Here are the latest developments in global markets:

FOREX: The dollar was little changed versus a basket of currencies on Monday after previously recording a one-month low and coming under pressure versus the yen, with dollar/yen hitting a fresh 16-month low. The pair later recovered though to trade higher on the day.

STOCKS: US markets remained in a downward spiral on Friday, as concerns over a potential trade war continued to suppress risk appetite. The Nasdaq Composite was the biggest underperformer once more, plunging by 2.4%, while the S&P 500 and Dow Jones fell by 2.1% and 1.8% respectively. However, futures tracking the Dow, S&P and Nasdaq 100 are all currently well-into positive territory, signaling a higher open for these indices today. The shift in sentiment is likely owed to comments by Secretary Treasury Steven Mnuchin over the weekend that he is “cautiously hopeful” the US can reach an agreement with China soon and avoid implementing tariffs altogether. In Asia, Japan’s Nikkei 225 and Topix rose by 0.7% and 0.4% correspondingly, while in Hong Kong, the Hang Seng was higher as well but by less than 0.1%. In Europe, futures tracking most of the major indices were flashing green.

COMMODITIES: Oil prices were on the back foot on Monday, with WTI and Brent crude declining by a bit more than 0.4% and 0.3% respectively, both benchmarks giving back some of their notable gains from last week. The precious liquid was likely dragged lower by the broader risk aversion in markets. Oil seems to be caught at a crossroads at the moment, with diminished risk appetite weighing on the commodity, but speculation that fresh sanctions could be imposed on Iran soon supporting prices. In precious metals, gold fell 0.2% on Monday, last seen near the $1345 per ounce level, after having touched the $1350 resistance zone earlier during the Asian session. The yellow metal was one of the biggest outperformers last week, as the mounting worries over global trade finally started to support the safe-haven perceived asset.

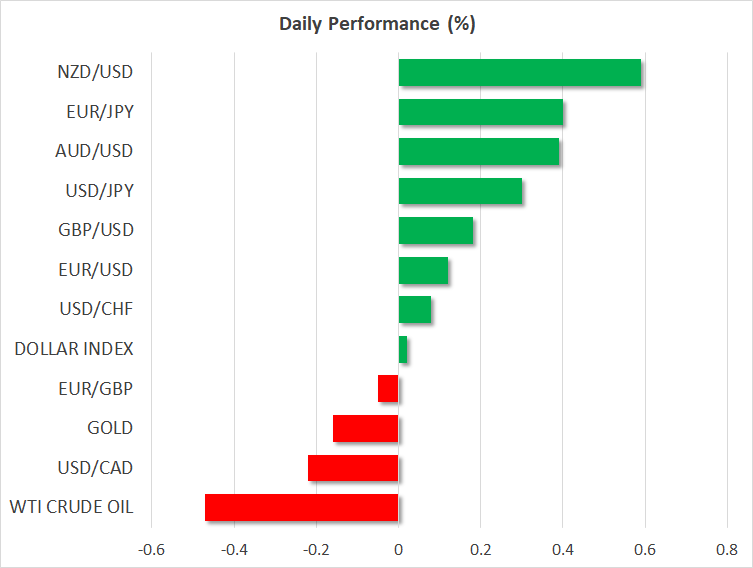

Major movers: Dollar rebounds from one-month low to trade little changed; antipodeans gain as trade war fears recede somewhat

The dollar index was roughly flat at 89.46 at 0630 GMT after previously falling to as low as 89.35, a level last seen on February 20. The greenback faced pressure versus the yen, hitting a fresh 16-month low of 104.55 before managing to recover to trade higher by 0.3%, a few pips above the 105 handle.

Continuing concerns over a possible global trade war and rising political uncertainty in Japan on the back of a scandal acting to the detriment of Japanese PM Shinzo Abe’s popularity were seen as reasons for the yen’s rise earlier in the day, but also last week when dollar/yen lost more than 1%.

Abe’s policies are supportive of a weaker yen and him losing popularity is seen by some as a reason to place long yen positions in forex markets. In relation to the scandal troubling his administration, the former Japanese tax agency chief will be testifying before parliament on Tuesday.

