- Recent developments mean that the RBNZ’s outlook for the OCR has likely moved back towards that forecast in the February MPS.

- We are similarly updating our forecasts to reflect the unexpectedly quick resolution of the Iran conflict and associated significant decline in the price of oil and refined fuels prices and related commodities.

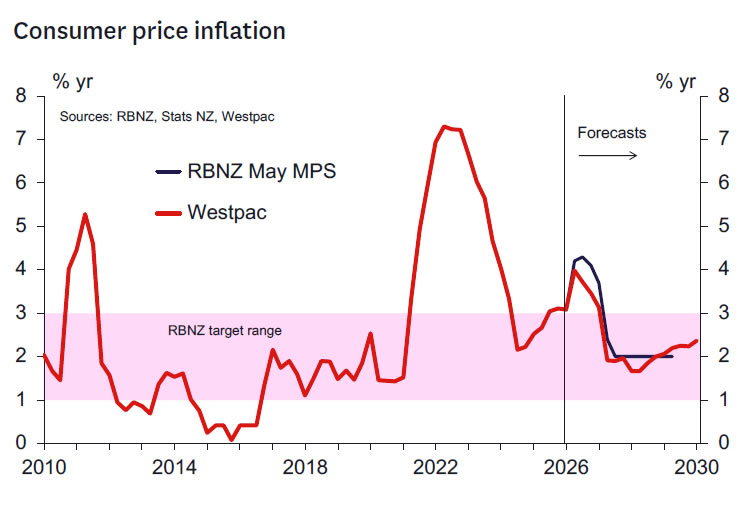

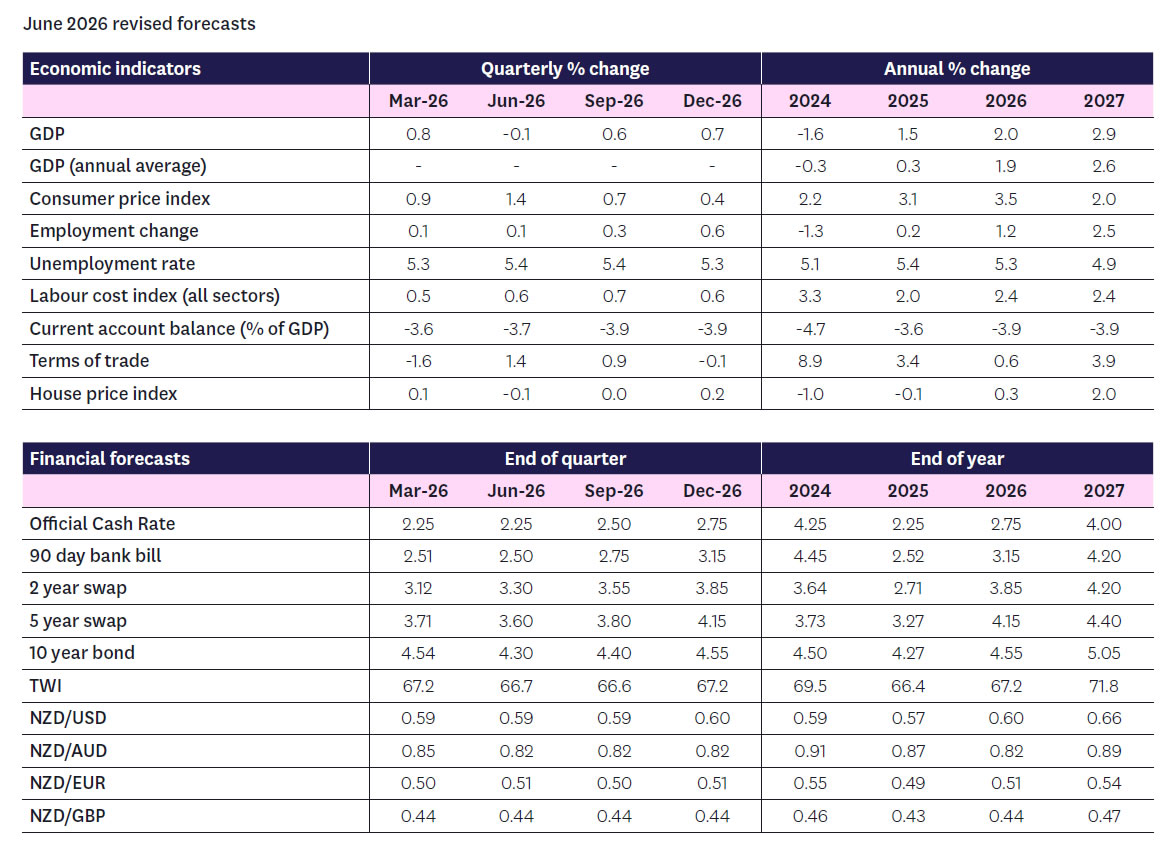

- We now see headline inflation peaking at 4.0% in the June quarter this year and ending 2026 at 3.5% – possibly lower if the most recent fall in oil prices is sustained.

