Canadian Highlights

- The ongoing U.S.-Iran conflict continues to dominate the headlines, pushing oil prices closer to recent highs.

- Monthly GDP and trade data shows Canada’s economy started the year on a steadier footing.

- The Bank of Canada maintained its dovish tone in its Summary of Deliberations, but acknowledged the two-sided risks on growth and inflation stemming from the war.

U.S. Highlights

- President Trump’s speech on Wednesday dashed hopes of a swift resolution to the conflict in Iran, sending crude oil prices higher.

- Retail sales rebounded in February after two months of stagnation. Meanwhile, JOLTS data indicated that the labor market remained in a low-hire, low-fire mode during February.

- Unless March payroll figures surprise meaningfully on the downside tomorrow, this week’s data supports the Federal Reserve’s current cautious, wait-and-see stance.

Canada – Barreling Ahead

WTI prices surged another 20% this week to over $110/bbl amid fading hopes for a quick resolution to the U.S.-Iran war. In his speech last night, President Trump’s hawkish remarks did little to ease markets, providing no timeline for a conflict resolution and warning of a possible escalation in coming weeks. Iran also doubled down on comments that it denies seeking a ceasefire, while insisting the Strait of Hormuz will remain closed and under its control. Despite the increase in oil prices, the Canadian dollar weakened by 0.7% to 71.9 cents U.S., as safe-haven flows and strong domestic data south of the border put a bid under the U.S. Dollar. Elsewhere, Canadian yields eased slightly this week as hawkish bets for Bank of Canada rate hikes later this year were pared back slightly.

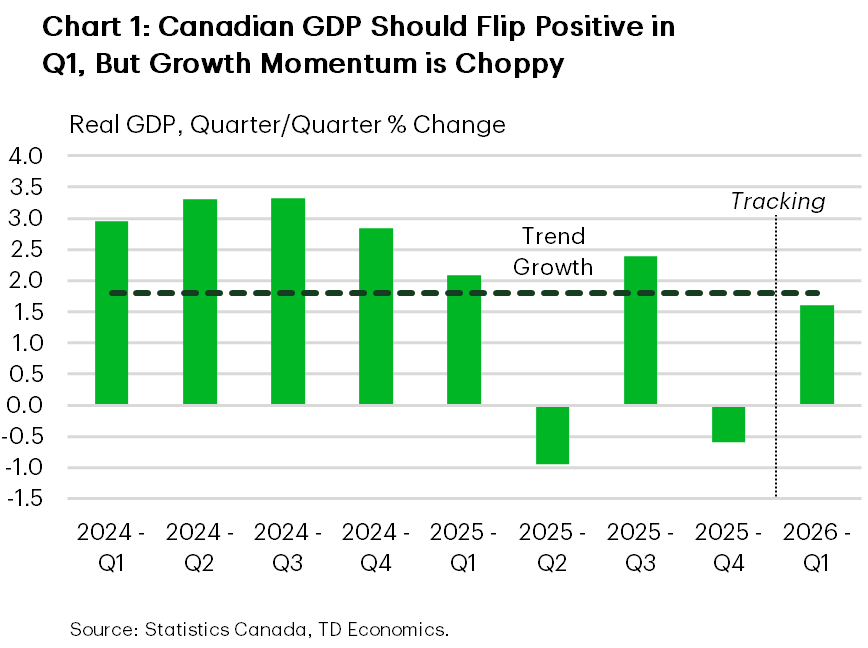

Canadian data this week gave a clearer picture of economic momentum prior to oil price shock. Industry-level GDP for the month of January showed Canada’s economy started the year on a firmer footing than many feared amid lacklustre Q4-2025 results. The reading was still on the softer side, growing by a modest 0.1% month-on-month (m/m), but it outpaced both Statistics Canada and market expectations for no growth. What’s more, early signs are pointing to an acceleration of 0.2% m/m real GDP growth in February, putting quarterly growth on track achieve trend-like results (Chart 1). Though positive on the margin, these readings may hold slightly less weight coming before the oil price shock impacted the economy.

