It’s a busy week ahead for Canadian economic releases, highlighted by the February inflation report on Monday and the Bank of Canada’s interest rate decision on Wednesday.

Canada’s national balance sheet accounts will also be released on Monday, providing an updated snapshot of household and financial sector health.

The BoC will be watching the Consumer Price Index report closely ahead of its policy decision, but we expect a tick lower in headline CPI growth to 2% (right at the 2% inflation target) in February won’t sway the central bank to move from the sidelines.

Recent inflation readings have been distorted higher by the GST/HST tax holiday a year ago, which temporarily lowered price levels, and the removal of the consumer carbon tax from energy prices last April that continues to lower year-over-year energy prices.

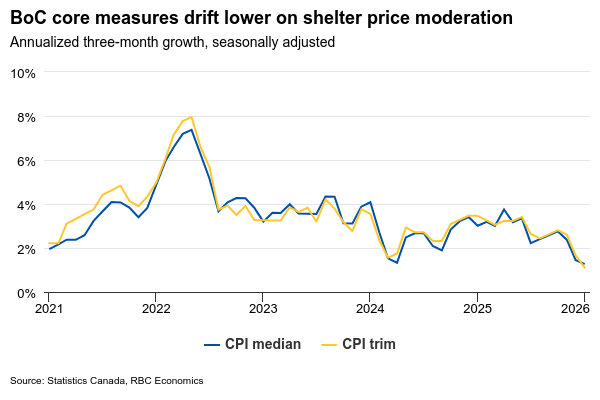

The BoC’s “core” median and trim measures control for tax changes, and have also been drifting lower to 2.5% on average in January, but driven largely by moderation in shelter price growth. Core services excluding shelter growth was still above 3% in January by our count.

Pockets of price growth remain elevated, particularly groceries still up almost 5% from a year ago in January. The drag from lower energy prices in recent months will reverse as oil prices spike higher due to conflict in the Middle East.

Recent labour market data shows mixed signals with some near-term softness but underlying conditions that support gradual improvement ahead. Employment fell 84,000 in February, adding to January’s 25,000 decline, with full-time positions bearing the brunt of losses. The unemployment rate rose to 6.7% in February from 6.5% in January, though it remains below the Q4/25 average of 6.8% and well below the recent peak of 7.1% in September.

As a result, we do not expect the BoC to make changes to the policy rate at Wednesday’s meeting. Our base case forecast also assumes the policy rate remains unchanged for the remainder of 2026 as inflation continues to trend lower toward target.

Data summary:

We expect the national balance sheet account for Q4 2025 to show household net worth continued upward, bolstered by ongoing equity market gains, albeit at a more moderate pace than robust Q3. The S&P/TSX Composite Index advanced 5.6% during the period, following an 11.8% surge in the previous three months. Nevertheless, a portion of these gains was likely offset by persistent declines in property values with the CREA Home Price Index falling 2.2%, maintaining deterioration similar to earlier periods. The debt service ratio probably decreased in Q4, driven by rising personal disposable income and reduced household non-mortgage borrowing.

Attention will also be on the U.S. Federal Reserve’s policy decision on Wednesday. The Fed held rates steady earlier this year, and recent U.S. data suggests labour market conditions continue to stabilize. We expect the Fed to keep rates unchanged through 2026.

Next Friday, we’ll get Canadian January retail sales, providing some indications of spending momentum in early 2026. Statistics Canada’s advance retail indicator released a month ago indicated sales increased 1.5% in January, reversing the decline in the prior month.

{kind=link}