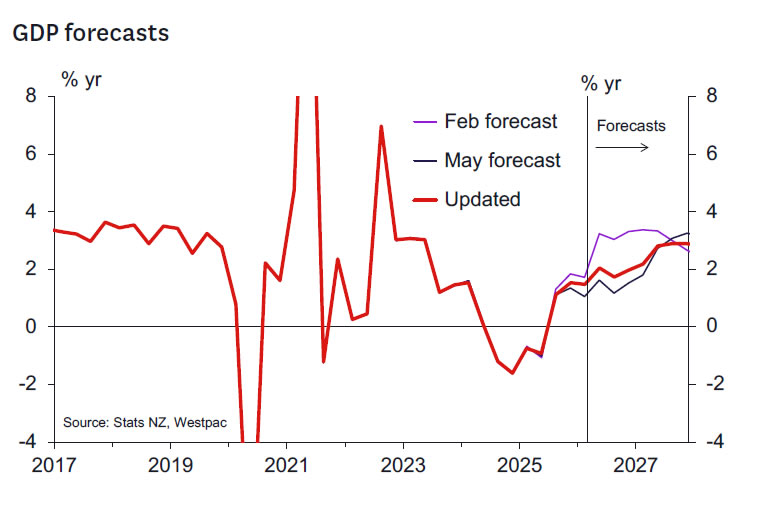

- We have marked up our 2026 GDP growth forecast to 2.0% from 1.5% previously, although this remains lower than our pre-war forecast.

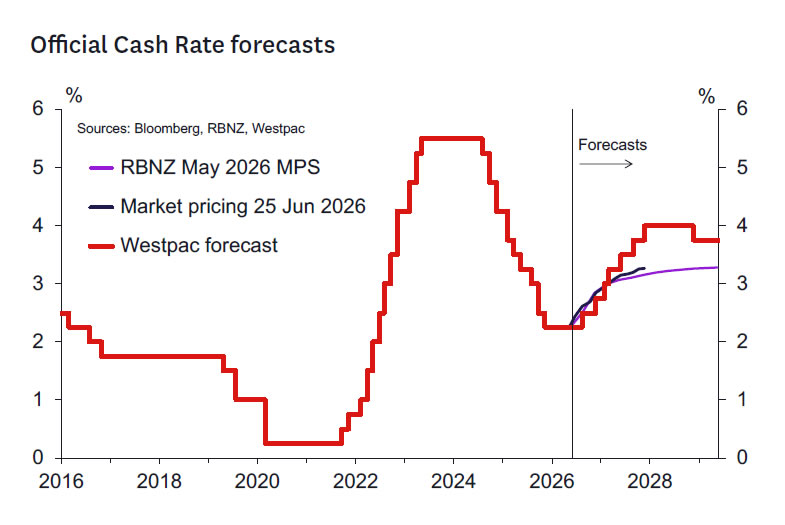

- We affirm our view that the OCR will be held at 2.25% at the upcoming 8 July meeting. Indeed, we expect this decision to be far less contentious than in May, and don’t rule out that this decision is made by consensus and so without a vote.

- We also affirm our view that the RBNZ will begin to tighten at the September MPS. However, beyond September, we now expect just one further tightening this year – rather than two – which will probably occur at the December MPS meeting.

- Relative to pre-conflict forecasts made by both Westpac and the RBNZ, this implies one extra OCR increase in 2026. This is justified by the more elevated path for inflation relative to that expected in early 2026.

- We have reduced the forecast peak in the OCR to 4% and thus retain the same pattern of OCR changes through 2027. A lower peak OCR is consistent with the smaller and shorter duration oil related supply shock now assumed.

- There are two-sided risks around this profile that depend on how quickly the economy recovers through the second half of 2026 and the pace at which underlying inflation pressures recede.

- Downside risks persist for the New Zealand dollar as interest rate differentials are likely to weigh on the exchange rate given much higher US and Australian policy rates. We will review our FX forecasts next month in the July Market Outlook produced jointly with our Australian colleagues.

