Here are the latest developments in global markets:

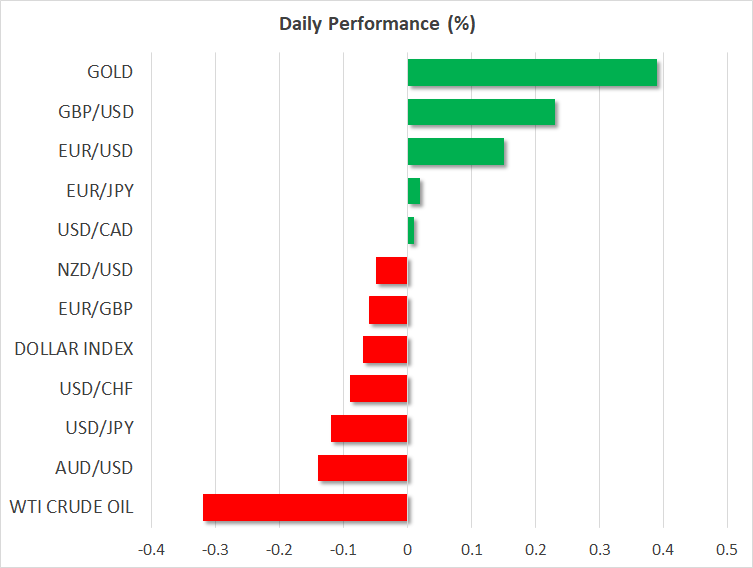

FOREX: The US dollar index traded nearly 0.1% lower on Wednesday, touching a fresh 2-week low ahead of the release of US CPI data and the minutes from the latest FOMC meeting. Both the euro and the pound gained yesterday, amid hawkish remarks from ECB and BoE officials respectively. Commodity currencies such as the aussie, kiwi, and loonie, were all a touch softer today, giving back some of the notable gains they posted yesterday as trade concerns abated.

STOCKS: US markets closed higher on Tuesday, buoyed by diminishing trade worries following the diplomatic tone in the Chinese President’s remarks. The Congressional testimony of Facebook CEO Zuckerberg likely played a role too, as the tech sector rallied in the aftermath. The tech-heavy Nasdaq Composite surged almost 2.1%, while the Dow Jones and S&P 500 gained 1.8% and 1.7% respectively. However, futures tracking the S&P, Dow, and Nasdaq 100 are all pointing to a lower open today, which may be related to expectations that a US military action in Syria is imminent. In Japan, the Nikkei 225 and the Topix closed lower by 0.5% and 0.4% correspondingly, though in Hong Kong, the Hang Seng gained 0.56%. In Europe, futures tracking all the major indices were a sea of red.

COMMODITIES: Oil prices corrected a little lower today, giving back some of the significant gains they posted yesterday. The catalyst for the gains were reports Saudi Arabia is aiming for $80/barrel oil prices, to boost the valuation of Saudi Aramco ahead of its planned IPO. Today, oil traders will turn their sights to the weekly EIA crude inventory data, for an update on US production. In precious metals, gold prices are 0.4% higher today, currently hovering near the $1344/ounce barrier. The gains seem to be related to geopolitical concerns, and specifically to the prospect of US military action in Syria that further jeopardizes US-Russian relations. The tumble in the dollar likely contributed as well.

Major movers: Euro gyrates on ECB speculation, commodity currencies bid amid abating trade risks

The euro went for a ride yesterday. The common currency surged initially following hawkish remarks from ECB Governing Council member Ewald Nowotny, who said that the ECB will wind down its QE program this year, and that the first deposit rate hike could be as large as 20bps. However, the ECB soon “intervened”. A spokesperson for the Bank noted Nowotny’s views are his own and don’t represent the Governing Council, backpedaling on the hawkish rhetoric and sending the euro back down. Still, the currency managed to rise again after that and finish the day higher overall, especially versus the yen that was on the back foot amid a risk-on environment.

In the big picture, even though investors already knew QE was most likely going to end this year, Nowotny confidence likely enhanced that narrative. Despite some softness in recent data, the ECB still looks set to taper its asset purchases in the autumn, with some signaling of that likely to come at the summer meetings.

The US dollar index traded nearly 0.1% lower on Wednesday, extending the losses it posted so far this week amid political and geopolitical uncertainties. At home, the Mueller investigation into Russian election-meddling is heating up, while overseas, the US is contemplating military action against Syria, risking further tensions with Russia. Not to mention trade risks, which although having subsided a little, are still present. Still, the dollar may get some reprieve from key economic releases today, which include the US CPIs for March and the minutes from the March FOMC meeting (see below).

Pound/dollar is 0.2% higher today, building on its gains from yesterday. The surge followed comments from BoE MPC member and notorious policy-hawk Ian McCafferty, who said the Bank should not wait to raise rates, amplifying expectations for a May hike.

