{kind=link}

Summary

U.S. Week in Review:

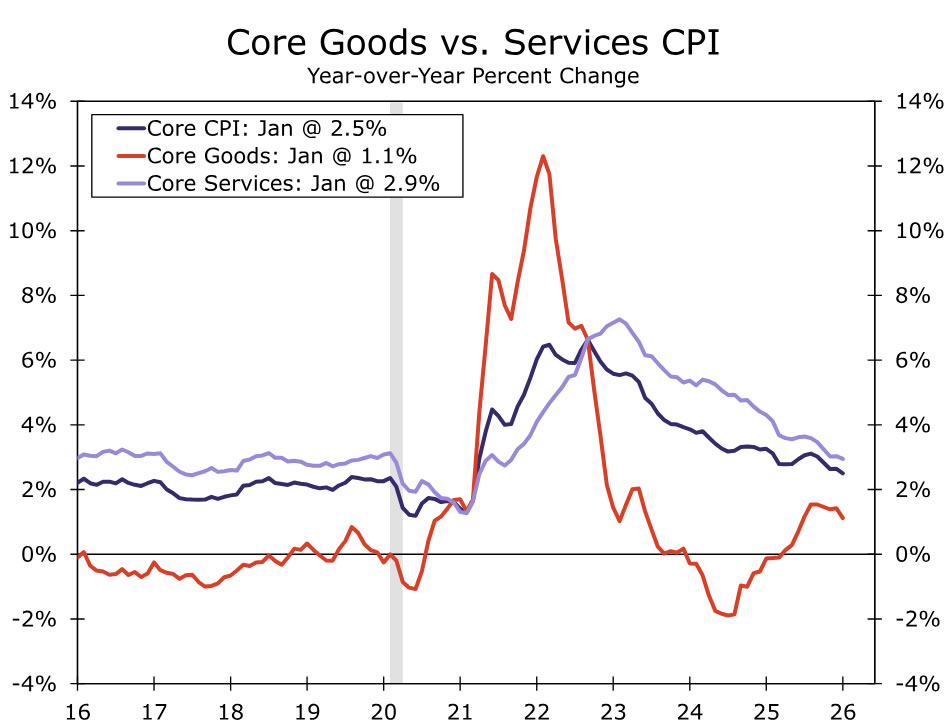

- Stronger labor market data and cooler inflation reduce the odds of near-term Fed easing. Job growth surprised to the upside (+130K), unemployment fell (4.3%) and recent hiring looks more stable than in outright deterioration—strengthening the Fed’s case to stay on hold. At the same time, CPI cooled more than expected with the annual rate on core inflation touching its lowest in nearly five years (2.5%), reinforcing the disinflation trend and keeping the door open to cuts later in the year. The latest data suggest a March rate cut looks increasingly unlikely, but the prospects for additional rate cuts remains alive for later in the year.

U.S. Week Ahead:

- December Trade Balance (Thursday)

- December Personal Income & Spending (Friday)

- Q4 GDP (Friday)

