{kind=link}

Summary

U.S. Week in Review

- The economic data calendar was relatively light this week. However, the major indicators that were published showed that inflation pressures continue to percolate with few signs of the labor market exiting its soft patch. Meanwhile, the Fed communication channel provided comments underscoring the lack of consensus on which side of the Fed’s dual mandate demands the most attention, given still-elevated inflation and labor market risks.

U.S. Week Ahead

- Next week will bring some key readings on the economy’s early year momentum. We look for the February ISM surveys to show a modest firming in services activity and that the factory sector is continuing to reemerge from the prior year’s slump. Yet, the February employment report is likely to indicate that, while the labor market remains roughly in balance, job growth is struggling more than last month’s jump in payrolls indicated. We believe the temperate labor market backdrop along with adverse winter weather led to a muted rise in January retail sales.

U.S. Week in Review

The economic data calendar was relatively light this week. However, the indicators that were published showed that inflation pressures continue to percolate with few signs of the labor market exiting its soft patch.

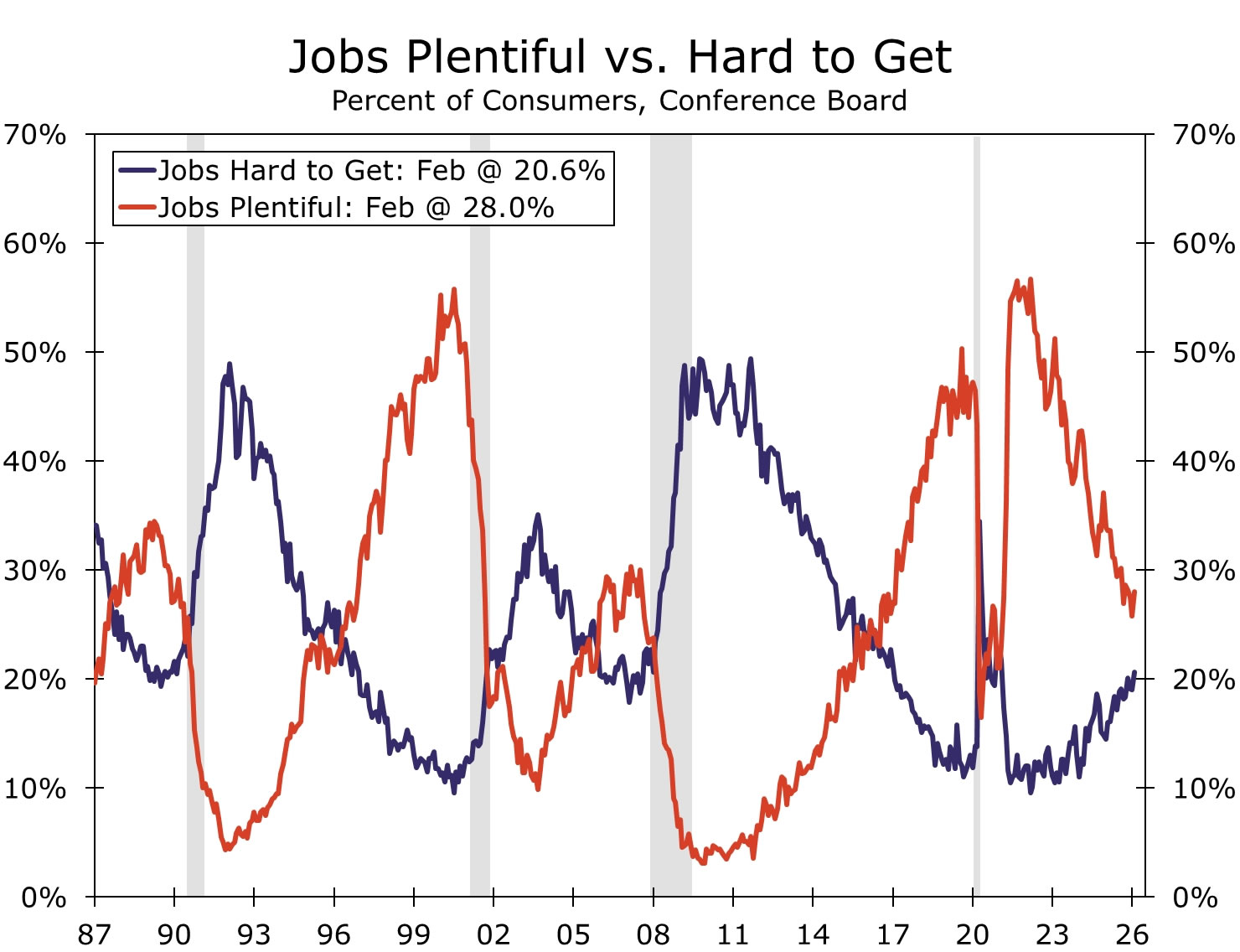

