Here are the latest developments in global markets:

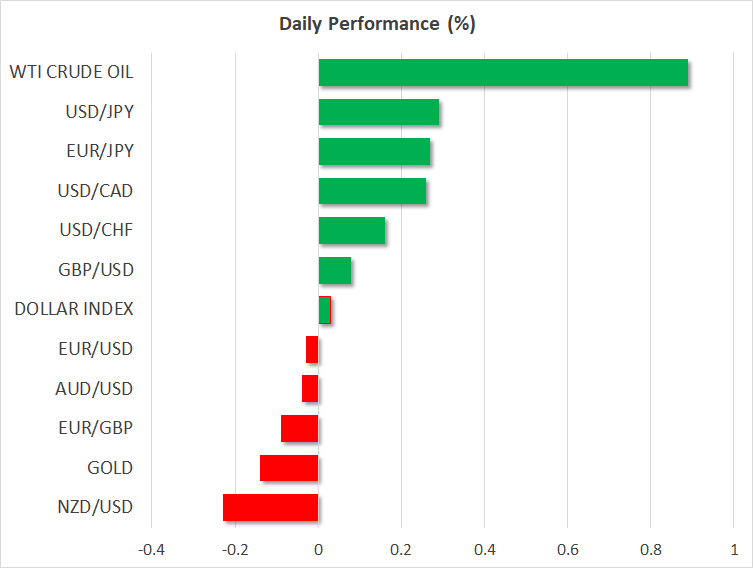

FOREX: The US dollar index was practically unchanged on Wednesday, after it posted some gains on Tuesday. The Japanese yen and the Swiss franc were on the back foot as geopolitical risks were perceived as easing, while the British pound steadied somewhat after retreating yesterday.

STOCKS: US markets soared for a second day in a row, as a strong earnings season and diminishing risks on the Korean Peninsula boosted risk appetite. The Nasdaq Composite led the way higher, climbing by 1.74%, buoyed by Netflix (+9.2%) and Amazon (+4.3%). Meanwhile, the S&P 500 and the Dow Jones gained nearly 1.1% and 0.9% respectively. Moreover, futures tracking the Dow, S&P, and Nasdaq 100 are all pointing to a slightly higher open today. Asia was a sea of green as well. Japan’s Nikkei 225 and Topix surged by 1.4% and 1.1% correspondingly, while in Hong Kong, the Hang Seng gained 0.4%. Over in Europe, futures tracking all the major benchmarks were flashing green as well.

COMMODITIES: Oil prices edged up amid the broader risk on environment. WTI rose by 0.9% on Wednesday, while Brent gained 0.8%. Besides risk appetite, prices were supported by a surprising drawdown in the private API crude inventory data, which likely fueled speculation for a similar reaction in today’s official EIA stockpile figures. In precious metals, gold traded 0.15% lower, last seen near the $1345/ounce barrier. The safe haven is being weighed on by a combination of diminishing geopolitical risks in Korea and in Syria, as well as a broader improvement in risk sentiment.

Major movers: Yen drops as North Korea risks fade, sterling retreats after data

The most notable moves overnight were seen in the Japanese yen, which fell by nearly 0.3% against both the dollar and the euro as tensions on the Korean Peninsula eased. The risk-on reactions came after President Trump said the US and North Korea have been holding talks “at extremely high levels” to try to arrange a summit between himself and Kim Jong Un. Soon thereafter, media reports said that CIA Director and soon-to-be Secretary of State Mike Pompeo had travelled to North Korea over the Easter and met with Kim, laying the groundwork for a meeting between the leaders.

Coming on top of separate reports yesterday that the two Koreas are discussing plans for ending their military conflict – as they are still at war technically – these signals likely amplified the narrative that things are calming down. Bearing also in mind that the situation in Syria is not expected to escalate further, geopolitical risk premium appears to have declined significantly. Besides the yen, the safe-haven Swiss franc also tumbled. Euro/franc climbed to 1.1970, its highest level in three years – ever since the SNB removed the floor in the pair.

On the trade front, developments were a mixed bag. China pledged to allow US car makers greater freedom in its market, but also imposed temporary 179% tariffs on American sorghum, a grain used to feed livestock. The move is consistent with China’s approach to this entire ordeal so far; the nation is willing to make some concessions, but will not shy away from a trade standoff either. While these developments were largely overlooked by equity investors, who instead focused on diminishing geopolitical tensions and a strong earnings season, they serve as a reminder that trade risks are still looming and that we have not entered the “talks” phase just yet.

Elsewhere, the British pound steadied against the dollar today, after it retreated off its nearly-two-year-high on Tuesday. The tumble in the pound came after UK wage growth data disappointed. Nonetheless, the probability for a BoE rate hike in May remained elevated at 70%. Today, markets will focus on the release of the nation’s inflation data (see below).

