- Discover our Weekly Market Outlook, exploring themes and events that forged financial flows throughout the week.

- This week saw the commencement of large wartime impacts on volatility. With the FOMC coming up, it’s not easy to expect better conditions ahead.

- Get ready for next week’s action by exploring upcoming events across global Markets.

Week in review – Oil Wrought Havoc on Markets

Now reaching the third week of the US-Iran-Israel conflict, ongoing disruptions to the Energy commodity Market are starting to pose grand problems.

In short, higher Oil prices translate to higher inflation. Higher inflation translates to less profitability. Lower profitability and higher inflation translate into struggling Markets.

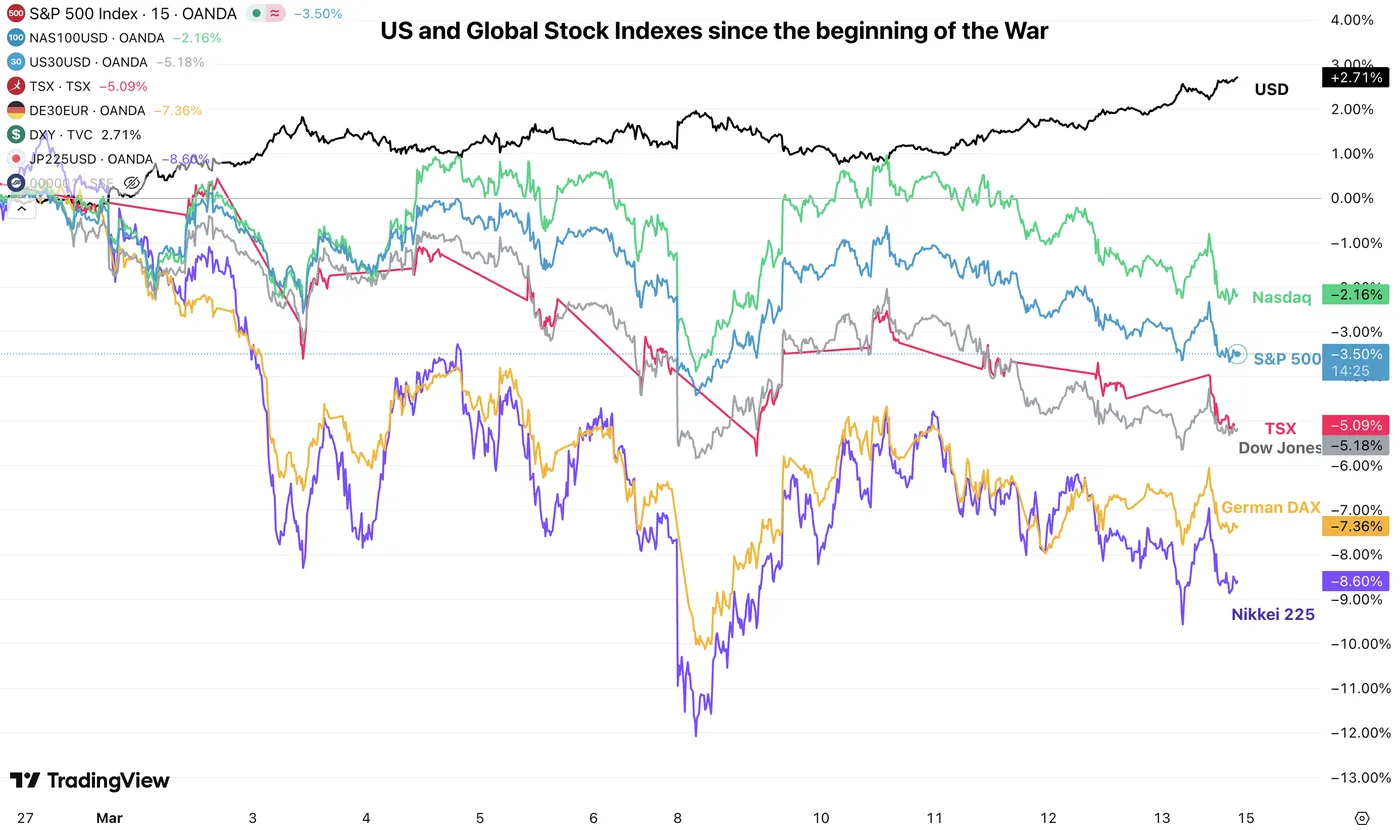

Global Weekly Index Performance – Source: TradingView – March 13, 2026

Stock Markets have taken a hit around the globe. Having remained impressively stable until recently, they are now entering a tougher period ahead.