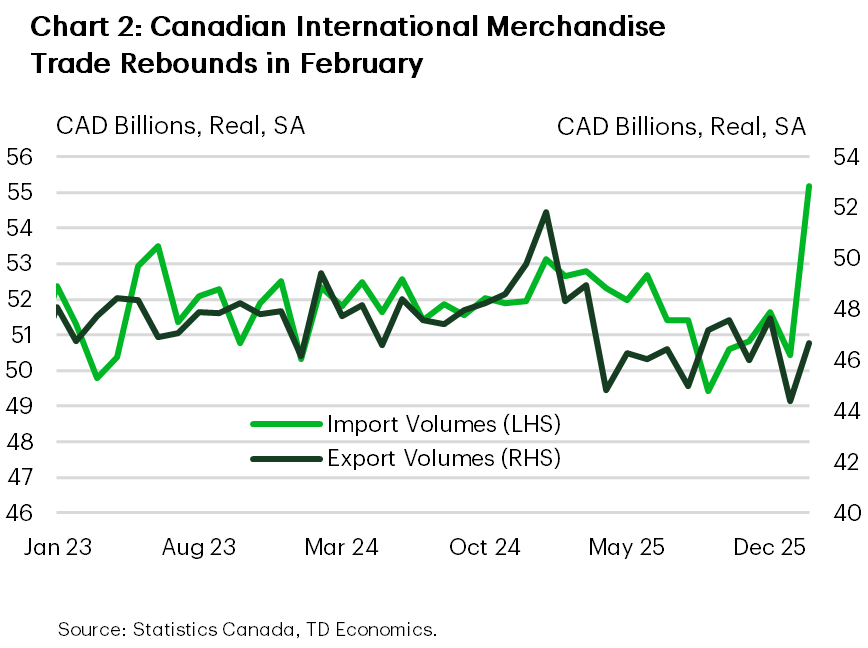

February’s international merchandise trade data also gave us another look at Q1 growth conditions. It was a sturdy month, as both exports and imports sharply reversed course from last month’s sagging activity (Chart 2). Gains on both sides of the ledger were broad-based as most subsectors booked a gain, though a bounce-back in auto-sector activity did a lot of the heavy lifting. The recent meteoric rise in oil prices will start to show up in the March data, boosting nominal trade momentum into the second quarter, which should help narrow Canada’s trade deficit. Elsewhere in trade, Canadian representatives are slowly re-engaging U.S. counterparts after a quiet few months, with hopes of smooth negotiations ahead of the July 1st CUSMA review.

The ongoing energy price shock and trade risks are still clouding the near-term outlook. In their Summary of Deliberations released this week, Bank of Canada Governing Council members recognized these challenges, but agreed to “look through” the spike in oil-driven inflation spike, opting instead of a more data-driven approach to policy setting. For now, the Bank maintains its dovish stance from the March policy meeting, given Canada’s economy remains sub par, with recent softness in core inflation and growth risks that tilt toward the downside. We expect the BoC to remain on the sidelines at their April 29th meeting, but will plan to monitor this shock carefully – weighing downside risks to growth against the upside inflationary impacts – and is prepared to act if circumstances change.

U.S. – Oil Prices: To the Moon and… (May Be) Back

Financial markets were volatile this week amid uncertainty on the duration of the Middle East conflict. The S&P 500 traded lower initially but rebounded mid-week on signs of de-escalation in the U.S.–Iran conflict. Treasury yields and crude prices also eased on the news, though the reprieve was brief. Like Artemis II, Trump’s speech on Wednesday night sent oil prices to the moon again on Thursday morning. While Trump reaffirmed a 2–3 week timeline for ending U.S. military involvement, he dashed hopes for a peace deal, promising to hit Iran “extremely hard”, and said that re-opening the Strait of Hormuz was not a U.S. goal.

