Here are the latest developments in global markets:

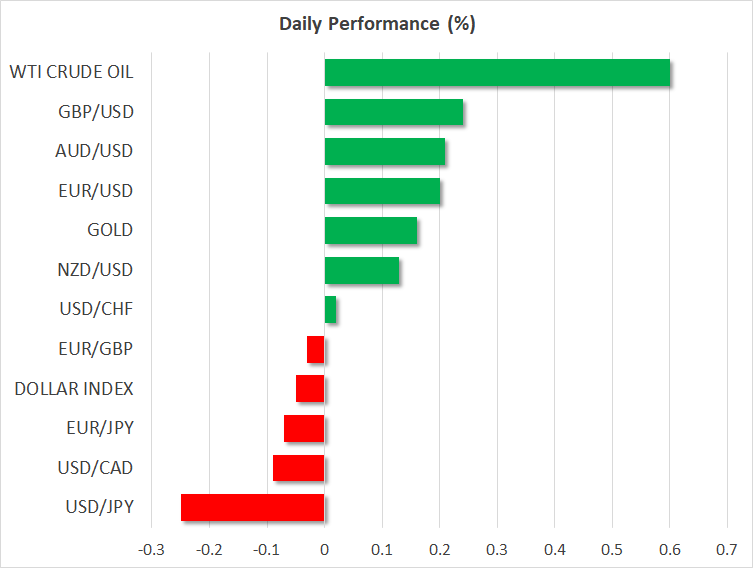

FOREX: The dollar index continued to trade near 3 ½ -month highs reached yesterday in the early European session on Thursday as the 10-year Treasury yields remained above 3.0% for the first time in four-years, last seen at 3.02%. Dollar/yen retained strength above the 109 key-level, with easing geopolitical and trade tensions supporting the pair as well but was slightly down on the day at 109.28 (-0.12%). Euro/dollar, posted limited gains ahead of the ECB rate decision later today, hovering at 1.2172 (+0.12%) as the rise in US treasury yields widened further the gap between US-German government bond yields. Investors were also scaling back long positions on the pair lately in expectations that the ECB would gradually move towards the end of its stimulus reduction program. Meanwhile, in Sweden, the central bank kept interest rates unchanged, saying that rates could rise towards the end of the year, later than previously thought due to a subdued inflation. In the wake of the news, dollar/krona rallied to 8.61 (+0.24%) the highest since the end of June, while euro/krona crawled up to a fresh 8-year high of 10.48 (+0.33%). Pound/dollar touched one-month lows at 1.3894 before a rebound towards 1.3943 (+0.09%) as traders remained cautious on whether the BoE will deliver a rate hike in May following dovish comments by the BoE governor earlier this month. Developments on the Brexit front were also not so bright either, with the House of Lords voting against the Brexit withdrawal bill which aims to leave the UK outside of the EU’s customs union. The antipodean currencies were trading flat, with aussie/dollar and kiwi/dollar fluctuating around 0.7575 and 0.7067. Dollar/loonie was also moving sideways around 1.2839.

STOCKS: European stocks were recovering from yesterday’s downfalls helped by encouraging corporate earnings results. At 0830 GMT, the pan-European STOXX 600 and the blue-chip Euro 50 were up by 0.27% and 0.24% respectively led by industrials, utilities, and consumer cyclicals. The German DAX 30 rose by 0.17%, the French CAC 40 climbed by 0.42%, the Italian FTSE MIB jumped by 0.56%, while UK’s FTSE 100 was flat. In Asia, stocks closed mixed, while futures tracking US stock indices were flashing red, pointing to a negative open. In corporate news, Phillips lighting, the world’s largest lighting maker, reported disappointing earnings numbers for the first quarter of 2018, with its shares tumbling by 12.6%. Deutsche Bank also saw its shares falling after its net profit declined by 79% y/y in Q1 2018, announcing its plans to reduce bond and equity trading in the US and Asia. Oil companies such as the Finish oil refining firm Neste and France’s Total were among gainers, with both companies recording an upbeat performance in the first three months of 2018.

COMMODITIES: Oil prices were heading to the upside on the back of a declining output in Venezuela and growing concerns that the US would re-impose sanctions to Iran. Yesterday, the French President Emanuel Macron, who spend three days in the US to persuade the US President to remain on the 2015 nuclear deal, expressed that the US President would likely leave the deal. WTI crude and Brent rose to $68.45 (+0.59%) and $74.48 (+0.78%) per barrel respectively. In precious metals, gold reversed earlier gains, returning to $1,322.30 per ounce.

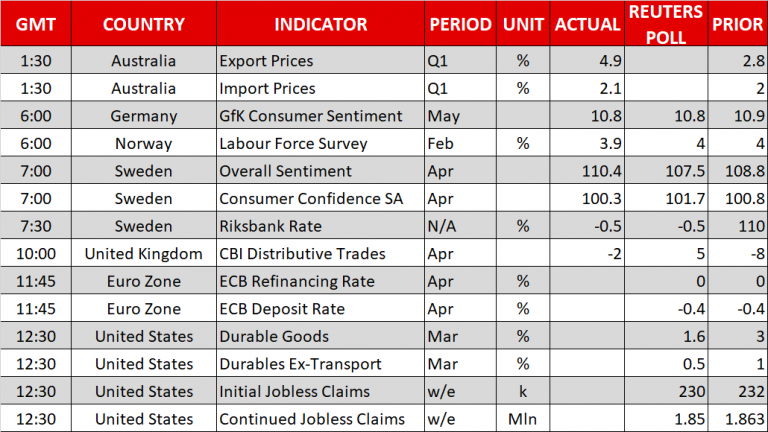

Day Ahead: ECB rate decision under the microscope; US durable goods & initial jobless claims coming up

All eyes will be on the European Central Bank today. Although no change is expected to monetary policy, traders will be eager to hear whether policymakers feel more confident to end the quantitative program at the end of the year. Still, some analysts believe that the ECB Governor, Mario Draghi who will hold a press conference at 1230 GMT following the rate announcement at 1145 GMT, will probably avoid any comments that could signal adjustments on the current monetary strategy, though, he might acknowledge the weakness in the Eurozone’s economic performance mirrored by the latest disappointing figures. June’s meeting, which will be accompanied by new economic projections might attract a greater attention.

Turning to the US, durable goods for March are scheduled for release at 1230 GMT. Headline orders are expected to ease to +1.6% m/m from +3.0% m/m in the preceding month, whilst the core durable orders (excluding transportation) are forecasted to tick lower to 0.5% m/m from 1.0% m/m in the previous month. Initial jobless claims due at the same time will be in focus as well. The number of people applying for unemployment benefits for the first time is anticipated to edge down to 230k in the week ending April 20 compared to 232k in the preceding week.

Elsewhere, New Zealand will see the release of trade stats at 2245 GMT, while in Japan, employment figures and initial estimates on industrial production for the month of March as well as April’s CPI numbers will attract attention.