The soft labor market narrative was on display within the details of January’s consumer confidence print. Top-line consumer confidence is still bouncing around at the lower end of its past five-year range but came in a bit stronger than expected during January. The upside surprise was an encouraging development in that it suggests consumers are not feeling any worse about the current state of the economy. That said, the labor differential subcomponent, i.e., the difference between respondents saying “jobs are plentiful” and those saying “jobs are hard to get,” remains a glaring weak spot.

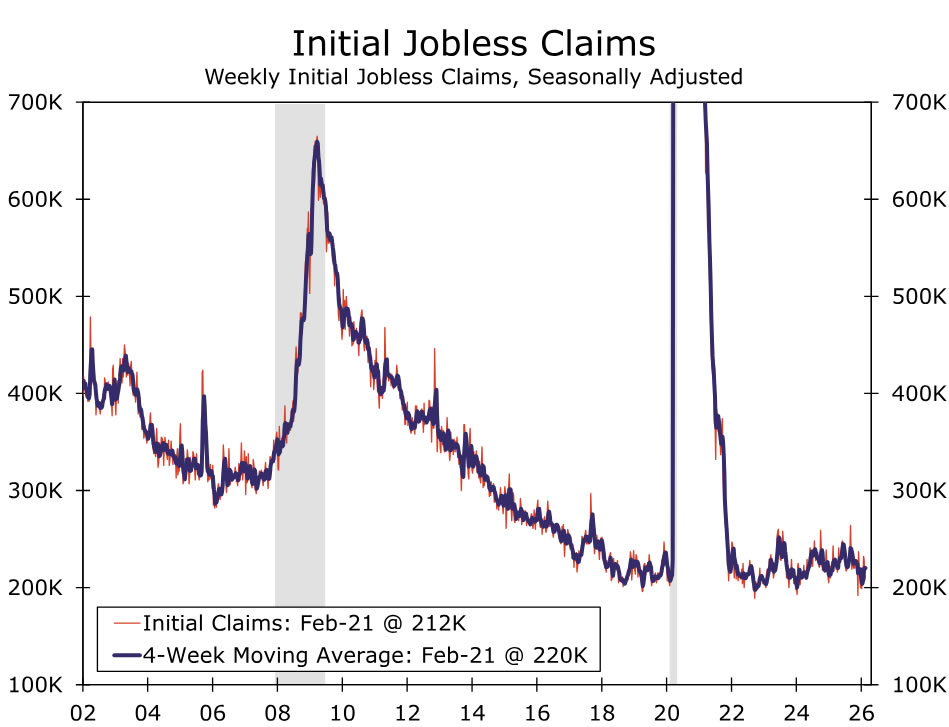

Breaking it down, just 28% of people think “jobs are plentiful,” up slightly during the month but still well off the recent cycle peak of over 50%. This suggests firms are still being cautious on adding to headcounts. But are they reducing payrolls in a material way? “Jobs hard to get” has averaged just 20% over the past several months, up from recent lows but hardly consistent with skyrocketing unemployment. In addition, initial jobless claims declined to 212K during the week ended Feb. 21, further evidence that overall unemployment is not surging higher. The message is that the labor market is currently lethargic, with very slow rates of new hiring. But deep and widespread layoffs (beyond a select few industries) do not appear to be happening either.

