- As widely expected, the RBNZ retained the OCR at 2.25%. There was no vote, with the decision reached by consensus.

- The commentary was hawkish as concerns of rising second-round inflation pressures were quite prominent.

- The MPC debated the options of an earlier vs later beginning to interest rate normalisation. Interest rate cuts were not discussed.

- An earlier start was described as May or July. A hike was discussed as an option today, but the Governor said that the MPC was not close to hiking at this meeting.

- The RBNZ’s short-term inflation forecast is now 4.2%y/y in June 2026 – higher than before, but close to our 4.1% forecast.

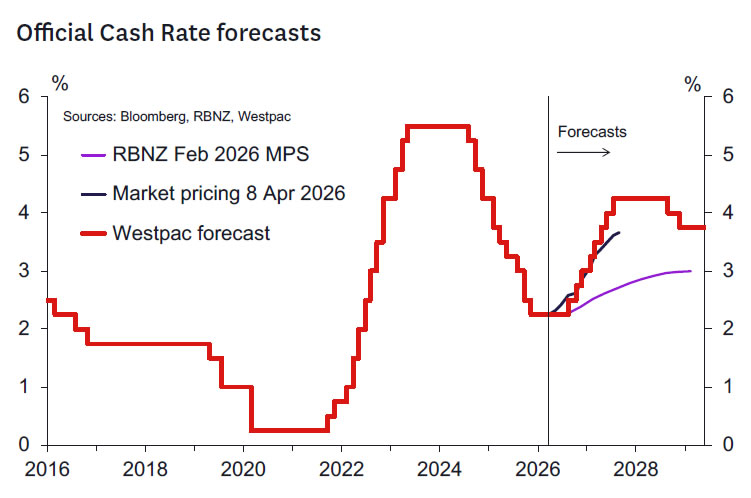

- We have pulled forward our forecast for the first OCR hike from the RBNZ to September (previously December).

- The balance of risks is towards an earlier start to hikes than September, should evidence of second-round inflation impacts accumulate.

OCR retained at 2.25% but coupled with a hawkish outlook.

The RBNZ kept the OCR unchanged at 2.25% as expected. There was no vote, with the decision reached by consensus. However, the Bank’s commentary adopted a more hawkish tone than expected. There was no discussion of needing to cut the OCR despite acknowledging that, at least in the short term, there would be greater excess capacity than previously thought. Rather, the debate was between:

- a “a pre-emptive response to medium-term inflation pressures could guard against the risk of inflation expectations becoming unanchored”; or

- a gradual increase in the OCR towards “more neutral levels” to reduce the risk of “reacting to higher nearterm inflation and accentuating weakness in the real economy and labour market”.

In the press conference the Governor noted that the MPC discussed the possibility of raising the OCR at this meeting, but there had been “no strong advocate” for doing so.

We interpret the more gradual path as being something akin to the late 2026 lift-off date that we have been forecasting, and that the RBNZ largely had in mind at the February meeting. A pre-emptive response likely implies something faster that begins by September but could come sooner than that, should evidence of secondround inflation impacts begin to accumulate. Indeed, the Governor indicated that the pre-emptive approach could have been a tightening in May or July. More dovish members were uncomfortable with the risks of that.

Key evidence that the RBNZ seeks seems to be in the form of anecdotal evidence on pricing and wage setting behaviour combined with higher frequency evidence on price setting, costs and inflation expectations coming from monthly surveys. We think it likely that at least some evidence along these lines will accumulate given the broad-based cost shock that the economy is facing. As a result, an earlier than December beginning to the tightening cycle looks much more likely now.

Hence, we are bringing forward our existing 25bp per meeting tightening profile to begin in September. The OCR will thus end 2026 at 3% and reach the previously expected 4.25% peak earlier, in September 2027. Easing is forecast to begin a year later in September 2028 with the neutral OCR reestablished in December 2028.

An earlier start than September should not be ruled out. And given it’s likely easier to explain the tightening profile in a Monetary Policy Statement meeting then the bias is likely for an earlier move to come in May versus July. The key question is: will sufficient evidence of second-round inflation impacts have accumulated by then? We think that’s still an open question at this point.

Key quotes from the press release and Record of Meeting were:

- “The Monetary Policy Committee is focused on ensuring that inflation returns to the 2-percent target midpoint over the medium term. This requires core inflation and wage growth to remain contained and medium- and long-term inflation expectations to remain around 2 percent. If these conditions are not met, decisive and timely increases in the OCR would be required.”

