- US and Iran talks make progress but key obstacles remain.

- Hopes rise of an end to the Strait of Hormuz blockade.

- But oil inventories are depleting fast; how long before they run out?

- Is the worst of the energy crisis yet to come?

Risk of complacency

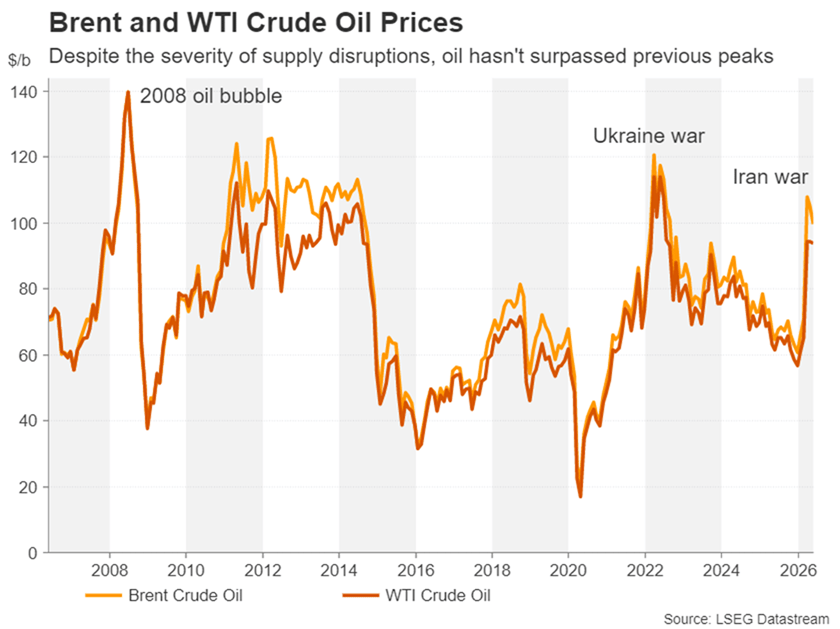

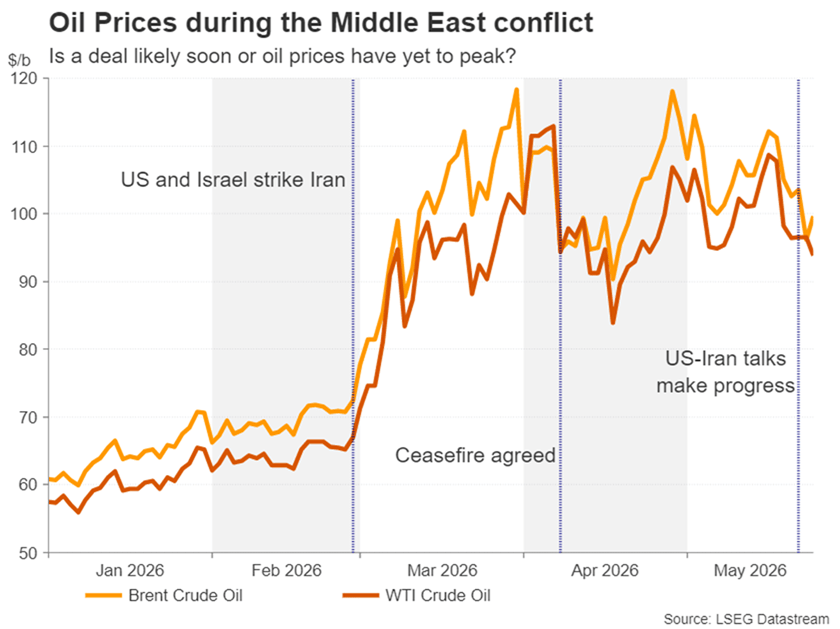

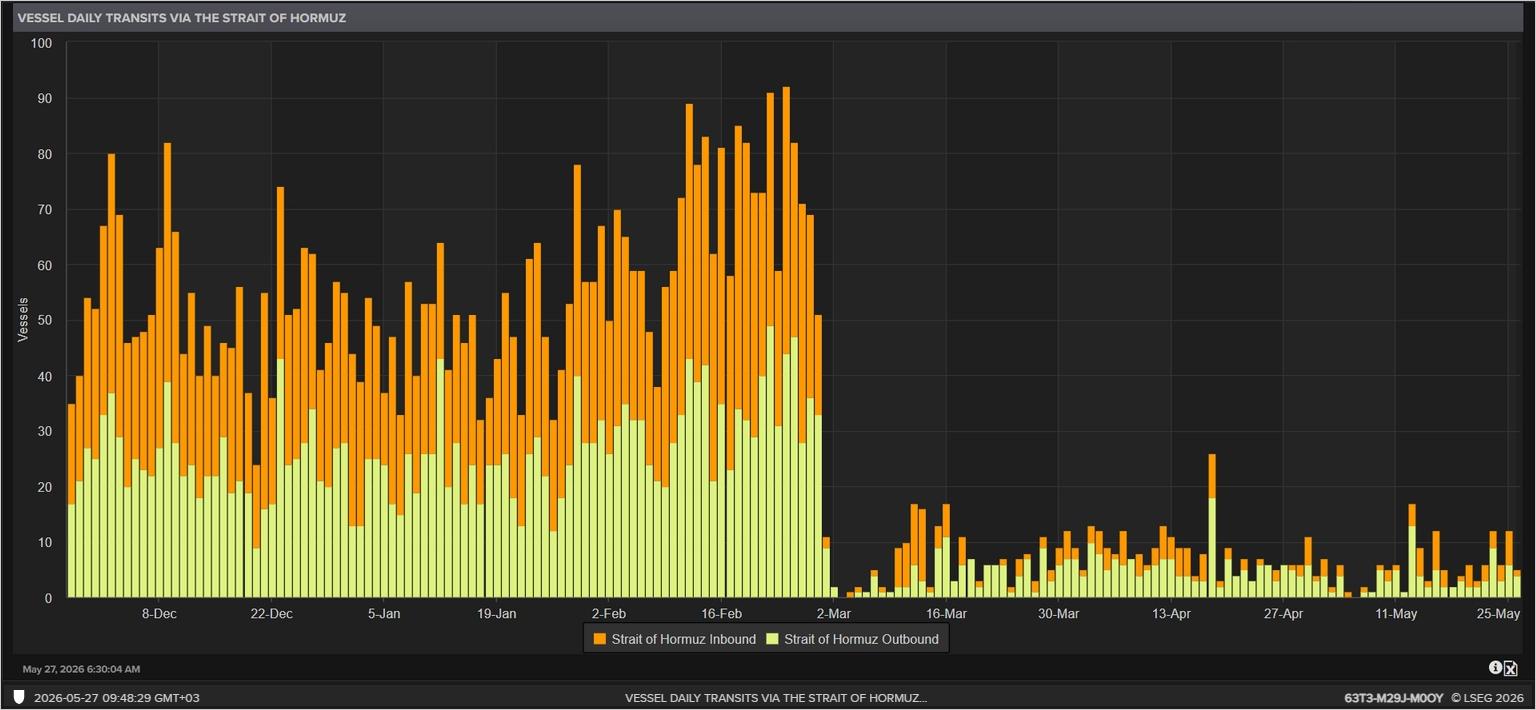

It’s been almost two months since the United States and Iran agreed to a ceasefire, bringing a temporary pause to the intense missile and drone strikes that crippled the region’s energy infrastructure. Yet, the cessation of hostilities has not brought about a reopening of the Strait of Hormuz – a vital passageway for global energy shipments – that handles about 20% of the world’s oil and gas supplies. While some traffic has resumed, daily volumes are a fraction of pre-war levels.

The severity of such a critical chokepoint remaining shut for a prolonged period should not be underestimated. But there’s a real danger that investors have been complacent about the risks. From a historic measure, the key crude oil benchmarks – Brent and WTI futures – peaked below the previous shocks in 2008 and 2022. This, despite the current crisis in the Middle East posing a bigger threat to longer-term supplies than either the supply-demand imbalance of 2008 or the sanctions imposed on Russia for its invasion of Ukraine in 2022.

A US-Iran deal may not be easy

The complacency can likely be explained by optimism that the war will not last long. Investors believe President Trump will not want the war to drag on for too long, as his popularity has plummeted in domestic polls, just months before November’s mid-term elections. Many are already speculating that the current ceasefire was initiated because Trump is seeking an exit from the war after failing to achieve a quick win by toppling the Iranian regime and imposing a one-sided deal on Tehran.