Day ahead: UK inflation and Bank of Canada decision the highlights of the day

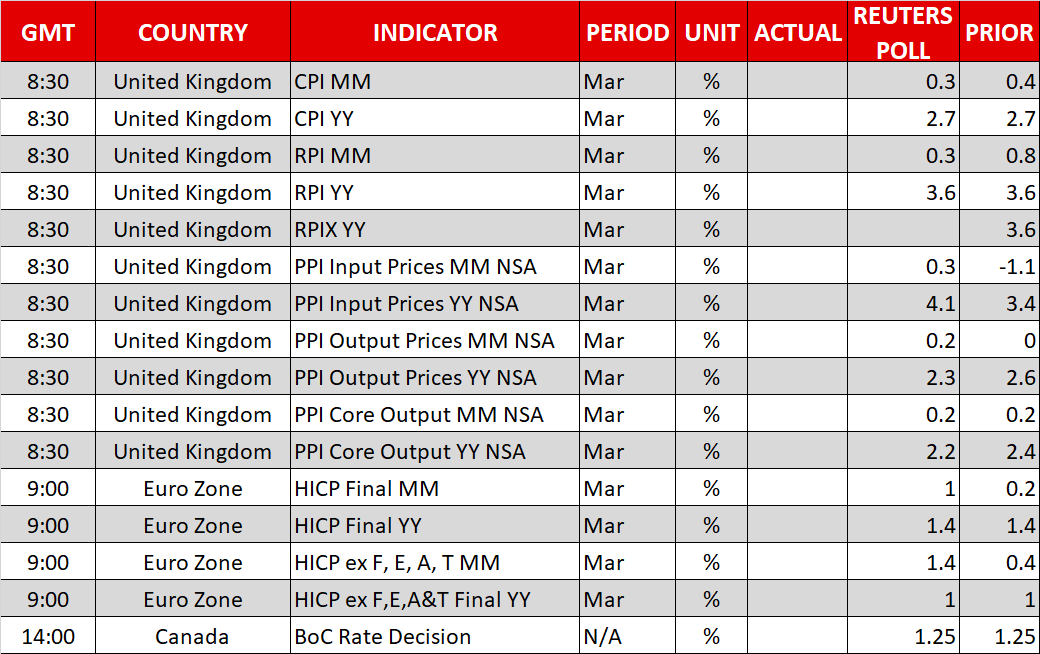

UK CPI figures and the Bank of Canada’s interest rate decision are likely to attract the most attention out of Wednesday’s economic calendar.

At 0830 GMT, UK inflation figures will be made public. Headline CPI is projected to stand at 2.7% y/y in March, the same pace as in February, while on a monthly basis it is expected to ease to 0.3% from 0.4%. If the numbers come in line with expectations, they would perhaps instill more confidence in positive real income growth making a comeback; Tuesday’s data showed average weekly earnings rising by 2.8% y/y. Core CPI will also be watched, while data on producer prices and retail price inflation – a measure used for the indexation of pensions and the adjustment of indexed-bonds – will be released at the same time as well.

UK overnight index swaps are projecting a 70% probability for a May rate hike by the Bank of England. It would be interesting to see how the odds for such a move are affected after the release of today’s figures.

Inflation figures for the month of March out of the eurozone are also slated for release today (0900 GMT), though those will pertain to the final release and are thus not that likely to spur sharp movements in currency markets.

Later in the day, the focus will turn to the Bank of Canada which will be completing its two-day meeting on monetary policy. The decision on interest rates is scheduled for release at 1400 GMT. The Bank is not expected to proceed with a rate hike, though there has been rising speculation for the central bank to tighten policy in the meeting that follows. To the extent the BoC signals that such a move could take place – for example by expressing confidence on a positive outcome in NAFTA talks – then the loonie is likely to receive a boost. The Canadian dollar is currently trading not far below a two-month high versus its US counterpart. Also on the agenda is a press conference by BoC Governor Stephen Poloz and Senior Deputy Governor Carolyn Wilkins at 1515 GMT.

Of interest to oil traders will be EIA’s report on US crude stocks for the week ending April 13. Crude inventories are anticipated to decline by 1.4 million barrels after rising by 3.3m in the previously tracked week.

With the earnings season in full swing, Morgan Stanley will be releasing its quarterly results before Wednesday’s US market open.

Fed officials making appearances include outgoing New York Fed President William Dudley (1900 GMT) and Fed Vice Chair for Supervision Randal Quarles (2015 GMT). Both hold permanent voting rights within the FOMC. Also attracting some interest is the Federal Reserve’s Beige Book which gauges current economic conditions in the 12 Federal districts in the US. It is scheduled for release at 1800 GMT.

In politics, US President Donald Trump and Japanese Prime Minister Shinzo Abe will be completing their two-day meeting taking place in Florida. Up to now, talks have focused on the prospective U.S.-North Korea summit that could take place around May or June. Trade issues are likely to be discussed as well.