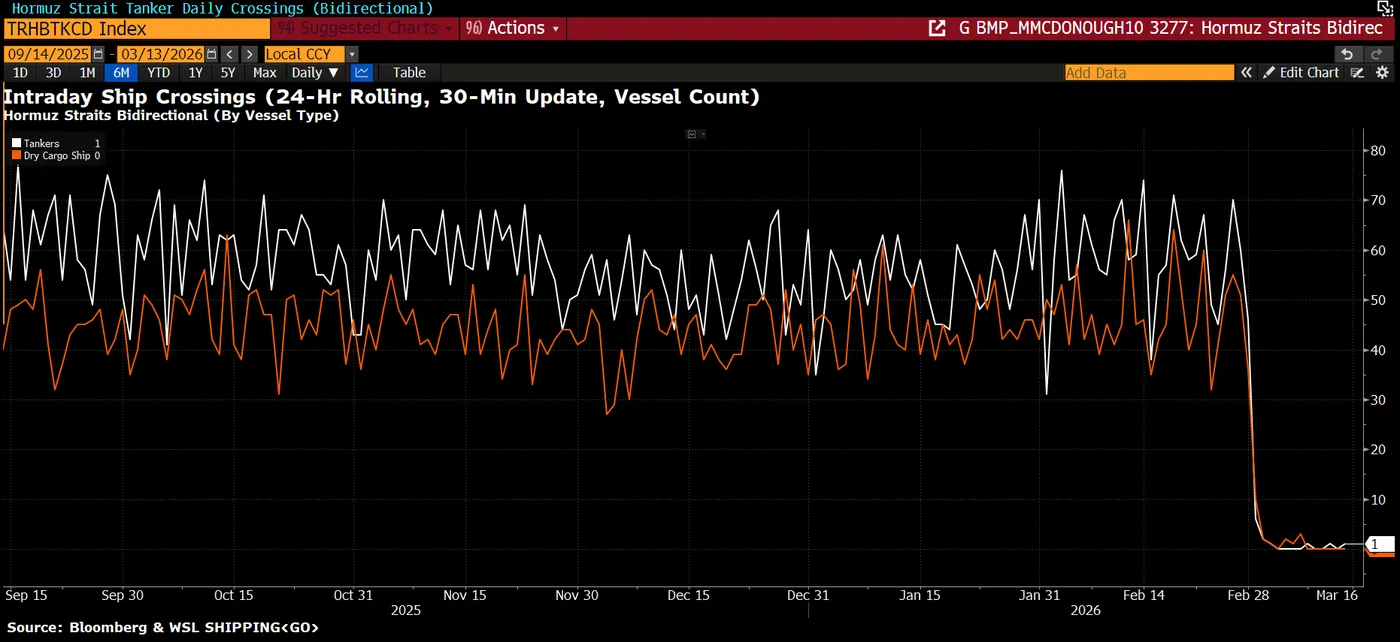

As global Oil supply finds itself in jeopardy, companies will face significantly higher energy prices in the coming period; this effect should last at least as long as the Strait of Hormuz remains in de facto closure (only a few boats and tankers, if any, are crossing every day).

Strait of Hormuz Traffic – Source: Bloomberg – March 13, 2026

The issue is that Markets are starting to reprice the prolonged inflationary effect of such prices – the 1970s consecutive petrol crises taught painful lessons.