US President Donald Trump’s move last week, pertaining to the imposition of tariffs on Chinese imports to the US, refueled the trade war narrative and led to volatility in currency and equity markets, with the latter posting notable losses as risk sentiment soured. Indicatively, the S&P 500 lost a whopping 6% in the week that preceded. However, South Korea winning an exemption from US steel tariffs, spurred some hopes that an outright trade war would be averted and helped risk appetite somewhat and with it commodity-linked currencies, including the aussie and the kiwi. Specifically, aussie/dollar and kiwi/dollar traded higher by 0.4% and 0.6%, at around 0.7730 and 0.7280 respectively – the latter having earlier recorded an 11-day high of 0.7284.

Elsewhere, euro/dollar was 0.1% up at 1.2364, with the eurozone’s four largest economies releasing March CPI figures as the week unfolds, while pound/dollar edged higher by 0.2%, trading at 1.4162; this compares to last week’s near two-month high of 1.4216.

Overall, the greenback was broadly weaker against other major currencies, besides the yen which was also losing considerable ground versus the euro and sterling.

Day ahead: Speeches by key policymakers and trade developments in the spotlight

There are no major data releases on the economic calendar today, but there are several speeches by key policymakers that could attract market attention. Any updates in the “trade war” narrative will also be closely followed.

In the UK, the Bank of England’s highly-influential chief economist and MPC member Andy Haldane will speak in Edinburgh, though the exact timing remains tentative. Following last week’s BoE meeting, where two other MPC members dissented and voted for a rate hike, markets will probably scrutinize Haldane’s comments for any signals regarding the likelihood of a hike at the May gathering. Investors have currently priced in a 60% probability for such an action, according to the UK overnight index swaps. Considering that Haldane is often viewed as a “centrist” policymaker, if he indicates his support for a May hike then markets could push that probability higher, and the British pound alongside it.

In the US, New York Fed President William Dudley (a permanent voting member within the FOMC) will speak on regulatory reform before the US Chamber of Commerce at 1630 GMT. Cleveland Fed President Loretta Mester (voter) and Fed Board Governor Randal Quarles (voter) will also deliver remarks at 2030 GMT and 2310 GMT respectively. Meanwhile in Europe, ECB Governing Council members Jens Weidmann and Ewald Nowotny will step up to the rostrum at 1030 GMT.

In equity markets, focus will probably remain on the possibility of a US-China trade war materializing. Secretary Mnuchin’s comments over the weekend that he is “cautiously hopeful” a deal can be reached with China seem to have turned sentiment around somewhat, at least according to futures tracking the major US indices. Any comments from the Trump administration – and of course by China – will bear close watching. Risk sentiment is highly fragile at the moment, and even a single headline could have major repercussions for price action.

Interestingly, both the S&P 500 and the Dow Jones closed slightly above their corresponding 200-day moving averages (MA) on Friday, and it will be crucial to see whether those levels hold today. A rebound from the 200-day MAs could signify some stabilization in these benchmarks, whereas a downside violation would probably open the way for the February lows in these indices.

In terms of second-tier economic data, the US Dallas Fed manufacturing index for March will be released at 1430 GMT, but this is usually not a major market mover.