Elsewhere, commodity-linked currencies enjoyed the reduction in trade uncertainties yesterday. The aussie, kiwi, and loonie all surged as investors sought riskier assets and diverted funds out of safe havens, like the yen.

Day ahead: FOMC meeting minutes & US CPI take the center stage

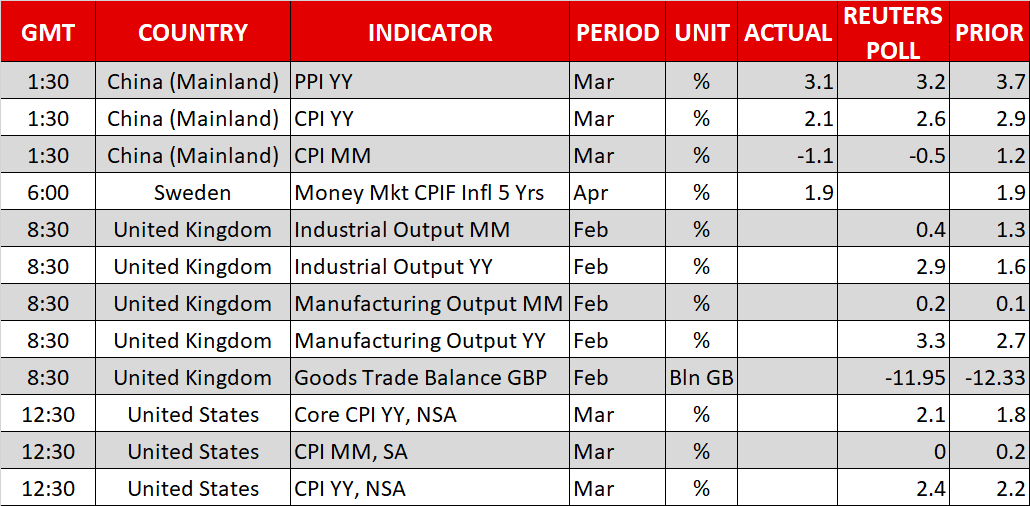

On Wednesday the FOMC meeting minutes due at 1800 GMT will be the highlight of the day as investors are eagerly waiting to identify details behind the Committee’s decision to raise interest rates at Jerome Powell’s first policy gathering as Fed Chairman. On March 20-21, policymakers raised interest rates as was widely expected and the closely-watched dot plot signalled two more rate hikes for 2018, which was already priced in by the markets. The latter was interpreted as a dovish sign since speculations were in the air that the Fed could deliver four rate hikes in total in 2018 instead of three. Policymakers, though, appeared more optimistic about this year’s rate path as the number of officials backing a steeper monetary tightening increased despite the median “dot” remaining unchanged at three hikes. The minutes will also reveal the Fed’s view on Trump’s trade policy, another spot that could add some volatility to the dollar.

Staying in the US, the Bureau of Labor Statistics will publish readings on consumer prices for the month of March at 1230 GMT. According to forecasts, the headline CPI is expected to edge up by 0.2 percentage points to 2.4% on a yearly basis, while the core measure, which excludes food and energy, is projected to increase to 2.1% y/y from 1.8% in February. This would be the highest growth recorded in a year.

In the UK, stats on manufacturing output and goods trade balance will attract attention, with analysts projecting an improvement in both measures. Particularly, production by manufactures is said to have grown by 3.3% y/y in February compared to 2.7% in the preceding month, while the trade deficit in goods is anticipated to have narrowed from 12.33 billion pounds to 11.95bn in February. Should the data surprise to the upside the pound could extend yesterday’s gains, that emerged after BoE MPC member Ian McCafferty stressed the need to raise rates as wage growth could appear stronger than policymakers believe.

In energy markets, the Energy Information Administration (EIA) will report on US oil inventories for the week ending April 6 at 1430 GMT. Oil prices jumped to two-week highs yesterday amid easing tensions between the two largest oil consumers, the US and China, despite the American Petroleum Institute indicating on Tuesday a larger-than-expected increase in US crude oil stocks for the aforementioned week and the EIA saying that crude oil production could rise more than previously thought.

As for today’s public appearances, the ECB President, Mario Draghi will be speaking in Frankfurt at 1100 GMT, while the ECB members Pentti Hakkarainen and Ignazio Angeloni are scheduled to deliver remarks at 1300 GMT and 1440 GMT respectively. In the US, Facebook’s chief executive, Mark Zuckerberg, will be in the hot seat for the second day, testifying before the House Energy and Commerce Committee regarding the sharing of private information with the London-based data mining firm Cambridge Analytica which had connections with Trump’s campaign in 2016.

