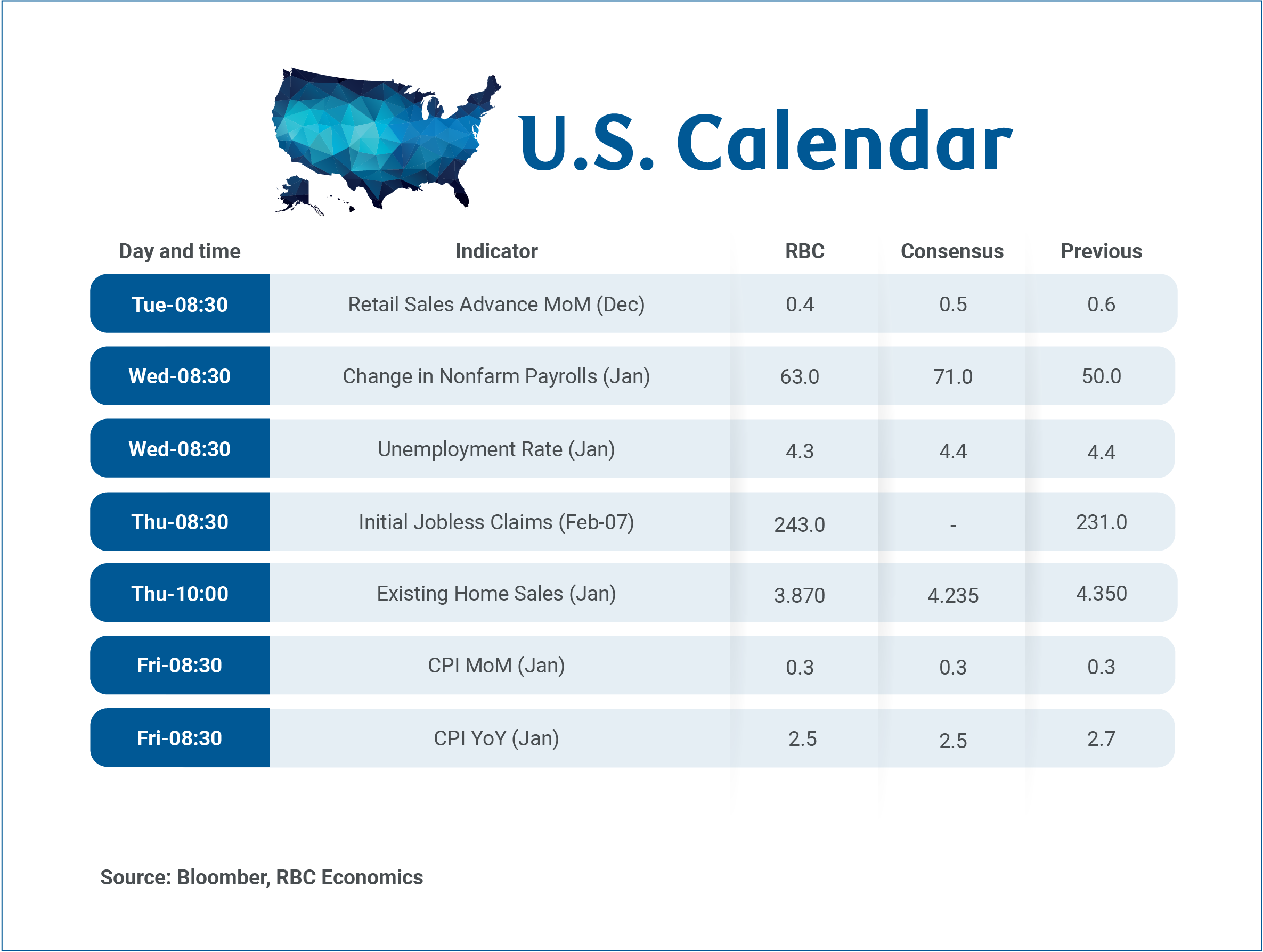

The coming week is relatively quiet for Canadian economic data releases with no major reports scheduled. As a result, attention will shift to developments south of the border with January’s U.S labour market data on Wednesday and inflation on Friday.

Both releases will be closely watched by the U.S. Federal Reserve ahead of the next interest rate decision in March, but also by the Bank of Canada for implications on Canadian growth and the inflation outlook.

Headline U.S. price growth likely slowed in January, driven by a 3% seasonally adjusted pullback in gasoline prices from December. But, we look for core price growth to remain unchanged at 2.6%—stretching readings above the Fed’s 2% inflation target to almost five years.

Tariff passthrough to consumer prices has been limited so far, but business surveys continue to flag further increases in the pipeline, and core producer price inflation continues to run well above consumer price growth (3.5% in December).

We look for food inflation to hold close to 3%. Measured year-over-year shelter inflation is still above 3% despite being lowered in November and December by a methodological quirk due to the U.S. government shutdown in October that should reverse by April.

Comparing inflation in Canada and the U.S.

There are clearly key differences in the current drivers of inflation in Canada and the U.S. Tariff increases in Canada over the last year have been limited, and business surveys like the BoC’s Business Outlook Survey point to easing business input cost inflation.

But, there are some similarities. Food prices have also been rising sharply in Canada, driven by the lagged impact of what are still relatively high global agricultural commodity prices, and low Canadian cattle inventories. They are adding upward pressure to beef prices rather than tariffs.

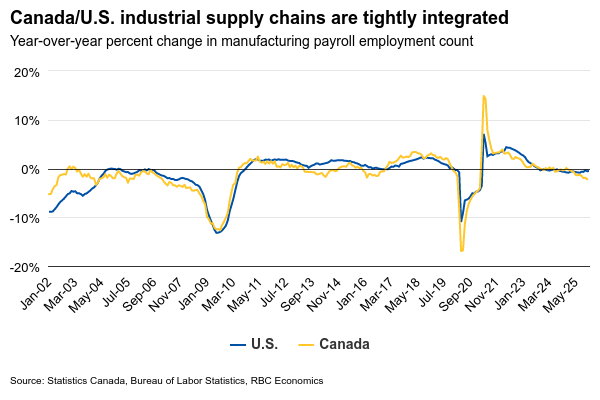

Broader U.S. tariffs can still spill over to higher costs for Canadian producers through integrated supply chains, and the BoC has cited restructuring costs to avoid tariffs as a key upside risk to future Canadian inflation.

U.S. jobs should tick higher despite recent indicators

We (and the BoC) will also be closely watching the delayed by the brief government shutdown over the past week (previously scheduled for Feb. 6) U.S. labour market report for signs the market is stabilizing. Particularly, in the manufacturing sector where ties with the Canadian economy are closest, and where employment counts have been steadily falling.

A run of weaker U.S. labour market data over the last week (spike in announced layoffs in January, higher initial jobless claims in the latest week, and a pullback in job openings) are a reminder the U.S. market has softened. But, private sector job openings data (indeed.com) looked better in January, and we continue to expect an 63k increase in overall employment in January.