After the Oil embargos during that decade, stagflation brought heavy pain to consumers and global markets – and the effects lasted about 10 years, culminating in a significant economic cooldown in the early 80s.

With many ships attacked throughout the week, WTI went from about $80 to today’s $98 – This doesn’t even mention the 30% up and down swings in WTI prices since Monday.

WTI Oil Prices since End February – Source: TradingView – March 13, 2026

To put things into perspective, this is about 72% higher than the prices seen in early January. But the issue is that this only reflects Crude Barrels – refined petrol products have well exceeded this rise worldwide, particularly in Asia.

The issue is that the narrative is shifting from a 4-5-week short war to the actual pricing of a much longer, more painful conflict. The media is blaming the US government for its lack of “exit plans”.

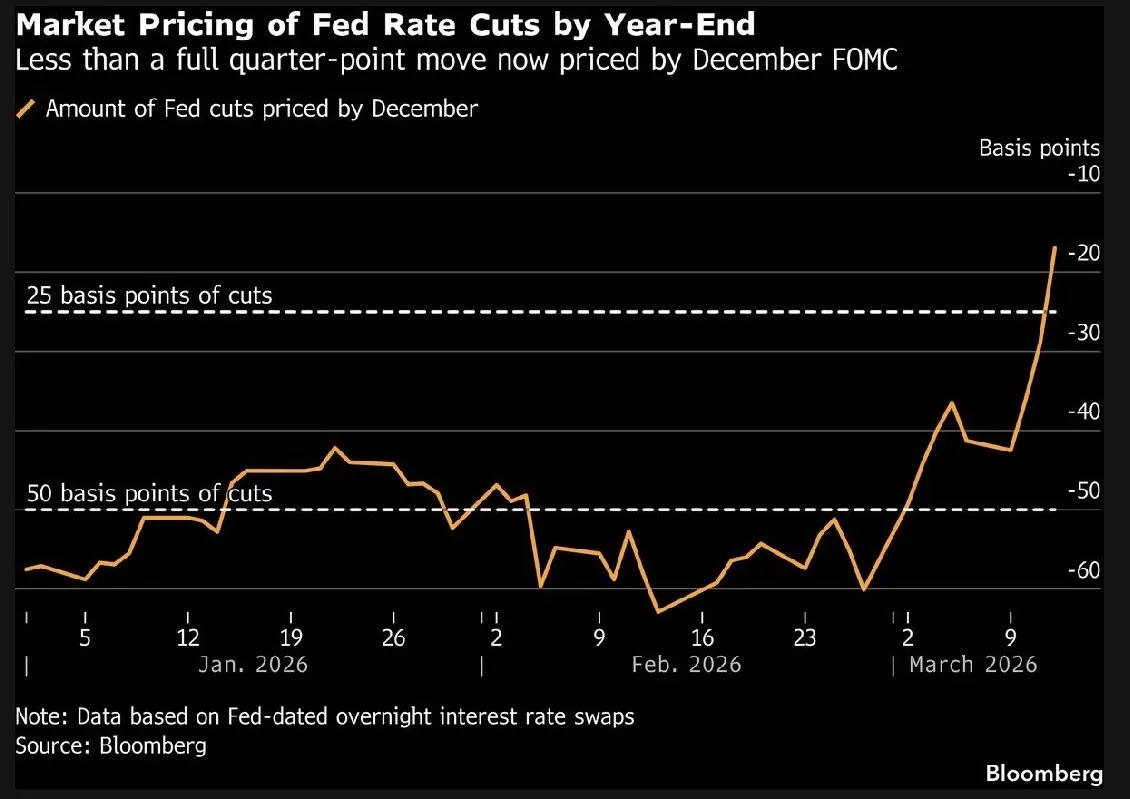

Hence, Inflation expectations are racing higher, Yields are rising above their 2026 peaks, and cuts are being priced out, replaced by hikes, making the overall situation look quite grim.

Rate Cuts are disappearing – Source: Bloomberg – March 13, 2026

The US Fed Funds rate cut pricing went from close to 65 bps to the current below ~20 bps. President Trump is proving Powell right yet again.