U.S. Week in Review

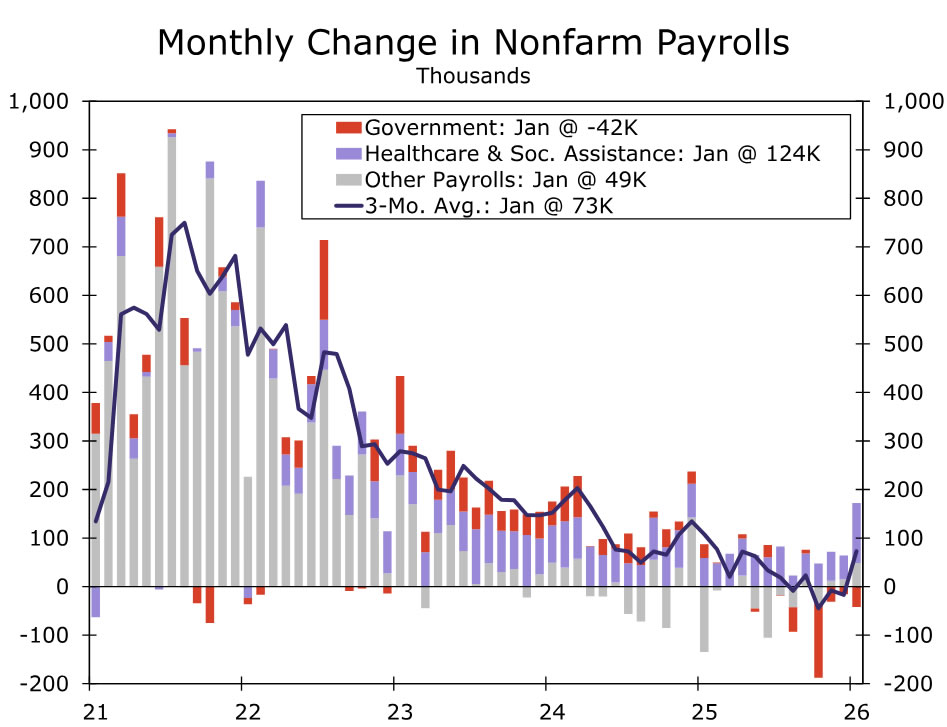

Strong Payrolls Dampen Hopes for Near-Term Rate Cuts

The upshot of a mini-government shutdown last week was the somewhat unusual alignment of indicators that brought fresh data on both jobs and inflation inside a span of 48 hours. This pivotal double header showed improvement on both of the Fed’s mandates. The job market improved, even if hiring remains quite concentrated in the healthcare and social services sector, and inflation cooled more than expected. Hawks on the FOMC can now point to a labor market that is regaining its footing, but doves can cite the improvement in bringing inflation closer to target as a rationale for adjusting rates down another notch closer to neutral.

For months now, we’ve been saying that the window for additional Fed cuts is closing. Taken together, this week’s data has likely pushed the next rate cut out until June, with the prospects for any further rate cuts in this cycle remaining dependent on how the data evolve over the next few months. If the breadth of robust hiring extended beyond just a few sectors, we’d say the window for additional cuts is closed. For now though, the tepid pace of hiring ex-healthcare does not warrant such conviction.

January payrolls handily exceeded modest expectations with a +130K gain in net hiring. This lifted the three‑month average to 73K (chart) and pushed the unemployment rate back down to 4.3%—where it was in August 2025 before the FOMC cut rates at its three subsequent meetings. While revisions were deeply negative, they were largely anticipated and did little to change the forward signal: job growth appears to be stabilizing rather than rolling over. Inflation data were more constructive. Headline and core CPI both cooled in January, and core inflation is now running at its lowest annual level since early 2021 (chart). While core PCE inflation is likely to come in stronger for January (~0.37% m/m) due to different weightings, source data and seasonal adjustment factors, the disinflation narrative remains intact. That said, the combination of firm labor data and still-above-target inflation makes a March rate cut look highly unlikely, even as it preserves optionality for cuts later in 2026.

The Employment Situation report may hoard the limelight especially with a big upside surprise, but other measures of the jobs market have not been quite so rosy. Wage pressures continue to fade. The Employment Cost Index undershot expectations in the fourth quarter, with compensation growth slowing to a 3.4% year-over-year rate—the weakest pace since 2021. Cooling wages and benefits (outside of healthcare) alongside solid productivity gains ease concerns about a labor-cost-driven inflation resurgence. But it’s these signs of a gradually moderating labor backdrop that keeps downside growth risks on the Fed’s radar. The latest consumer data point to some weakness with retail sales stalling in December. But, aggregate holiday spending rose 3.6% in November and December compared to a year-earlier, broadly in line with our earlier expectations. The year-end weakness appears narrow and goods-led rather than a broad retrenchment, leaving the outlook for consumer demand largely intact heading into 2026.

