U.S. Highlights

- Trade developments captured headlines this week. The U.S. disclosure of detailed plans regarding the tariffs on $50bn worth of Chinese imports led Beijing to retaliate with planned tariffs on $50bn of U.S. exports. The hardened Chinese stance led President Trump to threaten additional tariffs on $100bn worth of Chinese goods.

- While the announced tariffs are likely to merely shave off about 0.2pp from annualized GDP growth in the U.S. over the next two years, the potential for the conflict to escalate to a full-scale trade war is much more concerning.

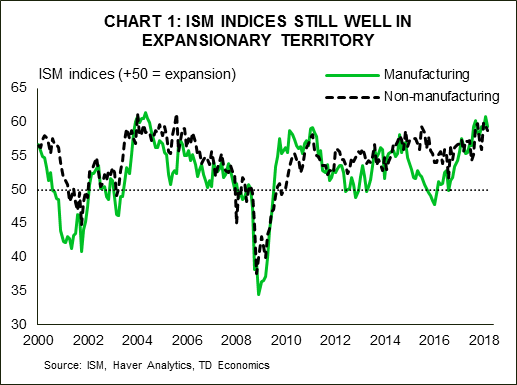

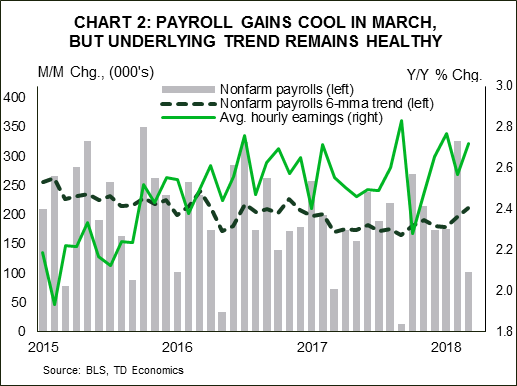

- Economic data came in healthy with the ISMs holding near recent highs while auto sales came in slightly better than expected in March. Payrolls disappointed despite a healthy ADP print, but wage growth accelerated on the month.

Canadian Highlights

- It was a good week for the Canadian dollar despite the pullback in oil prices. The loonie was lifted by improved prospects of a North American trade deal, with a preliminary agreement on NAFTA 2.0 potentially as early as next weekend, when leaders gather for the Summit of the Americas in Peru.

- Economic data was mixed. The trade deficit widened, with the weakness in net exports a drag on Q1 growth.

- On the other hand, the Canadian economy added an impressive 32.3 thousand jobs. The jobless rate held steady at 5.8%, with wage growth accelerating to 3.3% y/y. Wages were up a solid 3.1% y/y for permanent employees.

U.S. – Retaliating on Retaliation: Trade War Drums Beating

Equities have been on a rollercoaster ride this week, driven by shifting headlines on U.S.-China trade tensions. Initially, the U.S. announced details on its plans to levy a 25% tariff on $50 bn worth of goods imports from China, targeting some 1,300 items, including aircraft parts, batteries and medical devices. In a tit-for-tat move, China announced it would respond by mirroring the tariffs on American goods imports. The range of products targeted by China however, which included soybeans, cars, aircraft and chemicals, was narrower at 106 products. Later in the week, Pres. Trump instructed the U.S. Trade Representative to consider an added set of tariffs on $100 bn worth of imports. In what’s looking like a high-stakes poker game, China’s Ministry of Commerce said that China was prepared to “hit back forcefully” – reigniting trade war fears.

It is important to distinguish between tariffs that we already have details on and the latest inflammatory rhetoric. The former are not overly concerning. We estimate that the U.S. tariffs (including enacted tariffs on steel and aluminum) could shave off about 0.1 pp from annual GDP growth over the next few years, and could add up to 0.1 pp annually on inflation. Depending on what’s finally enacted following a consultation period, the price and demand impacts could be somewhat more pronounced if the tariffs are applied largely on consumer goods rather than business investment goods. On the other hand, China is targeting roughly 38% of American goods exports to China, which represent only about 0.3% of U.S. GDP. We estimate that these tariffs would reduce U.S. growth by up to 0.1 pp annually for the next two years. In this vein, slightly weaker U.S. demand could also act to offset some of the price pressures from the U.S. import tariffs.