The thin flow of major indicators allowed plenty of time to parse through a full week of Fed speak. Generally speaking, the comments provided underscored that there is no clear consensus at the FOMC and among the regional bank presidents on which side of the Fed’s dual mandate demands the most attention. For example, Chicago Fed President Goolsbee stated “I remain optimistic that there can be more rate cuts this year. But that hinges on seeing actual progress on inflation that shows we are on a path back to 2%.” Governor Miran seemed more concerned about downside risks to employment, saying “I think it’s way too early to sort of sound an all clear that the labor market doesn’t need more support from the Federal Reserve” and “four cuts I think are appropriate and I’d rather get them sooner rather than later.”

However, comments from Governor Waller at the NABE policy conference in D.C. on Monday especially stood out to us. “If the labor market data for February are consistent with the stronger job creation and low unemployment rate initially reported in January, indicating that downside risks to the labor market have diminished, it may be appropriate to hold the FOMC’s policy rate at current levels and watch for continued progress on inflation and strength in the labor market. But if the good labor market news of January is revised away or evaporates in February, it would support my position at the FOMC’s last meeting, that a 25-basis-point reduction in the policy rate was appropriate, and that such a cut should be made at the March meeting. As things stand today, I rate these two possible outcomes as close to a coin flip.”

In our view, January’s “strong” employment growth may have been overstated and a more moderate payroll gain in February seems likely. For more on our nonfarm payroll forecast, please see below in our Outlook section. Nevertheless, labor market conditions do not appear to be deteriorating and look to have stabilized, albeit within a “low hire, low fire” context. Meanwhile, January’s hotter-than-expected rise in both the headline and core Producer Price Index is the latest reminder that price pressures are still evident and that most inflation measures are still running above the FOMC’s 2% target. From our standpoint, this lowers the likelihood of a March rate cut, though two additional 25 bps cuts later this year are still on the table, given still-present downside risks in the labor market.