The only one enjoying the ride is the Petrodollar, which serves as the denominator for much more expensive Crude and loves the pricing out of cuts. The issue is that, at the current point in the economic cycle, this could pose heavy restraints on the economy.

Tracking upcoming data (particularly labor and manufacturing activity) and next week’s Fed communications will be essential to get a better idea of what’s coming.

The USD correlation with oil rises is once again pretty evident. Hence, it will be essential for traders to monitor the Dollar Index’s movements to track overall Market flows in the coming period.

Oil and Dollar Index Positive Correlation. March 13, 2026 – Source: TradingView

On a brighter note (if we can call it such, there’s nothing really bright about war), the US and Israel are making some strong advances to their strategy, with 90% of drone and ballistic missile launchers destroyed, and similar damage to the IRGC’s military production sites.

The idea is that if Iran doesn’t want to throw in the towel, and the US and Israel insist on inflicting mortifying blows to its enemy, Markets will have to count on the latter to hope for a shorter conflict.

To me, we are not at maximum Market fear yet, but there is a high chance that fears will get overblown. This could provide decent opportunities in the coming weeks.

Oil and Strait of Hormuz developments are, for now, the two largest threats to general Market pricing, so keep the two in check.

(And don’t forget about the Private Credit trouble lurking out from far)

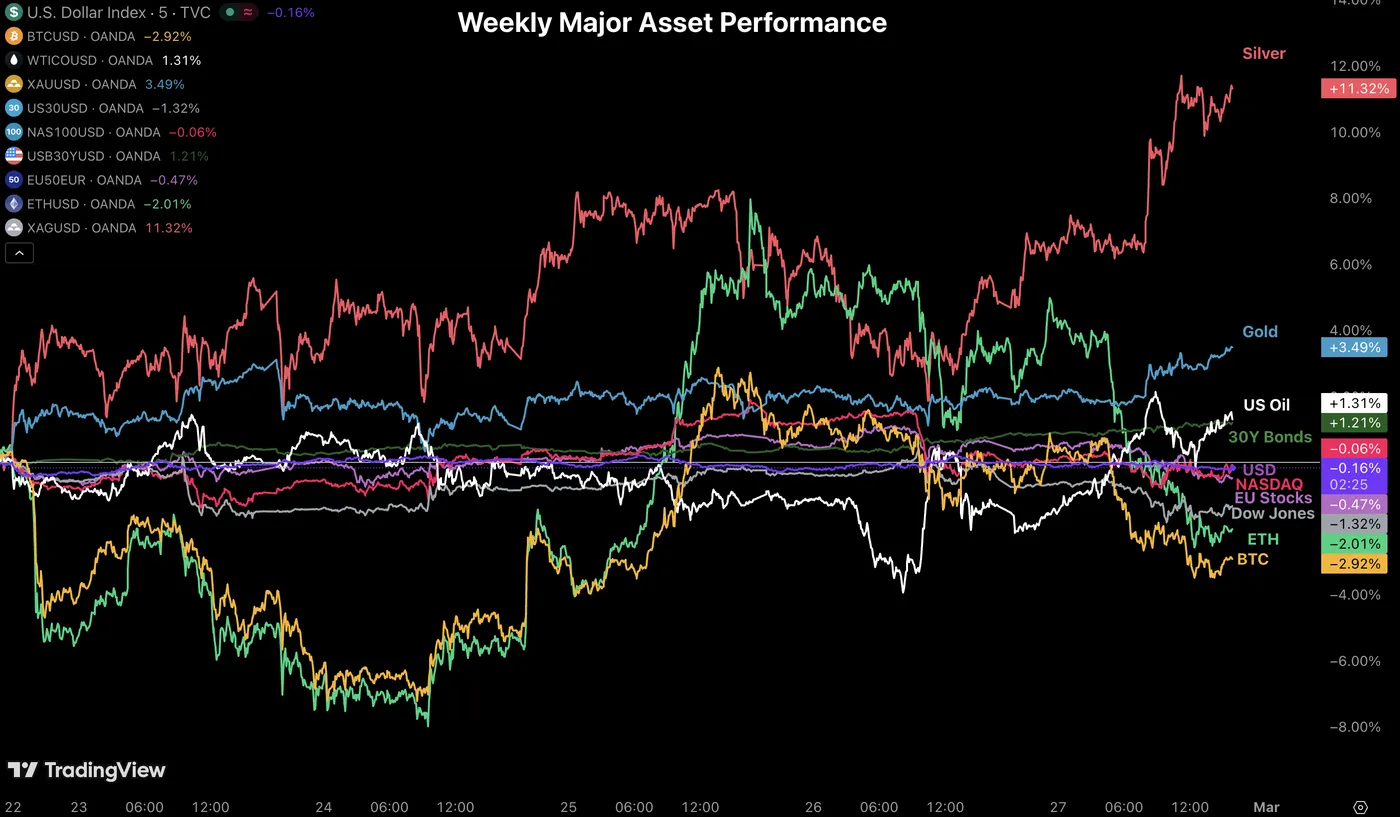

Weekly Performance across Asset Classes

Weekly Asset Performance – March 13, 2026 – Source: TradingView

Metals were the worst performers of this week’s action, and by far.

As long as Oil maintains a higher path, traders can expect similar flows ; That is, as long as Strait of Hormuz traffic doesn’t pick up.

The Week Ahead – Major Central Bank decisions

Asia Pacific Markets – Royal Bank of Australia and Bank of Japan’s Rate Decisions