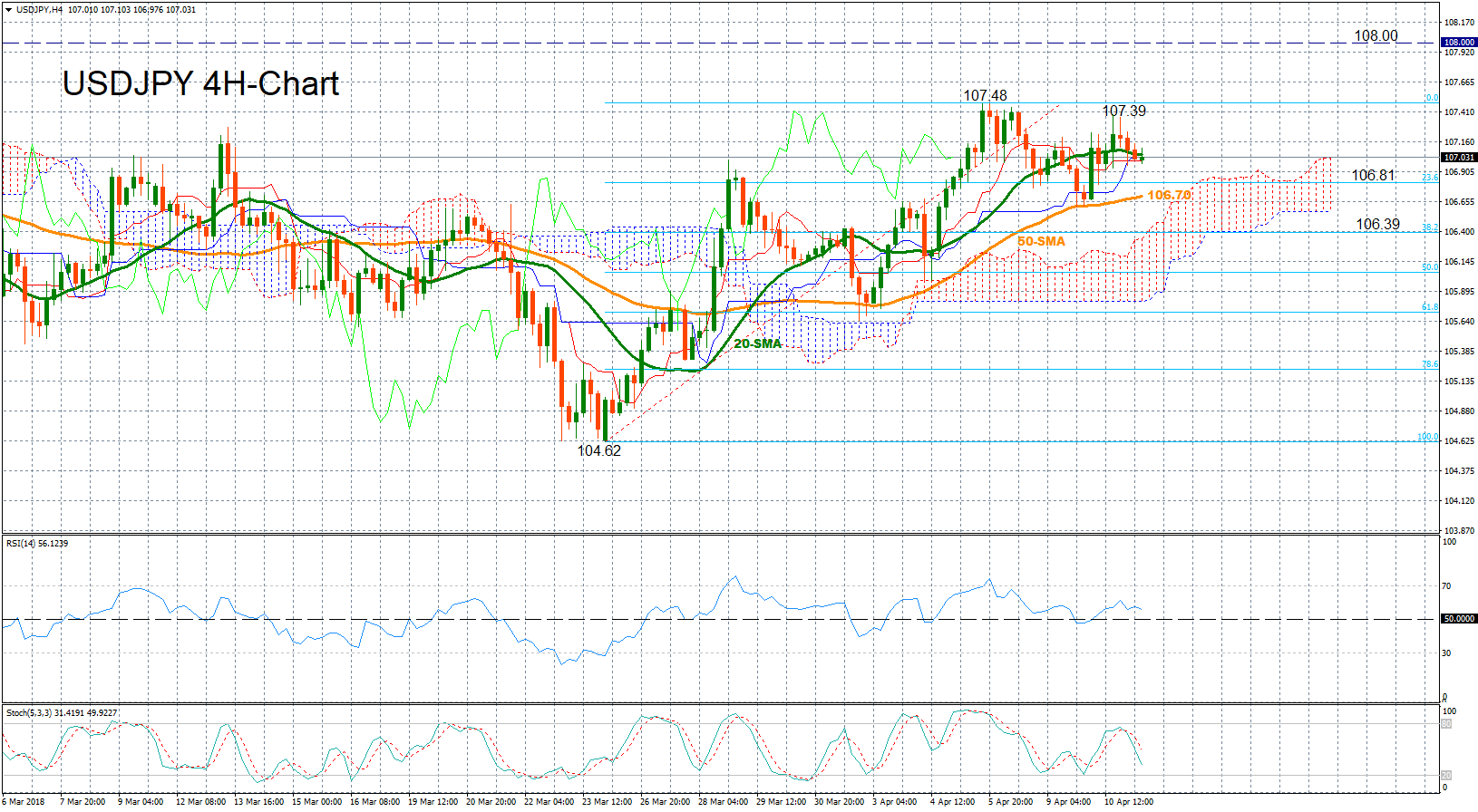

Technical Analysis: USDJPY sends bearish signals for the short-term

USDJPY rebounded adequately yesterday after it found support at the 50-period simple moving average line (SMA) in the four-hour chart. But today the market is turning lower and the technical indicators suggest that weakness might persist in the near term as the RSI is heading lower towards its neutral threshold of 50 and Stochastics are moving downwards after posting a bearish cross.

The pair, though, will be waiting for the US CPI figures and the FOMC meeting minutes today in hopes to regain its strength. In case the CPI numbers beat expectations and the minutes prove hawkish, increasing the odds for further monetary tightening this year, dollar/yen could bounce back to yesterday’s high of 107.39 before it tests the more-than-a-one-month high of 107.48 printed last week. Any break above from there could open the door to the 108 handle.

In the alternative scenario, dovish headlines could extend losses towards 106.81, the 23.6% Fibonacci of the upleg from 104.62 to 107.48, while in the event of steeper declines, the 50-period SMA currently at 106.70 could provide support ahead of the 38.2% Fibonacci of 106.39.