U.S. Week Ahead

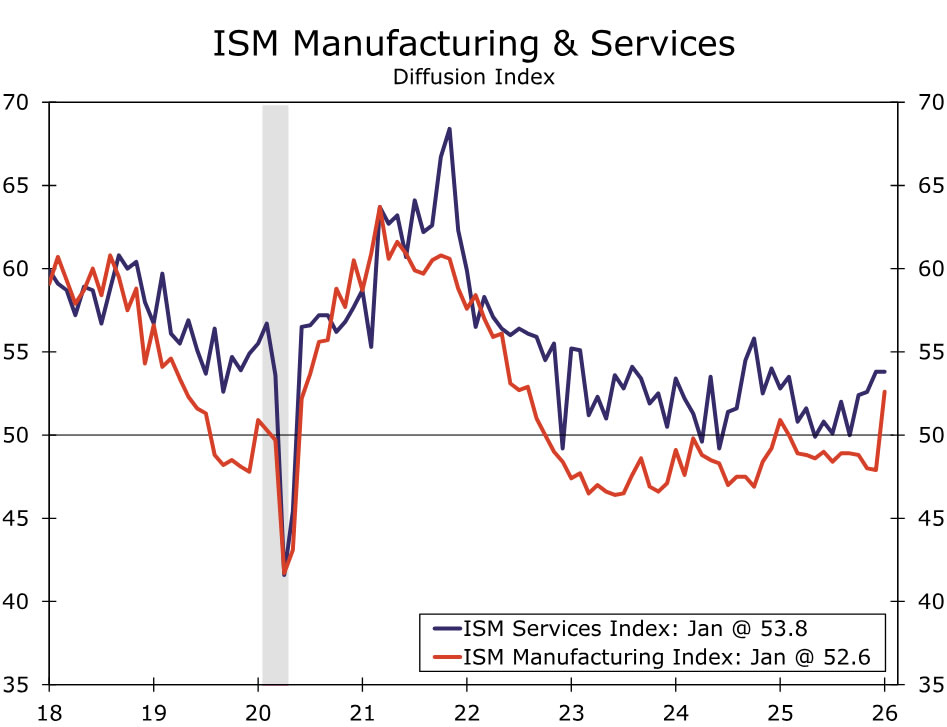

Monday & Wednesday • ISM Surveys

The ISM manufacturing index crossed into expansion territory in January for the first time in 10 months. The improvement comes amid an upswing in capital spending—highlighted by broadening in durable goods orders—as well as restocking efforts in the wake of last year’s tariff hikes. We would not be surprised to see a little giveback in February following last month’s leap, however, and estimate a February print of 52.0. The nearly 10-point jump in the new orders component in January overstates underlying momentum in the factory sector in our view. Regional PMIs for February show manufacturing activity continued to expand last month, but a more even-keeled pace.

Non-manufacturing activity continues to hold up better, as indicated by the ISM services index maintaining its 14-month high in January. Although firms remain cautious when it comes to hiring, business activity has been sturdy. We look for the February reading, due Wednesday, to edge up to 54.2.

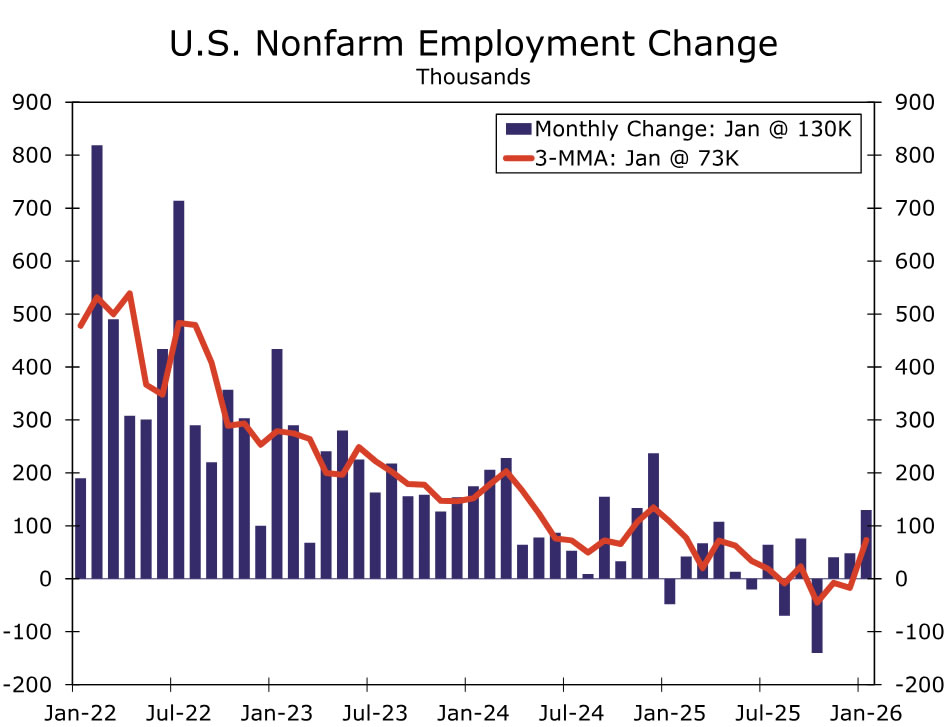

Friday • Employment

We expect the February employment report to show that January’s robust pace of payroll growth overstated underlying momentum in the labor market. While some stabilization in demand for workers is evident, a range of indicators, including JOLTS and consumers’ perception of job availability, continue to point to a gradual loosening in labor market conditions rather than a renewed acceleration in hiring. We look for nonfarm payrolls to rise by 45K in February, with weakness in weather-sensitive industries like construction and leisure & hospitality and some payback in healthcare & social assistance after a significantly above-trend reading in January.