But the Iranians are remaining defiant and taking a tough stance in the negotiations by defending their right to a ‘civilian’ nuclear programme. The Americans, however, are adamant that Iran must not be able to develop nuclear weapons and are demanding that Iran surrender its existing stockpile of enriched uranium.

As things stand, the best that can be hoped for is a framework agreement for a permanent solution that would pave the way for the reopening of Hormuz. Nevertheless, after weeks of talks, the negotiations finally seem to be going somewhere, with reports suggesting that a deal is 95% complete.

Oil’s rollercoaster ride

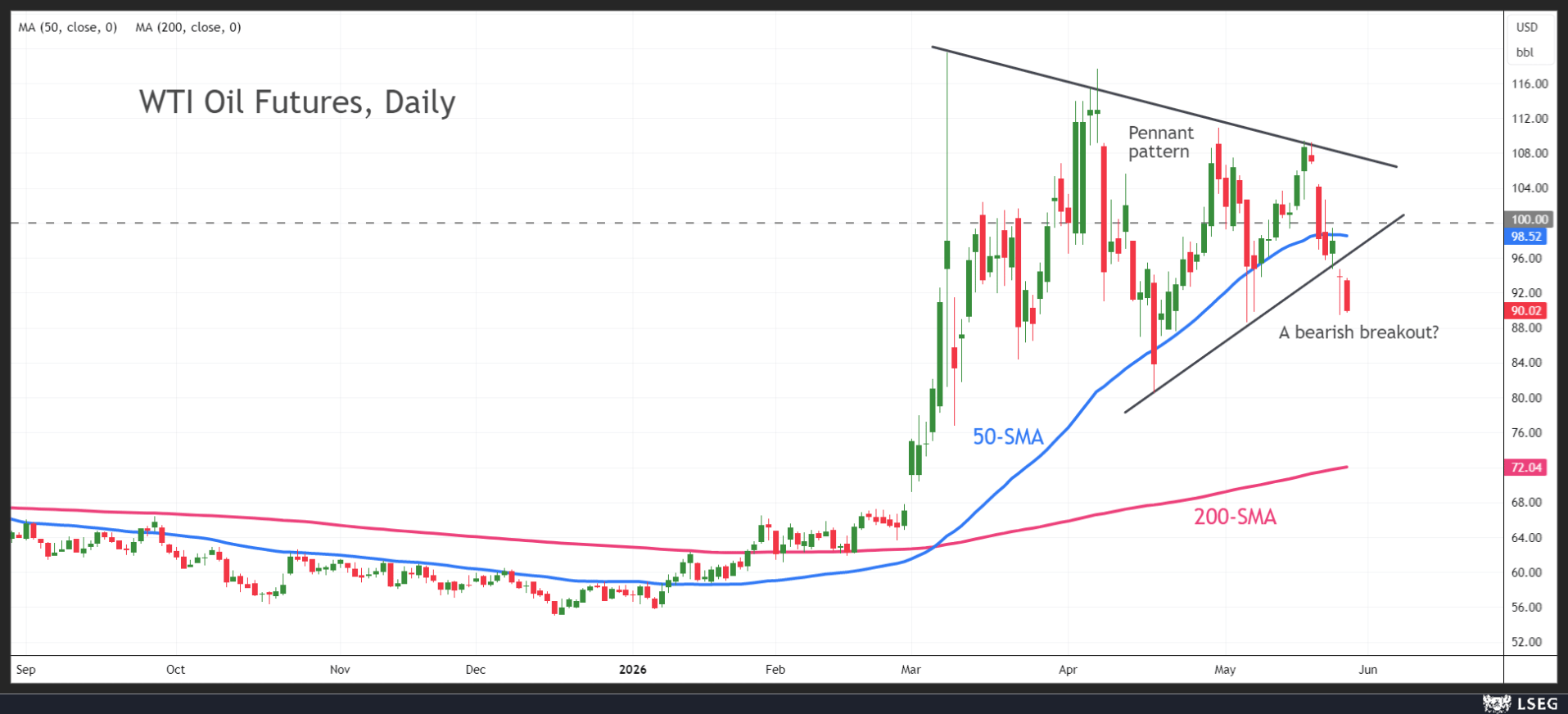

In many ways, oil’s price action since March demonstrates the frequently shifting sentiment on the expected duration of the conflict. The simultaneous formation of lower highs and higher lows that typically constitute a pennant pattern reflects the mood swings from hope to fear, with the pennant’s very wide angle indicative of the heightened volatility. But essentially, oil has been in a consolidation phase that may now be coming to an end.