A Revised Economic Outlook Is Warranted

A great deal has changed since early May when we last reviewed our forecasts for the global and domestic economies – more than the market appears to have appreciated considering the continued pricing of a RBNZ rate hike at next month’s policy review. The key issue has been the unexpectedly quick progress on reducing Persian Gulf tensions and the potential for a faster return of shipping flows in the Strait of Hormuz, with resultant improvements in trade flows of oil, petrochemical products and natural gas, as well as a range of other key products (such as fertiliser).

While it is premature to conclude that tensions in the region will be durably settled, there are sufficient signs that diplomatic efforts are well underway such that a decent period of ceasefire and more normal shipping flows is in prospect. Hence, it’s appropriate to incorporate this new information into our New Zealand macroeconomic view.

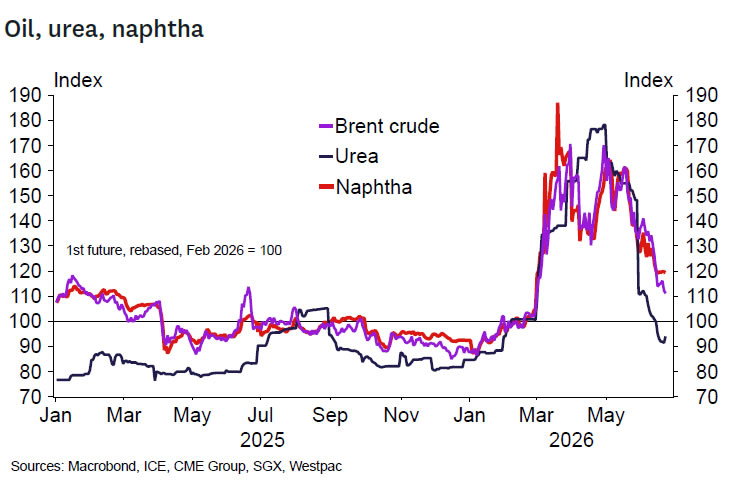

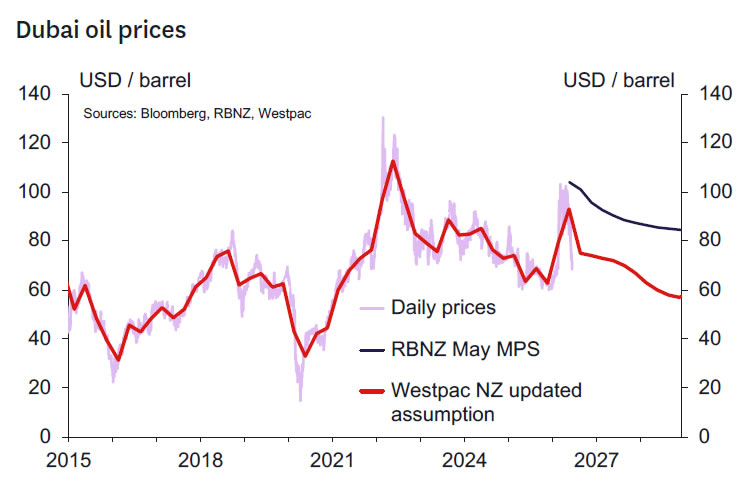

The key updates to our assumptions relate to the assumed level and future path for oil and refined fuels prices. These have converged much more rapidly than expected to levels we previously didn’t expect to see until mid-2027. Brent crude oil is currently trading around US $73/bbl, close to the levels we saw prior to the war. We expect that prices will ease further over 2027 to $69/bbl. Refined fuels prices have been easing more gradually, but have still fallen substantially from a peak of US $195 bbl in March to US $110 bbl at the time of writing (vs around US $92/bbl prior to the war). Refined fuel prices are expected to continue easing back over the coming months, falling to US $102 bbl by the end of this year and US $90 bbl by the end of 2027.

Importantly, oil prices are now much lower than the RBNZ assumed in the May forecasts.

We have also accounted for recent economic data on GDP, selected price indices, and other higher frequency data on output when reviewing our economic view. We have not reviewed our global economic forecasts, or the exchange rate forecasts (aside from updating the starting point for the exchange rate) as these will next be reviewed, in conjunction with our Australian colleagues when we prepare our July Market Outlook publication forecasts.

We also have not included the implications of the new fiscal position revealed in Budget 26. Having said that we think the implications are likely modest and will be fully incorporated into our forecasts when we prepare our next Economic Overview in late August.

GDP Growth – Recovery to Resume Sooner

We have upgraded our GDP forecasts for both the June quarter – the peak of the oil shock impact – and over the second half of this year. Much of this reflects a bringing-forward of the timing of the economy’s recovery as the oil shock fades, so we now expect a slightly slower rate of growth through 2027. GDP growth for 2026 is now forecast to be 2% and 2.9% in 2027.