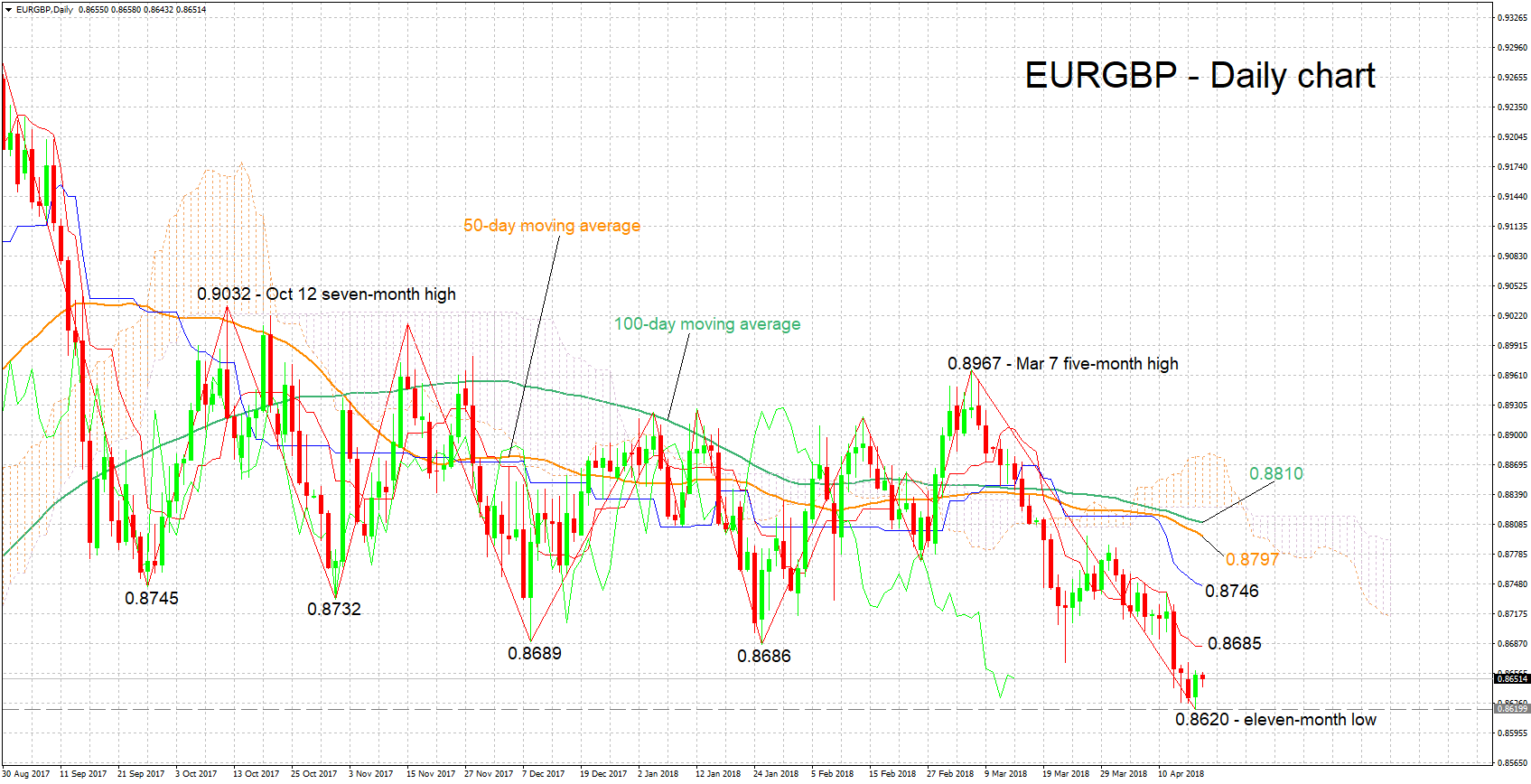

Technical Analysis: EURGBP short-term bearish, trades not far above 11-month low

EURGBP has lost considerable ground after touching a five-month high of 0.8967 on March 7, eventually reaching an 11-month low of 0.8620 during Tuesday’s trading. The Tenkan- and Kijun-sen lines are negatively aligned in support of a bearish short-term picture. Notice though that the Chikou Span may be signaling an oversold market.

If today’s UK data more conclusively put a May rate hike by the Bank of England on the table, then EURGBP is likely to decline, with support potentially coming around yesterday’s 11-month low of 0.8620; the 0.86 round figure is also part of the area around this trough.

On the upside and in case market participants see reduced chances for a May rate increase, resistance could come around the current level of the Tenkan-sen at 0.8685. Notice that the range around this point encapsulates a couple of bottoms from the recent past, as well as the 0.87 handle.