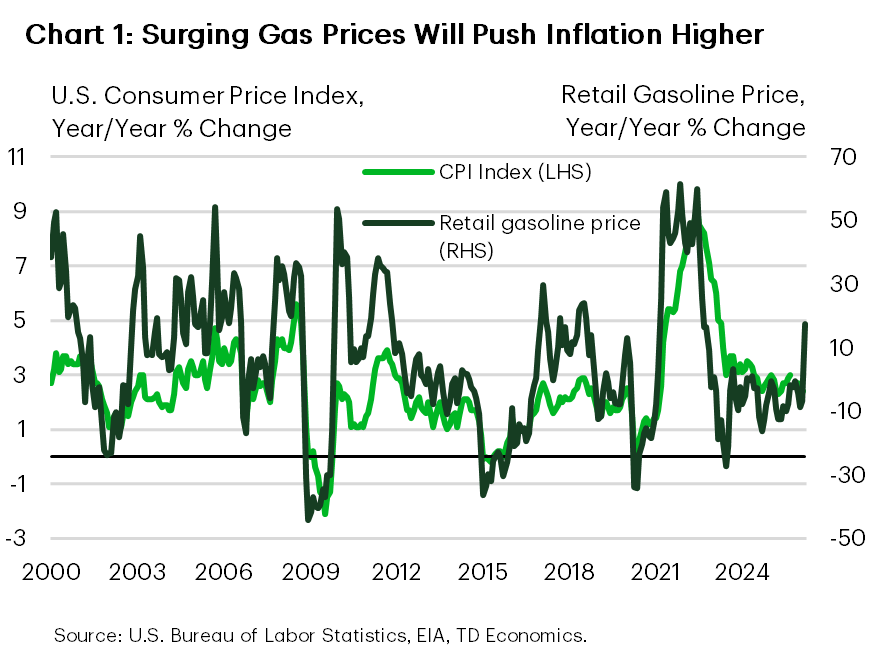

Even if the U.S. reduces its military attacks soon, oil prices could stay high: ramping up production and repairing infrastructure takes time, and supply risks persist if the Strait of Hormuz remains closed or below capacity. Inflationary risks are tilted upward even as our latest report notes the latest oil shock is unlike the one in 2022 in some ways. This shock is more concentrated in oil, with natural gas and agricultural commodity prices contained.

The economic backdrop is also different. Supply chains weren’t strained before the latest price shock, the labor market has cooled, and the economy isn’t firing on all cylinders. Still, with gas prices rising to $4/gallon this week, and signs that the conflict is adding pressure to other commodities, higher inflation is in the cards (Chart 1). This week’s data showed households’ inflation expectations jumped in March.

This is the fourth price shock to hit households in five years, arriving amid a slowing labor market. JOLTS data showed hiring declined in February, while job openings and layoffs were steady but low, suggesting the labor market remains in a low-hire, low-fire mode. Markets expect payrolls to rise by 65k in March, similar to the ADP print, and a partial rebound after an unexpected loss of 92k jobs in February. While not yet signaling a sharp deterioration, a cooling labor market leaves households more exposed to negative shocks.

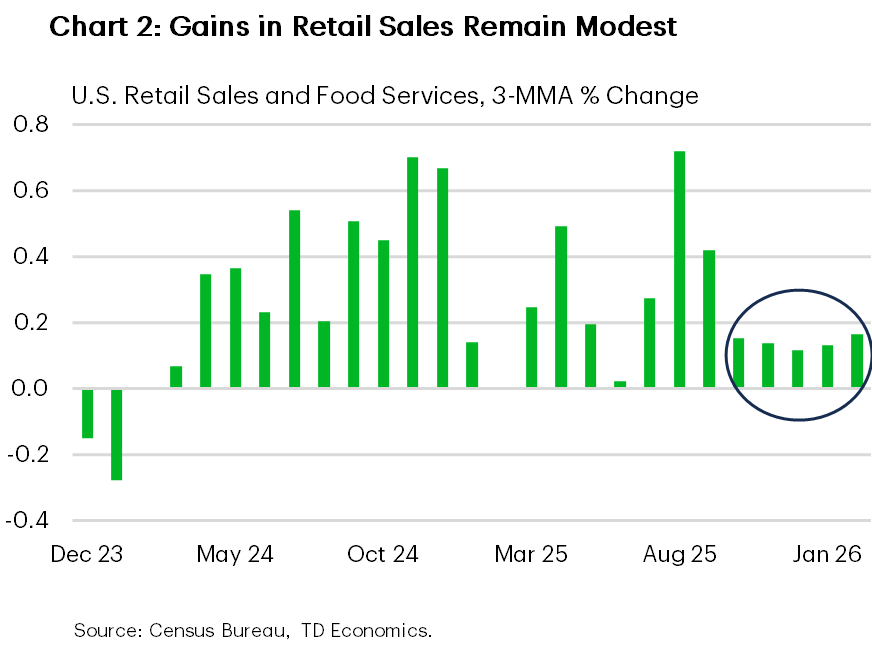

Consumer spending has stayed relatively resilient, but households are inflation-weary and showed caution even before the latest surge at the pump. Retail sales rose 0.6% m/m in February after two months of stagnation (Chart 2). Adjusted for inflation, sales volumes are up only 1% from a year ago. Larger tax refunds may help mitigate higher gas prices, but slower hiring and equities selloff could still weigh on consumption.

With stagflation fears surfacing, the Fed faces a tough balancing act. So far, it seems content to stay on hold. Earlier this week, Fed Chair Powell said oil shocks are typically short-lived and the Fed can remain patient; however, he noted the Fed would act if inflation expectations shift. NY Fed President Williams said, “the current stance of monetary policy is well positioned to balance risks to our maximum employment and price stability goals.” However, if you chase two rabbits, you likely won’t catch either. Let’s hope the Fed doesn’t find itself in that spot.

{kind=link}