APAC Traders will see the release of China’s Industrial Production Numbers and Retail Sales, two key releases to track the second largest economy and particularly if the effect of their local supportive policies have been working.

This should have a slight influence on AUD prices, but some other releases should mark the strongest 2026 performance even more.

Monday evening welcomes the Royal Bank of Australia’s rate decision, when a hike is about 80% priced.

This would bring the Australian rate to 4.35%, largely the highest for Major currencies (also erasing the 2025 very temporary rate cuts).

Aussie Dollar traders will also look for communication hints towards Wednesday’s Employment Data for Australia.

Kiwi GDP data for 2025 will also finally release, so that should also get the NZD in the spotlight.

Thursday will bring the final major Market catalyst, with the Bank of Japan’s Rate Decision. A hike is about 10% priced in for next week; A surprise hike would surely change a lot to the current Yen weakness, but to me, it wouldn’t be so uncalled for after recent JPY weakness.

If the BoJ doesn’t deliver, April will be the next rate hike target.

Europe and UK Markets – An intense Thursday Session

Europe will be mostly muted throughout next Week, but that wouldn’t include Thursday’s triple threat.

Currency traders will have a lot to work with between the UK Employment Data, but most importantly the Swiss National Bank, Bank of England and ECB Rate Decisions, all in the same day (and in that order).

North American Markets – Bank of Canada and FOMC

Canada will open the week with its Inflation data, but the largest day for North American Markets will surely be Wednesday.

The Bank of Canada and the FOMC will release their rate decisions, with no change expected.

Keep a very close eye and ear to what Powell has to say during his Press conference.

And don’t forget the US PPI release!

Keep a close eye on geopolitical developments, particularly those involving the US-Iran talks, as they are likely to continue influencing Commodity and broader Markets.