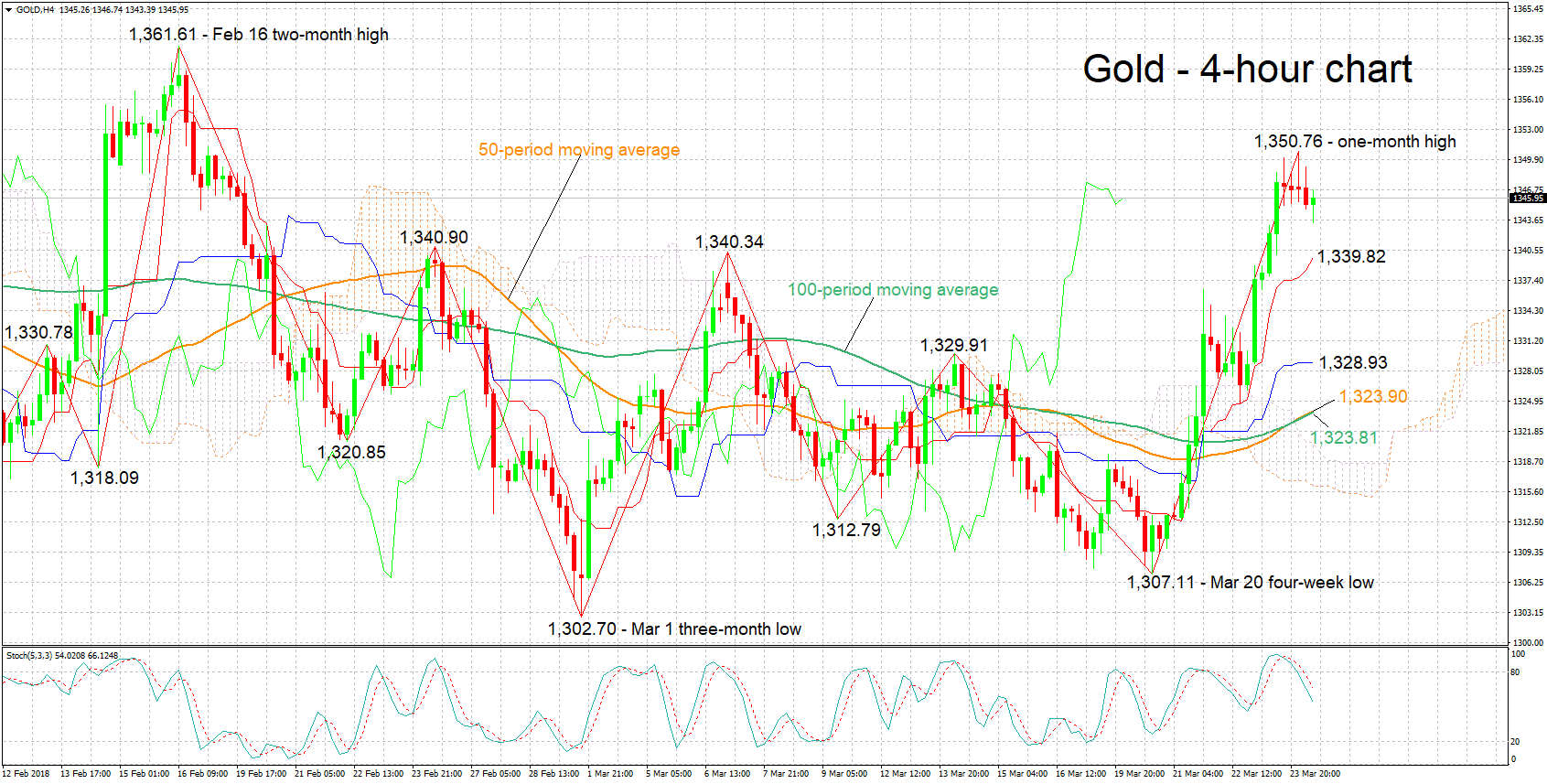

Technical Analysis: Gold hits fresh one-month high, bearish signal by stochastics in very short-term though

Gold posted notable gains in the week that preceded and reached a more than one-month high of 1,350.76 earlier on Monday. The Tenkan- and Kijun-sen lines are positively aligned in support of a bullish picture in the short-term for the precious metal, though the Kijun-sen has flatlined, suggesting that bullish momentum is losing steam. In addition, the stochastics are giving a bearish signal in the very short-term: the %K line has crossed below the slow %D one and both lines are heading lower.

Escalating tensions on the front of global trade have the capacity to lead to further gains for the safe-haven perceived asset, with resistance to advances potentially coming around the 1,350 handle which was somewhat congested in the past and which includes the more than one-month high from earlier in the day. An upside break off this area would increasingly turn the attention to the range around the two-month peak of 1,361.61 recorded around mid-February.

Abating fears over trade on the other hand are likely to reduce the precious metal’s attractiveness, potentially pushing it lower. The area around the 1,340 handle which encapsulates a couple of peaks from the recent past as well as the current level of the Tenkan-sen at 1,339.82 might act as support to price declines.

The direction of the greenback also can spur movements in the dollar-denominated commodity; a stronger greenback renders the metal less attractive to non-dollar holders and vice versa.