U.S. Week Ahead

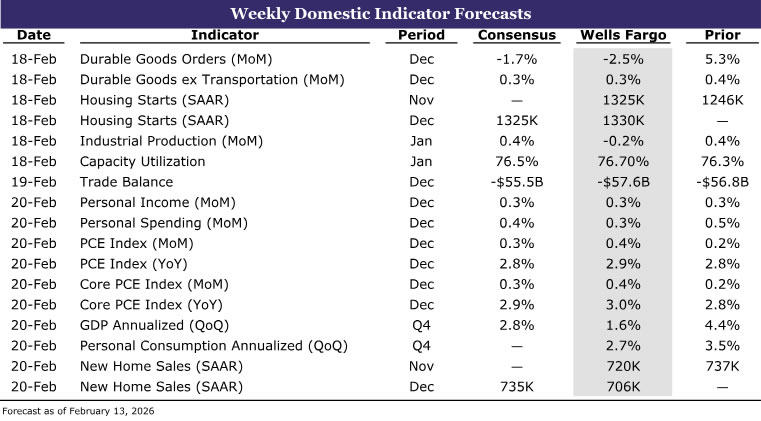

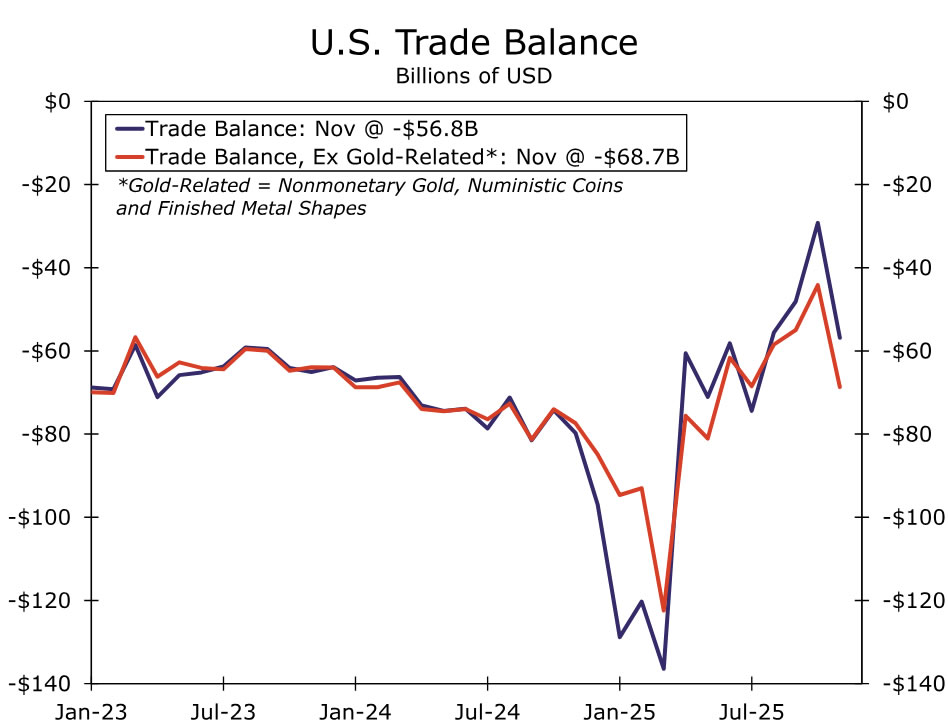

U.S. Trade Balance • Thursday

Recent trade data have been noisy, but the signal remains intact. After narrowing sharply in October, the trade deficit widened again in November, driven largely by volatility in a handful of categories—most notably gold, pharmaceuticals, and high‑tech imports. These swings reflect category‑specific distortions, not a broad deterioration in trade fundamentals. Stripping out gold and high‑tech effects, underlying import demand was soft in 2025, weighed down by tariff uncertainty and slower capital spending outside the technology sector.

Looking ahead, we expect the trade deficit to widen further to -$57.6 billion in December, as these specific factors continue to influence the year‑end data. However, the outlook for early 2026 is more constructive. Firm consumer demand, a recovery in more traditional areas of capital spending, and inventory normalization—absent evidence of a structural shift toward onshoring—should support a rebound in import growth as we move into the new year.