The guarded optimism that kept oil from surpassing the March 9 peak of just below $120 a barrel but still very elevated near $100 barrel, has given way to the bears. News over the weekend that the US and Iran standoff could soon be over has led to a downside breakout below the pennant.

Is Oil turning bearish?

At this point, the risk of this being a false breakout is quite high, as a lot could still go wrong in the negotiations and there’s already been one military flare-up this week. Whilst there are a number of sticking points that must be resolved, the two most critical ones are about Iran’s nuclear disarmament and control of the Strait of Hormuz.

The fact that Iran appears to have agreed in principle to give up its highly enriched uranium in return for sanctions relief is encouraging. It’s also positive (for the global economy, not so much for the oil rally) that both sides are prioritizing the reopening of Hormuz.

Trump wants a deal

With regional mediators and powers stepping up diplomatic efforts, and President Trump signalling his willingness to allow the negotiators some time to work out the details, there is a good reason to be hopeful. However, the devil is in the details and so an agreement could take far longer than anticipated, not to mention the risk of the talks breaking down, particularly over the thorny issue of Tehran handing over its enriched uranium.

So where does all this leave oil supplies? Even in the best-case scenario that the US and Iran end their respective blockades of the Strait of Hormuz, it could be some time before any deal goes into effect and after that for energy flows to fully normalize. Hence, there’s a danger that it may be too late for the energy market to avoid a crunch point.

Are energy shortages looming?

One of the reasons why oil prices didn’t skyrocket even higher during this crisis is that most countries had significant inventories of crude oil and natural gas to fall back on. But with only a handful of oil and LNG tankers being allowed to pass through the Strait, some countries could begin to run out of stockpiles within weeks.

Many governments have sounded the alarm about impending energy shortages, taking various contingency measures, but it’s unclear how well prepared the world is for a worsening energy crisis if the Hormuz issue isn’t resolved soon.

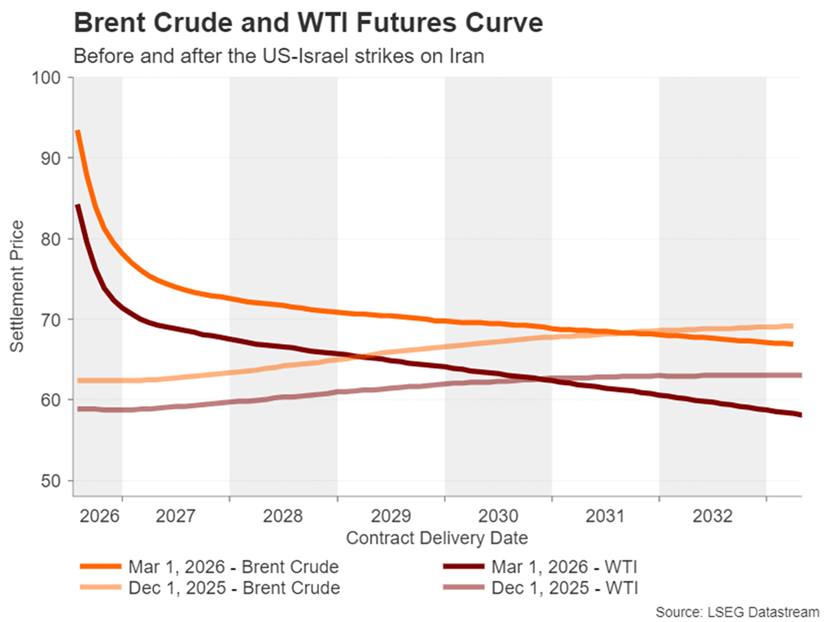

Yet, even with inventories depleting at a worrying speed, oil traders don’t seem too concerned. In fact, the oil futures curve has been in backwardation since March, signalling that oil prices will begin to fall substantially towards the end of the year.