We estimate the unemployment rate held steady at 4.3% in February, but see two-sided risk to this call. The household survey’s measure of employment growth has been running well ahead of its trend the past two months, leaving some scope for payback in February that could push the jobless rate up to 4.4%. However, the implementation of the household survey’s annual population adjustment poses downside risks, given the shift in immigration trends last year. Ratios from the household survey such as the labor force participation rate and unemployment rate are less affected by the population control adjustments than level data, but can move slightly under meaningful changes in the composition of the population.

The roughly balanced labor market should lead to average hourly earnings advancing a trend-like 0.3% in February and 3.7% over the past year. For more information, please see our employment preview.

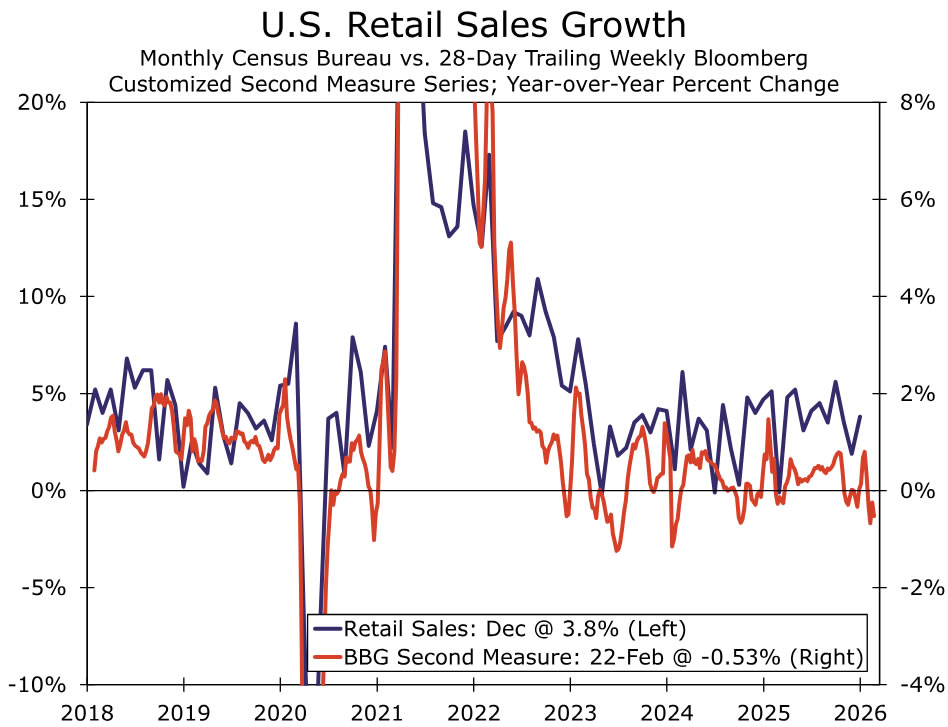

Friday • Retail Sales

The shutdown-delayed January retail sales report is expected to show spending got off to a modest start in 2026. A large winter storm across the central and eastern U.S. likely crimped activity, with auto sales in January already reported to have fallen to nearly a three-year low. Lower gasoline prices will also have weighed on sales, leading us to expect just a 0.1% increase in total retail sales last month.

Yet, consumers are still finding ways to spend despite the cooler jobs market leading to slower income growth and a dampened consumer mood. High-frequency credit card data showed some modest firming in spending in January, leading us to expect retail sales ex-autos rose 0.3% last month. We expect retail sales to show more signs of life in the coming months as larger tax refunds and stabilizing labor market conditions support more discretionary spending.