The potential for the conflict to escalate is much more concerning. U.S. exports to China totaled $130 bn last year. This means that if the U.S. went ahead with tariffs on $100 bn of goods on top of what’s already being considered, and China reciprocated, the direct impact from exports would be much harsher given that all U.S. goods exports to China would face tariffs. The indirect impacts related to supply chain disruptions and the hit to business confidence and investment would also be more pronounced.

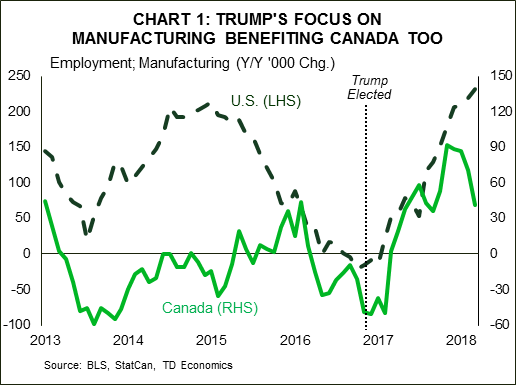

Developments on the trade front overshadowed decent signals from the economy. Auto sales came in slightly better than expected in March, and the ISM indices remained well in expansionary territory, despite easing off slightly (Chart 1). Payrolls gains slowed to 103k on the month, but this came atop of a very strong showing in February at 326k (Chart 2). Looking past the monthly noise, the underlying job market remains healthy, as demonstrated by increased wage gains – up 2.7% y/y.

Tax cuts and increased government spending are expected to add fuel to the labor market and the economy, with the latter expected to run at roughly 3% over the next few quarters. In short, the U.S. economy remains on a solid course, but further escalation in the trade conflict poses a material downside risk. The hope and expectation is for the conflict to be resolved through the ‘The Art of the Deal’ rather than ‘The Art of War’.

Canada – Loonie Lifted on Prospects for NAFTA 2.0

It was a fairly quiet start to the month across Canadian financial markets with little in the way of economic data until late in the week. The data that did come was mixed. International trade disappointed, while the labour market surprised to the upside. Equity markets limped along, dipping through midweek before recovering to end the week where they started. They were pressured lower by oil prices which slipped across major benchmarks on a bearish U.S. inventory report. The loonie strengthened nonetheless, benefiting from improving NAFTA prospects amidst U.S. dollar strength.

The greenback was lifted by another round of protectionist rhetoric out of the White House. President Trump on Thursday night called for a tripling of the value of Chinese exports subject to tariffs, to $150 billion. This was done as a response to a perceived hardening of the stance in Beijing – with Chinese officials suggesting that they will retaliate “at all cost”. While this is an unlikely scenario, since China’s economy would likely face a near-collapse should Americans stop buying its wares, the more aggressive positioning certainly raises the probability of a disorderly outcome.

Barring a potential global recession, the tougher stance towards China could work in Canada’s favour, offering an opportunity to fill some of the demand previously satiated by Chinese products. This is already apparent in the case of aluminum and steel, with more industries likely to be presented with an opportunity not available since the turn of the century – when China joined the WTO. This opportunity will be all the more apparent should a modernized trade pact, or NAFTA 2.0, be signed soon. With rumours of a potential announcement at the Summit of the Americas in Peru on April 13/14th, an agreement in principle may be on offer sooner than anticipated. While details would still need to be ironed out, such an outcome would allow U.S. trade negotiators to concentrate their efforts on levelling the playing field with China.