A review of the most recent data suggests that the economy held its ground through the peak of the oil price shock in April and May, faring a bit better than we had assumed in our last forecast update. We now expect GDP to fall by just 0.1% for the June quarter, from our previous forecast of -0.3%.

We should note that both forecasts include an allowance for the seasonal distortions that remain an issue in the GDP data. Our new forecast implies an underlying growth pace of around +0.2%, with seasonal factors knocking 0.3% off the reported result.

With oil prices receding faster than we’d assumed, the economy is set to resume its pre-conflict recovery path sooner as well. We expect quarterly growth to pick up to 0.6% and 0.7% in the September and December quarters, from 0.4% and 0.6% previously. Altogether that would see the economy grow by 2.0% over the course of this year, compared to our previous forecast of 1.5%. That’s still some way below the 3.3% growth that we were expecting this year prior to the Iran conflict, which will still prove to be a significant setback to the momentum that was otherwise building in the economy.

Labour Market – Hiring to Resume

With a stronger GDP outlook for this year, we now expect a lower peak and a quicker turnaround in the unemployment rate over the next year. We still expect some softness in the jobs market in the near term – the uncertainty generated by the Iran conflict has likely led some businesses to hold off on hiring decisions. The high-frequency jobs data so far suggests that we’re on track for flat rather than falling employment over the June quarter. But that won’t be enough to absorb the growth in the working-age population, so we expect to see the unemployment rate tick up again to 5.4% after having eased to 5.3% in the March quarter.

Beyond that though, we see less risk of a further rise in unemployment over the coming quarters. Our forecast now peaks at 5.4% through the middle part of this year, easing to 5.3% by year-end and 4.9% by the end of 2027 (the latter forecast is unchanged).

Housing – Still Moving Sideways

We have revised up modestly our forecasts for house price growth in 2026. Recent house price data confirms a flat profile for house prices in recent months and a similarly flat path for the days to sell a property. Looking forward, we anticipate a mildly more positive tone to return to the market as consumer and business sentiment improves with falling energy prices. Previously we had thought we might see a relatively weak outcome for September quarter house prices, but now it seems more like a flat outcome is closer to the mark. Weaker expectations for RBNZ OCR hikes have translated through to lower mortgage rates in recent weeks which should also assist sentiment.

We now expect very modest house price growth of 0.6% in 2026 (previously we expected a modest 1% fall). We still expect prices to rise by 2% over 2027. We continue to expect house prices in the regions to outperform those in the major North Island urban centres as it will take some time for the services sector to pick up and the labour market to strengthen to the point where we see a decent fall in the unemployment rate (now forecast to begin late in 2026 and picking up pace through 2027).

Inflation – Lower Peak, Quicker Reduction

In response to the faster than expected fall in oil prices, we have pulled down our inflation forecasts. We now expect that annual inflation will peak at 4.0% in the June quarter (down from the peak of 4.5% we assumed in our May forecasts), slowing to 3.5% in the December quarter – possibly lower if oil prices remain as low as they are today. That would be well below the 4.1% rate the RBNZ assumed for year-end inflation in its recent May MPS projections.

The earlier than expected fall in global oil prices has already flowed through to lower prices at the pump for New Zealand consumers. The average price of 91 unleaded around the country has fallen to $3.02/ltr (down nearly $0.50/ltr from its peak in May), while diesel has fallen to $2.56 (down more than $1/ltr). Further price falls are likely given current spot energy prices. Those lower oil prices have directly shaved about 0.5ppts off our year-end inflation forecasts.

We have also dialled back assumed second round inflation effects reflecting the smaller and shorter duration cost shock. That’s taken about 0.2ppts off our inflation forecasts. We retain around 50% of the second-round effects included in previous CPI forecasts as although oil prices have fallen substantially, they are still well above the levels we saw prior to the conflict. We will review these estimates as we receive more definitive CPI data in coming quarters.

More generally, we think that subdued demand has constrained how far many businesses have been able to raise their prices despite increases in operating costs.

Looking to 2027, inflation is expected to drop back as the impact of the oil price shock dissipates. Indeed, given base effects associated with this year’s oil shock, headline inflation will briefly dip below 2% in 2027, before rising as the economy recovers.

Smoothing through the volatility associated with fuel prices, core inflation has lingered at firm levels over the past few years despite the softness in economic activity. The average of the RBNZ’s suite of core inflation measures sat at 2.3% in the March quarter. Inflation excluding food and fuel prices, is currently around 3% and it is expected to linger close to the top of the RBNZ target band for the remainder of this year, before easing over 2027.