Gulf Oil buyers look elsewhere

This may not be totally improbable. There are several factors why the energy crisis may not be as serious as many people fear. Despite all the headlines, the Strait of Hormuz isn’t completely closed off, and some oil and gas shipments have been able to get through. Moreover, both Iran and Saudi Arabia – the region’s largest producer – have alternative export routes to the Persian Gulf, so they are still able to export some oil.

Primarily, though, Iran’s largest customer – China – continues to buy Iranian oil, maintaining at least 50% of its imports from the country. In the meantime, India, which is another big energy importer, has been able to buy more oil from Russia, following the easing of some sanctions on Moscow to alleviate the oil supply problems.

Aside from Russia, other countries such as Brazil and Norway, not to mention the United States, have benefited too from the blockade of Hormuz. This diversification away from the Middle East, not just towards alternative suppliers but also towards alternative sources like renewable energy, could prevent the energy price shock from becoming too acute.

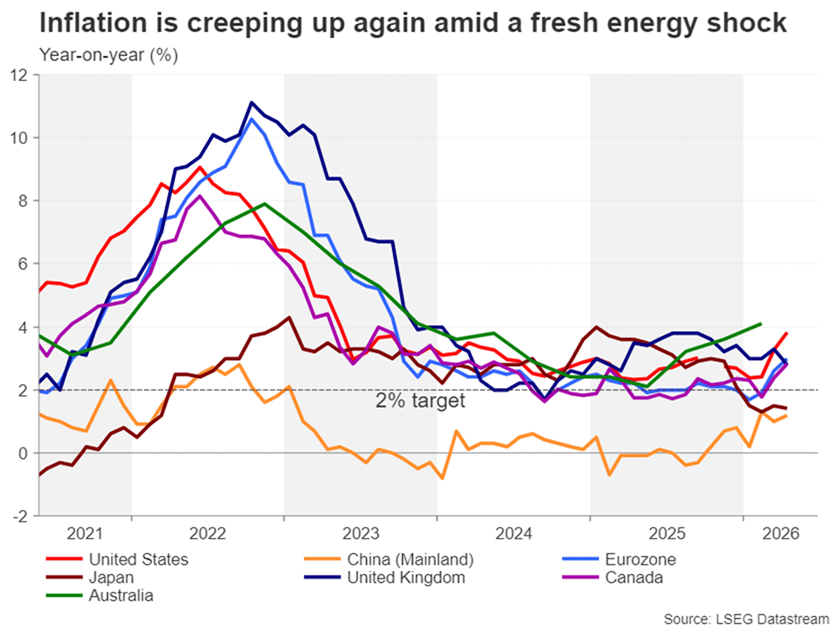

Inflation is on the way up

However, it’s not just the disruption to oil and gas exports that poses a major inflation headache. The region is a key hub for other vital exports around the world such as agricultural fertilizers, industrial chemicals, petrochemicals, and even aluminium. Hence, one way or another, the inflation effect will be felt.

More crucially, the backwardation in the oil futures curve could be explained by the anticipation that at some point, higher energy prices will cause demand destruction, rather than by the optimism that the US and Iran will be able to settle their differences quickly and reach a deal.

Demand destruction can occur not just from the higher prices themselves, but from higher interest rates too, as central banks would need to respond to rising inflation. According to the World Bank, a 10% jump in oil prices causes a 0.35% rise in global inflation within a year and a 0.55% increase within three years.

Rate hikes are coming

If those estimates are applied to the current crisis and taking the international benchmark of Brent crude as the oil price, then the 60% year-to-date gain could lead to a more than 2% increase in global inflation next year. With inflation in most countries already above central banks’ 2% target, such an acceleration is enough to warrant tighter monetary policy.

So far, only the US Federal Reserve appears to be looking through this latest inflation uptick. If there is a deal soon, it may just get away with keeping interest rates on hold. But a more likely outcome is that it will be months before oil prices retreat substantially below the $100 region and the Fed will have no choice but to follow its global peers in hiking rates.

The bigger question mark, though, may not be whether interest rates will go up or not, but by how much. Right now, there’s a greater risk investors have been too conservative with their rate hike expectations and once reality hits, they will overcompensate by pricing in more tightening than is needed. However, if the worst-case predictions do not materialize, a relief rally is almost certain to follow.

{kind=link}