Canada’s trade relationship with the U.S. remains by-and-large balanced. The goods surplus shrank to $2.6 billion in February, according figures released on Thursday, with the figure largely offset by a deficit on the services side of the ledger. NAFTA 2.0 would be positive in removing uncertainty for businesses on both sides of the border but the deal is unlikely to bring back manufacturing jobs to Canada or the U.S. en masse. Still, the sector is faring well currently. The American manufacturing sector added 22 thousand jobs in March, taking the yearlong tally to 242 thousand. And despite the 8 thousand pullback in March, the sector added 41 thousand jobs in Canada over the last twelve-months.

All in all, Canada’s economy added 32 thousand jobs in March. This was above expectations but largely in line with the 296 thousand created over the past 12 months. The jobless rate was unchanged, as was wage growth – which remained at a healthy 3.1% y/y. Such performance, while unlikely to put a fire under the Bank of Canada, should provide plenty of comfort for another rate rise in the summer and a couple more next year, with a quicker tightening cycle likely particularly should NAFTA 2.0 be signed soon.

U.S.: Upcoming Key Economic Releases

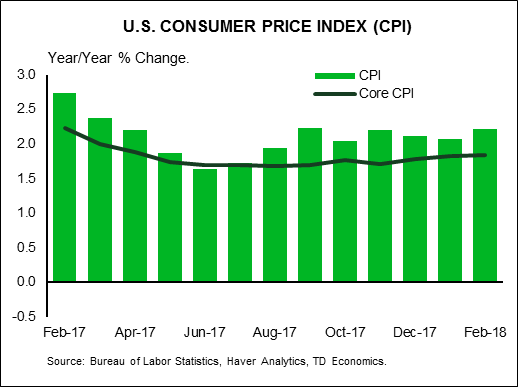

U.S. Consumer Price Index – March

Release Date: April 11, 2018

Previous Result: 0.2% m/m, core: 0.2% m/m

TD Forecast: 0.0% m/m, 2.4% core 0.2% m/m

Consensus: 0.0% m/m, core 0.2% m/m

We expect headline CPI inflation to accelerate further to 2.4% y/y in March, with prices flat on the month on a seasonally adjusted basis. Gasoline prices were little changed on the month and we expect higher electricity prices to be offset by lower natural gas prices. Excluding food and energy, we expect core CPI to print another 0.2% m/m increase. This assumes a correction in core goods prices, led by apparel and vehicle prices, offset by a rebound in core services, driven by the shelter component. Core inflation should move higher to 2.1% y/y though largely on a base effect. Thus, the strength of the m/m increase will be key to watch.

Canada: Upcoming Key Economic Releases

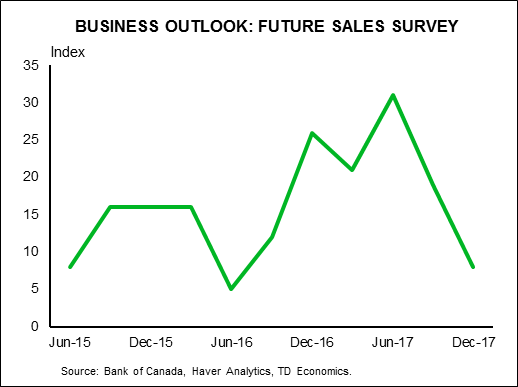

Bank of Canada Business Outlook Survey

Release Date: April 9, 2018

The Bank of Canada’s Business Outlook Survey (BOS) should reinforce the wider slowdown in the Canadian economy with a more cautious assessment of business conditions, but will stop short of sounding outright dovish. Since the previous survey, the economy has been subject to greater uncertainty on trade, a sharp minimum wage hike and a broad slowdown in housing, all the while without any relief on the poor competitive stance worsened by the US fiscal reform. We do not expect the survey to recognize recent progress in NAFTA talks, since consultations preceded the recent optimistic turn. However external demand remains robust, as evidenced by the pickup in US growth, and inflationary pressures continue to build, especially on the wage front or raw materials. This suggests the overall tone will be more mixed than the previous survey, but don’t expect to hear firms suggest that growth is stalling.