Monetary Policy – Less Urgency Required

Our forecasts imply the RBNZ’s outlook for the OCR will likely move back towards the economic outlook envisioned back at the February MPS (when the Bank expected at most one 25bp hike this year). This would imply much less urgency to raise the OCR compared to the view in the May MPS (which had assumed two to three 25bps hikes this year).

The key question is: just how far will the RBNZ have moved? We think it reasonable that the RBNZ will likely have taken at least one 25bp hike out of its internal projections and will likely now be projecting one to two 25bp OCR hikes this year. Hence, we don’t think the RBNZ will have reverted all the way back to its pre-Iran war views – in part because the inflation outlook remains significantly elevated for a while yet relative to what the RBNZ expected back in February. But nevertheless, the significant shift in circumstances since May should imply a significant shift in the forward stance.

So, what does this imply for the upcoming 8 July meeting? We think that the sharp fall in energy prices and the resulting improvement in the inflation outlook will have undermined the case for pre-emptive action. The hawks on the MPC may well still see a strong case for OCR increases this year but will likely be significantly comforted by the big change in the immediate inflation outlook as it must imply lower risks of persistently high inflation. At the least, the argument for moving earlier will look a lot weaker than back in May when those views were ultimately outweighed by the dovish camp. There’s a significant chance that the hawkish bloc opts for no change in the OCR in July while remaining open for OCR hikes later in 2026.

The more dovish MPC members that wanted to see more evidence of enduring second-round inflation impacts in May will likely have hardened their views. Indeed, with the key June CPI, labour market and QSBO reports all due between the RBNZ’s July and September meetings, together with the next round of inflation expectations surveys, there seems little to be lost in waiting to see what these key reports reveal (and to see whether the current US-Iran negotiations progress to a durable final deal). We don’t think we have learned much about the extent of second-round inflation impacts since May aside from the fact that the short-term inflation outlook now looks far less threatening than then. And of course, there is more tangible evidence the economy stalled in the June quarter (the RBNZ’s June quarter Nowcast indicates flat Q2 growth). Looking ahead, as discussed previously, there are likely good reasons to expect a stronger H2 2026 growth performance than felt back in May, but this is likely to still need to be confirmed by data and still likely to be far weaker than hoped for in early 2026 when even then just one OCR hike for 2026 was said to be on the cards. We don’t think that any of the doves are likely to want to shift camp to the hawk’s side in the July meeting.

A key argument market participants seem to rely on is the sense that the RBNZ may have almost promised a July hike back in May. We don’t think this is accurate as the MPC will always fiercely note that any forward guidance on the OCR will be data dependent. We understand that mathematically, the RBNZ May forecast for an average OCR for the September 2026 quarter at 2.51% seems consistent with a July hike. But this will not have been a non-data dependent promise. In most cases, the RBNZ’s short term OCR forecasts provide broad guidance on the likely direction of the OCR rather than a definitive forecast and have historically proven to be a poor guide to the next policy decision. More importantly, the Governor’s words when describing the outlook are likely to be more prescient. The Governor noted that an increase in the OCR seemed likely “in coming meetings” – this is not a promise of an OCR increase in July. This is rather an expression of the intention to lift the OCR later in the year – and even that intention will (and should!) be data dependent.

Therefore, we affirm our view that the RBNZ will hold the OCR at 2.25% at the 8 July meeting. In fact, we expect this to be far less contentious than the May decision, and do not rule out the possibility that this decision is reached by consensus and so without a vote.

Looking beyond July, it remains reasonable to expect the RBNZ to tentatively begin lifting the OCR at the September MPS meeting and move again once more towards neutral settings before the end of the year – most probably at the December MPS meeting. But even these forecasts are not a slam dunk and have two-sided risks. Should the June quarter CPI provide benign in terms of core inflation measures then the RBNZ could leave the OCR unchanged until December. If the CPI runs hot, then we could still see the three 25bp rate hikes that we forecast before today.

Our central view implies one fewer hike this year than we had forecast most recently but one more than we had forecast prior to the conflict. This is justified by the more elevated path for inflation relative to that expected in early 2026. We have retained the same OCR changes that we had previously forecast to occur in 2027 and so the OCR is now forecast to peak 25bps lower at 4.0%. A lower peak OCR is consistent with the smaller and shorter duration oil-related supply shock now assumed. Our view on the neutral OCR remains at 3.75%.

In this update we have made no change to our FX forecasts. Downside risks persist for the New Zealand dollar as interest rate differentials are likely to weigh on the exchange rate given much higher US and Australian policy rates. We will review our FX forecasts next month in the July Market Outlook produced jointly with our Australian colleagues.

.){kind=link}