Here are the latest developments in global markets:

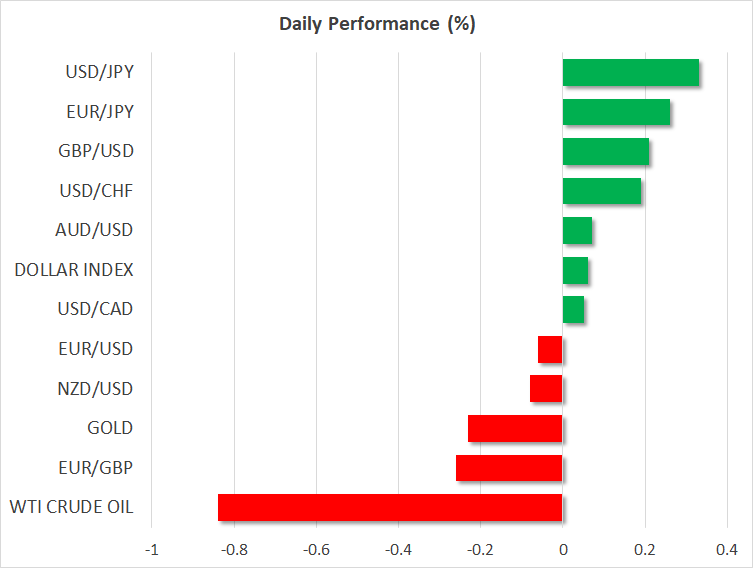

FOREX: The dollar was flat relative to a basket of currencies on Wednesday after adding 0.3% the previous day. Developments on trade were once again on the forefront and are likely to determine the short-term direction in the currency markets.

STOCKS: US markets closed significantly lower on Tuesday, dragged predominantly by technology stocks. Declines in Facebook and Nvidia, as well as news that the US is considering restricting Chinese investments in US technology companies may have contributed to the broader risk aversion. The tech-heavy Nasdaq Composite led the way lower, plunging by 2.9%, while the S&P 500 and the Dow Jones fell by 1.7% and 1.4% respectively. Futures tracking the S&P, Dow, and Nasdaq 100 are all currently close to neutral territory. As is often the case, the souring in risk appetite spilled over to Asia, which was a sea of red today. Japan’s Nikkei 225 and Topix indices declined by 1.3% and 1.0% correspondingly, while in Hong Kong, the Hang Seng fell by 1.6%. In Europe, while most indices closed higher yesterday, futures tracking all of the major benchmarks are currently flashing red, pointing to a lower open today.

COMMODITIES: Oil prices fell as well, on the back of the broader decline in equity markets, and the API crude inventory report showing a much larger-than-anticipated build in stockpiles. WTI crude fell by 0.8%, while Brent traded 0.7% lower. Today, markets will turn their focus to the official EIA inventory data, due out at 1430 GMT. In precious metals, gold is 0.2% lower, with the safe-haven perceived asset seemingly unable to draw support from the uncertainties over global trade. The recovery in the US dollar yesterday probably hurt demand for the dollar-denominated yellow metal, which tends to decline when the greenback strengthens.

Major movers: Dollar continues to distance itself from 16-month low vs yen

The dollar index was flat at 89.36 at 0630 GMT. This compares to a low of 88.94 hit yesterday, the lowest for the measure since February 16. Trade tensions remain in focus, with a US-German “alliance” against China being possibly on the table. This comes after easing concerns the previous day on the back of reports that the US and China are willing to enter into discussions on trade issues, deviating from the inflammatory rhetoric from previous days.

Despite attention being firmly on trade issues, updated GDP figures out of the US later today might also spur some movements, especially in the absence of other data. The US currency edged higher versus the yen, for dollar/yen to continue distancing itself from the 16-month low of 104.55 hit on Monday. The pair was trading 0.35% higher, at 105.70.

The improving geopolitical situation in the Korean peninsula is perhaps a factor that’s diverting funds out of the safe-haven perceived yen. China confirmed earlier on Wednesday that North Korea’s Kim Jong Un met with his Chinese counterpart Xi Jinping on a surprise visit to Beijing, this being his first such visit since taking power in 2011 and is a move that is seen as easing tensions in the region.

Euro/dollar was marginally lower around the 1.24 handle after losing 0.3% on Tuesday to retreat from a near six-week high of 1.2476. Catalysts for the common currency’s decline were weaker than anticipated data, including on business confidence, as well as some dovish-interpreted remarks from ECB Governing Council member Erkki Liikanen, who cautioned against premature tightening by the European Central Bank.

Sterling was 0.2% higher against the greenback at 1.4181, after falling 0.5% the previous day. Today’s gain came on the back of a report making reference to plans on avoiding a post-Brexit hard border with Ireland.