- “The outlook for medium-term inflation pressures depends on the size and persistence of the inflationary impulse stemming from higher oil prices and the extent to which it is offset by weaker demand in the economy.”

- “If the increase in near-term inflation is largely temporary, the Committee envisages gradually moving the OCR to more neutral levels as activity recovers and near-term inflationary pressures dissipate. However, any signs of significant secondround inflationary effects or increases in medium-term inflation expectations would require decisive and timely increases in the OCR to re-anchor inflation expectations.”

- “On the timing of any increase in the OCR, members discussed that a pre-emptive response to mediumterm inflation pressures could guard against the risk of inflation expectations becoming unanchored and reduce the extent of second round price increases.”

- “Conversely, the Committee noted the risk of reacting to higher near-term inflation and accentuating weakness in the real economy and labour market. Members noted that this could cause unnecessary volatility in output and employment if the conflict was resolved in the near term or if the economic outlook weakens by more than currently expected.”

The RBNZ’s initial thoughts on the near-term outlook.

The RBNZ provided updated inflation forecasts for the next two quarters. This is a change from their usual practice of not releasing updates to their forecasts at interim reviews and reflects that recent geopolitical developments have in the RBNZ’s words “materially altered the outlook and the balance of risks for inflation and economic growth”.

The RBNZ now expects inflation of 3% in the March quarter (previously 2.8%), rising to 4.2% in the June quarter (previously 2.7%). Those updated figures are close to our own forecasts. The RBNZ did not provide forecasts further ahead.

The RBNZ has noted that higher energy costs will push up other prices in the economy. However, longer term impacts on wage and price setting (aka. ‘second round impacts’) are expected to be constrained by weak demand at this stage. This is a key area of uncertainty and one where the RBNZ will be watching closely for signs that longer-term inflation pressures are increasing. Indeed, the RBNZ went on to note that “any signs of significant second-round inflationary effects or increases in medium-term inflation expectations would require decisive and timely increases in the OCR to re-anchor inflation expectations. The Committee is vigilant to these risks.”

While the RBNZ did not provide forecasts for other variables, they noted that the conflict and related increases in both operating costs and economic uncertainty will result in weaker activity in the near term. That’s very much in line with our own thoughts.

Things to watch ahead of the next meeting.

The RBNZ’s next policy review is on 27 May, when it will also publish a full Monetary Policy Statement (MPS) with refreshed forecasts (and probably some alternative scenarios too considering the current level of uncertainty). How the RBNZ’s stance evolves between now and then will depend on the path the Middle East conflict takes; what early indicators and anecdote suggest about the impact of the conflict on activity and inflation, both in New Zealand and abroad; and any developments in financial markets as a result of the conflict or other vulnerabilities triggered by the conflict.

As far as domestic economic indicators are concerned, we think the following are key ones to watch.

- Q1 CPI (21 April) and April Selected Prices (15 May): These pricing indicators will reveal the initial firstround direct and indirect impacts of the recent surge in fuel prices. They will provide some insight as to how high headline inflation might peak, but not about how long it will remain at elevated levels.

- Q1 QSBO (21 April) and April/May ANZ Business Outlook (30 April/27 May): Unfortunately, the data-rich QSBO survey was initially in the field very early in the conflict (it is unclear whether a breakdown of early and late responses will be released). Therefore, the ANZ surveys may provide a more up-to-date account of how businesses are responding to the conflict.

- March/April PMI and PSI surveys (mid-April/mid- May): These may provide some early insight regarding the likelihood of a contraction in GDP in Q2.

- Q1 labour market surveys (6 May): Employment and hours worked data from the HLFS and QES surveys will cast light on what momentum the economy had going into the conflict, while the LCI will cast light on underlying inflation pressures.

- Budget 2026 (28 May): While the formal unveiling of the Budget comes the day after the release of the MPS, ahead of the Budget the RBNZ’s MPC will receive a high-level briefing from the Treasury on what to expect at the macro level. Pre-Budget speeches and policy announcements may reveal more in the public sphere.

In addition to the above, we will be monitoring a range of other high-frequency indicators, such as monthly data on filled jobs, consumer spending, building consents, housing market activity and prices, job ads and consumer confidence. We will also be paying close attention to developments in prices for New Zealand’s key export commodities. The RBNZ looks to also be focused on anecdotal evidence of business pricing and wage setting behaviour – although that will be harder to track.

{kind=link}