Personal Income & Spending • Friday

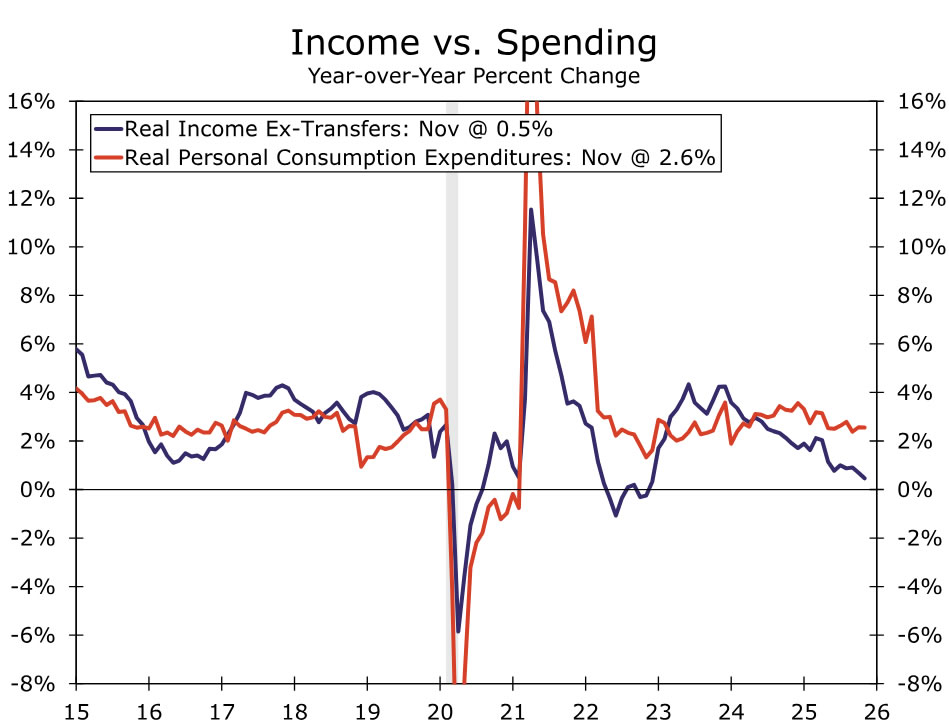

U.S. consumers remain on solid footing heading into 2026. Household spending continues to run at a healthy pace, and we look for nominal personal spending to rise 0.3% in December, leaving real spending roughly flat. While December retail sales were softer than expected and should weigh modestly on year‑end spending, the weakness appears driven by timing and pull‑forward effects rather than a deterioration in underlying demand. As a result, the softer retail print does not meaningfully change our constructive view of the consumer entering the new year.

Income growth remains the key watch point. Soft income gains have required households to lower saving rates, and we expect personal income to rise only 0.3% in December. Even so, the near‑term outlook for consumption remains supportive. Tax relief, easing inflation, and steadier job growth should help offset income headwinds and keep real consumer spending growing at a moderate pace through 2026.

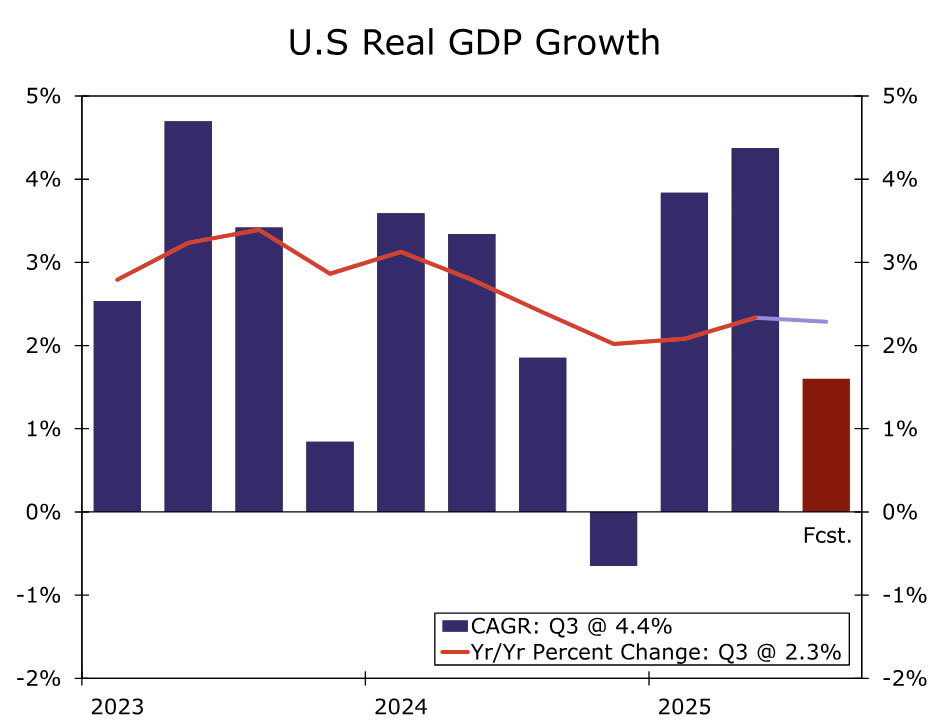

Q4 GDP • Friday

U.S. growth likely slowed at year‑end, but underlying fundamentals remain solid. We estimate real GDP grew at a 1.6% annualized pace in Q4, with most of the weakness attributable to the extended government shutdown from early October through mid‑November, which likely shaved roughly 1.2 percentage points from headline growth.

Stripping out shutdown effects, activity held up well. We expect real PCE to grow at a 2.7% annualized rate, while business investment likely posted a modest gain led by high‑tech equipment and intellectual property. Net exports and inventories remain the key sources of volatility. Beyond tariff uncertainty, a surge in investment‑related gold flows continues to cloud the signal from monthly trade data, while inventories remain inherently difficult to forecast given limited real‑time information. Through this noise, the economy appears to have ended 2025 in a healthy position, growing at a 2.2% average pace over the year.