The aussie and the kiwi were not much changed versus their US counterpart after experiencing declines the previous day; the Australian currency’s losses brought it within breathing distance of the three-month low of 0.7765 recorded last week. The sell-off in Wall Street overnight dampened risk appetite, as well as sentiment for the two currencies which tend to gain in a risk-on environment. Meanwhile, data earlier on Wednesday showed New Zealand business sentiment declining in March, despite companies’ outlooks for their own activity being more upbeat.

Day ahead: Updates on global trade and Brexit likely to dominate quiet calendar day

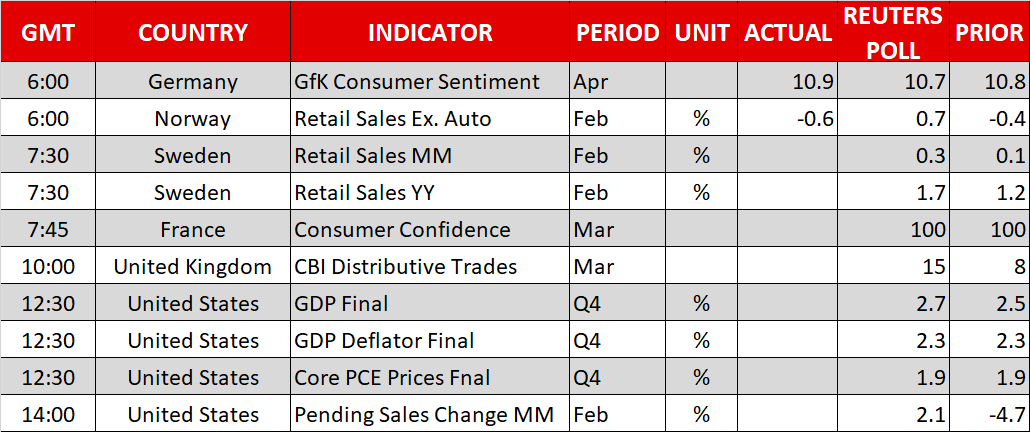

In the UK, the Bank of England (BoE) will release its survey of economic agents for Q1 at 0830 GMT, which reports on economic conditions in the UK based on conversations with over 700 businesses. This could provide some insights regarding wage pressures and investments in the UK economy ahead of actual data. A BoE rate hike in May is already priced in by 60% according to the UK overnight index swaps. In case this survey enhances expectations for such an action – for instance by showing signs of wage growth accelerating – then the British pound could extend its recent gains.

In Brexit news, UK press is reporting that the government is set to unveil new plans on how to avoid a “hard” Irish border, which has been one of the main hurdles in negotiations with the EU. Should the UK indeed present a practical solution, that would be another factor arguing for a stronger pound in the near-term, as the Brexit risk premium would probably decline on expectations of a comprehensive deal finally being reached.

In terms of economic data, the most noteworthy release today will be the final estimate of US GDP for Q4, due out at 1230 GMT. The final figure is anticipated to be revised higher to a 2.7% annualized pace, from 2.5% in the second estimate. Pending home sales for February are also due for release at 1400 GMT, and the forecast is for a rebound from the previous month.

In energy markets, the weekly EIA crude inventory data at 1430 GMT will be closely watched for a fresh indication of the state of US production and demand. Besides these data, traders will also keep their eyes on movements in the US dollar, how risk sentiment evolves, and any updates on whether Iran will face new sanctions.

In equities, price action will likely continue to be driven by incoming headlines around trade. In such an unpredictable environment, technical indicators could be particularly useful in determining the next directional wave. In this respect, note that the S&P 500 and the Dow Jones are both hovering near their respective 200-day moving averages and it will be critical to see whether they rebound from there, or break lower. Also of interest will be Facebook CEO Mark Zuckerberg’s hearing before a House committee in the aftermath of the privacy scandal involving the social-media giant. Moreover, we are approaching the end of the month as well as the quarter, and most European nations’ markets will stay closed on Friday. The Japanese fiscal year ends on Friday too, so many markets moves over the next days could be owed largely to flows, not fresh fundamental catalysts.

As for notable speakers, we will hear from Atlanta Fed President Raphael Bostic (voter) at 1530 GMT.