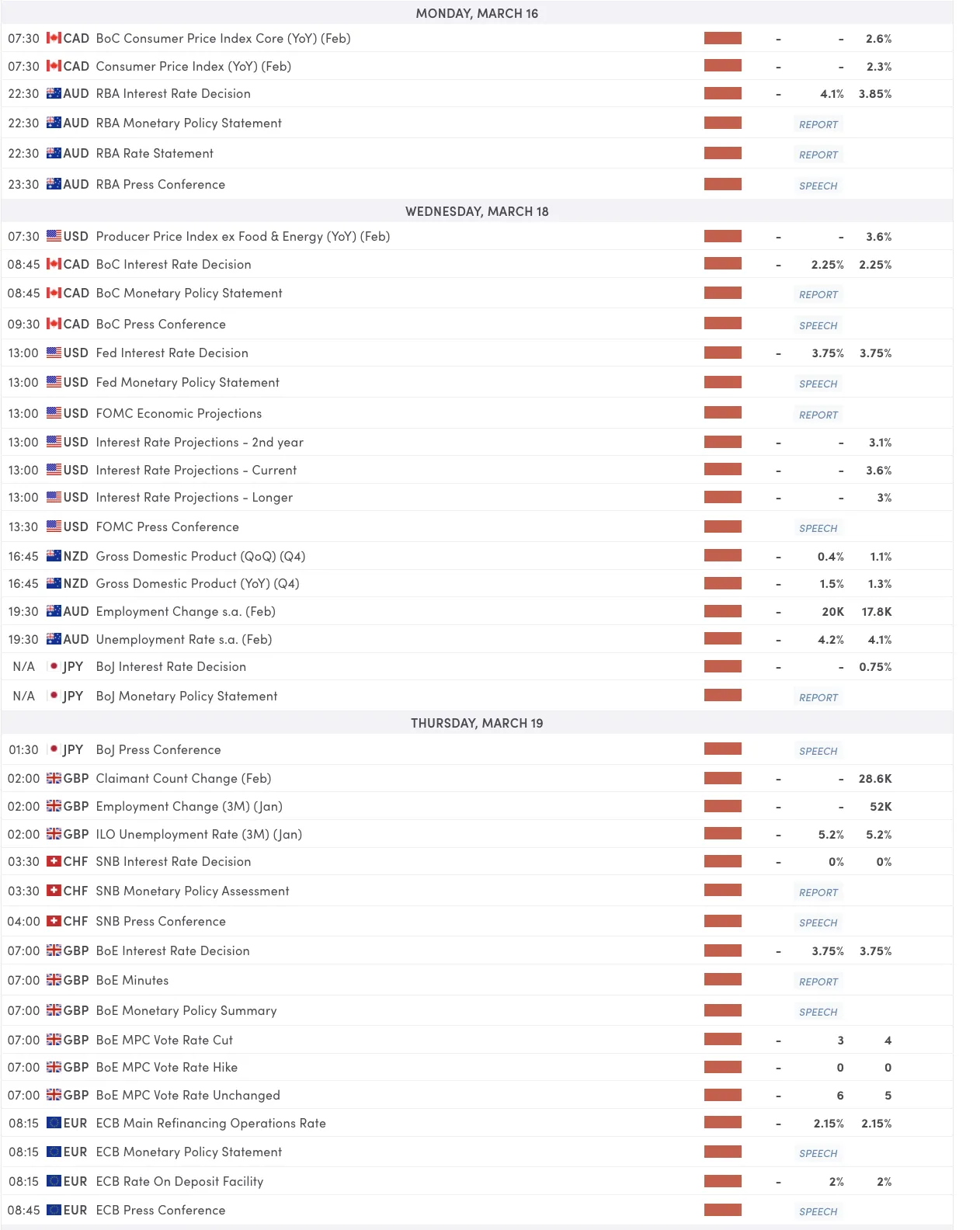

Next Week’s High Tier Economic Events

For all market-moving economic releases and events, see the MarketPulse Economic Calendar. (High-tier data only)

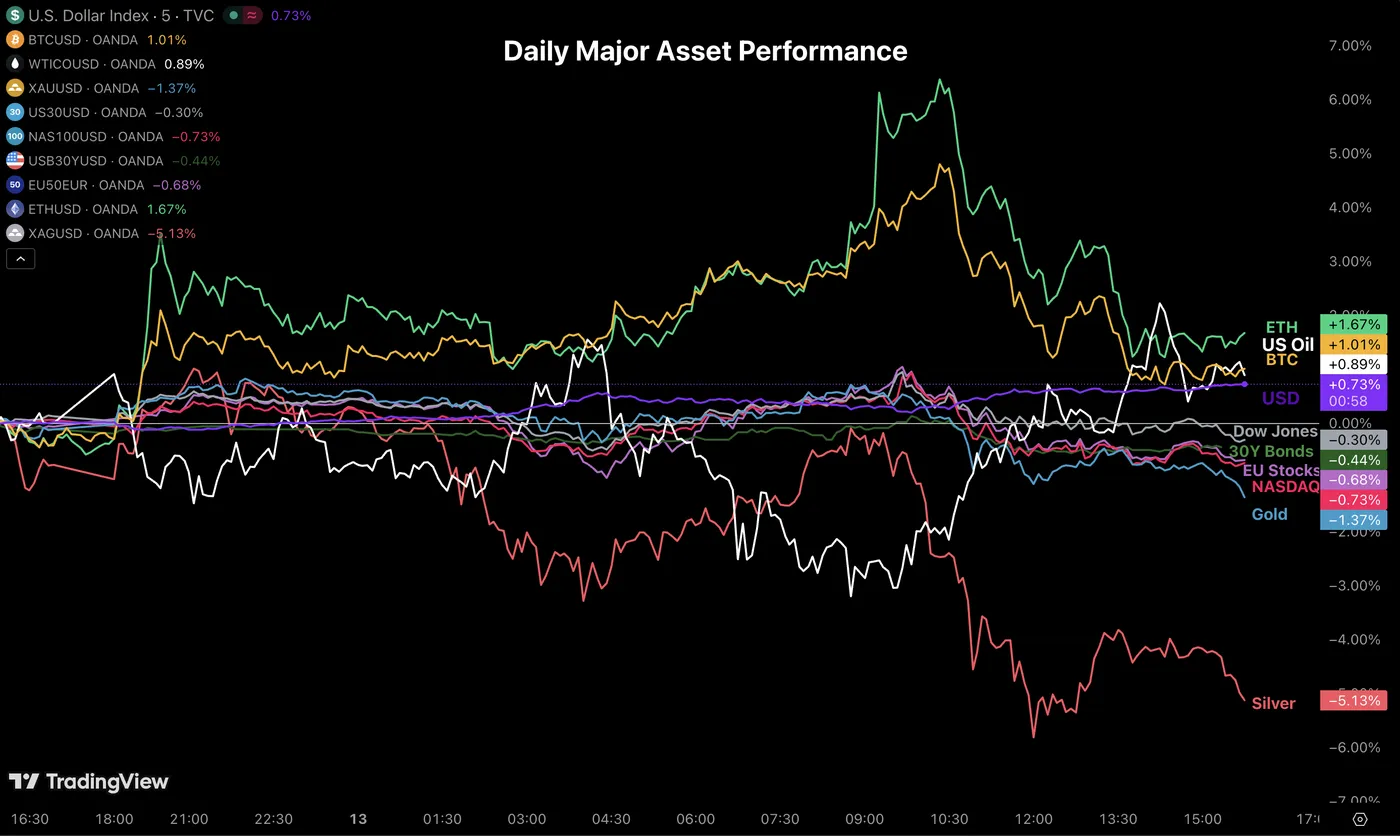

March 13th Market Wrap

Cross-Asset Daily Performance, March 13, 2026 – Source: TradingView

Today marked a decent rebound in Cryptocurrencies which really stand out from the recent Market trends.

Apart from that, Oil bounces higher again despite its pullback attempt, and the US Dollar found new highs against most of its FX peers, particularly Antipodeans and Europeans.

The Dollar Index is now trading above its November peak.

In terms of economic data, releases were soft. Core PCE came in softer than expected (2.8% vs 2.9% exp), University of Michigan barely moved (which is a good sign these days), and Canadian employment shrugged by 89.3K (!).

This could somewhat ease inflationary fears, but this would more likely have its effect on Monday (as weekend risk gets unrolled, if there’s valid reasons to do so!)

Safe Trades and enjoy your weekend!

{kind=link}