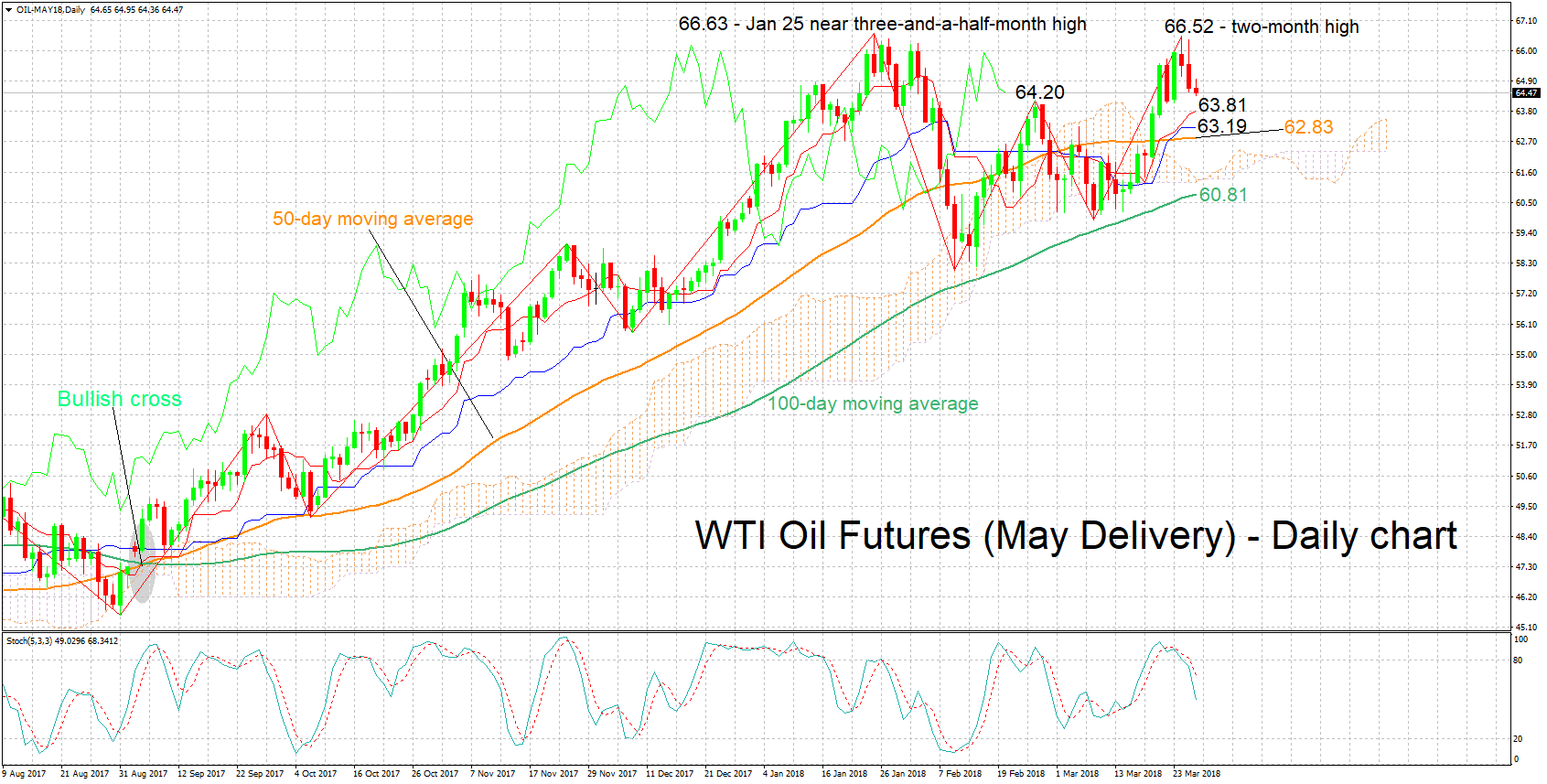

Technical Analysis: WTI oil futures retreat from 2-month high; EIA report to offer direction

WTI oil futures for May delivery have advanced considerably over the last couple of weeks, eventually reaching a two-month high of 66.52 on Monday, challenging the near three-and-a-half-year high of 66.63 recorded in late January. However, the price has since retreated from that high. The Tenkan- and Kijun-sen lines remain positively aligned though the flat Kijun-sen is an indication that bullish momentum has lost steam. Moreover, the stochastics are giving a bearish signal in the very short-term: the %K line has crossed below the slow %D one and both lines are moving lower.

If the Energy Information Administration’s weekly report shows a smaller-than-anticipated increase in US crude oil inventories – or a drawdown of course – prices could be supported. Resistance in this case might come around Monday’s two-month high of 66.52, with the area around this peak also including the near three-and-a-half-year high of 66.63 from January 25.

Should, on the other hand, crude stocks increase by more than expected, then prices could post losses. In this scenario, the range around the current level of the Tenkan-sen at 63.81 could act as support. The area around this point also includes the Kijun-sen at 63.19 and a previous peak at 64.20, while it was congested in the recent past as well. Numerous potential key points in case of a downside violation lie not far below: the current level of the 50-day moving average (62.83), the Ichimoku cloud top (61.33) and bottom (61.21), and the 100-day MA (60.81).

{kind=link}