Here are the latest developments in global markets:

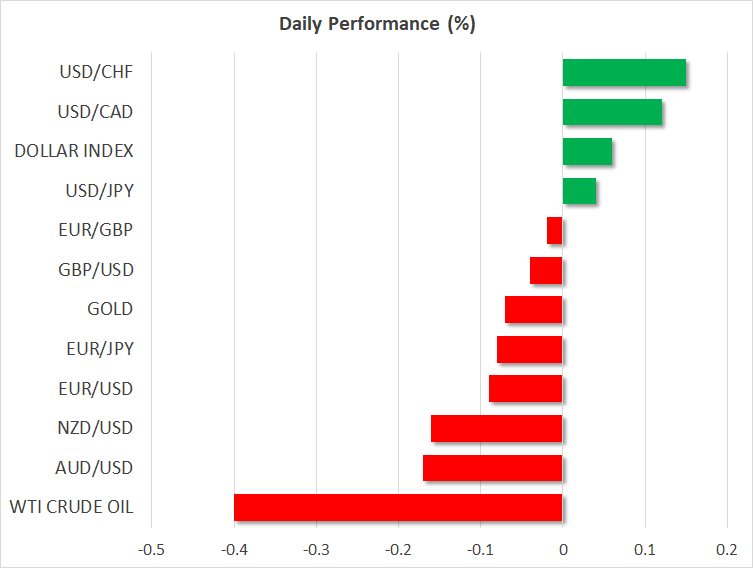

FOREX: The US dollar index is higher on Friday, but by less than 0.1%, building on the gains it posted yesterday. Meanwhile, the euro was on the back foot, after the ECB maintained a relatively cautious tone in yesterday’s policy gathering.

STOCKS: US markets edged higher yesterday, as a raft of encouraging earnings releases and a pullback in US bond yields supported risk appetite. The tech-heavy Nasdaq Composite climbed by 1.64%, boosted by AMD (+13.7%), Facebook (+9.0%), and Amazon (+3.95%). Meanwhile, the S&P 500 and the Dow Jones gained 1.04% and 0.99% respectively. As for today, futures tracking the Nasdaq 100 are in positive territory, but those tracking the Dow and S&P are flashing red. The optimism in Wall Street rolled over into Asia too. In Japan, the Nikkei 225 and the Topix rose by 0.66% and 0.29% correspondingly, while in Hong Kong, the Hang Seng was 0.71% higher. Europe was a similar story, with futures tracking all the major indices pointing to a higher open today.

COMMODITIES: Oil prices declined a little on Friday, though they still remain elevated near their recent highs. WTI and Brent crude are lower by 0.4% and 0.5% respectively, giving back some of the gains they posted on Thursday. The broader narrative in the oil market remains one of expectations for sanctions on Iran soon, speculation around which has limited any significant declines in prices recently, even despite signs that US production continues to soar. In precious metals, gold is nearly 0.1% lower today, extending losses from yesterday. The safe haven continues to be battered by a recovering dollar, and evidently by the latest improvement in Wall Street’s risk appetite as well. The easing tensions on the Korean peninsula may have also played a role. It is currently trading near the $1,316 per ounce mark, and should these factors continue to weigh on demand, the next stop may be the March lows, at $1,307.

Major movers: Euro sinks after Draghi fails to impress bulls; BoJ drops timeframe for hitting inflation goal

The euro tumbled yesterday, following the ECB’s policy meeting. The Bank kept both its policy and guidance unchanged, as was widely expected, so attention quickly turned to the press conference by President Draghi. While the ECB chief began by indicating the economy remains on a strong course, he quickly acknowledged that there has been some moderation in economic data as of late.

And although he noted this slowdown appears to be owed to transitory factors that will soon fade, Draghi also entertained the possibility it may prove to be more persistent, indicating the Bank will monitor such risks closely. He even added the Governing Council hadn’t discussed the future of the QE program at all, as that would be premature without a better understanding of the slowdown. Implicitly, Draghi left open the scenario that the ECB may delay its normalization plans should the situation deteriorate further, likely disappointing those looking for clear signals that the days of QE are drawing to an end.

While the ECB still looks set to scale back its purchases later this year, with some signaling of that likely to come in the summer, economic data bear even closer monitoring, as further deterioration could make the Bank more cautious to head towards the exit.

Overnight, the Bank of Japan (BoJ) also remained on hold. Interestingly, policymakers removed from the policy statement a phrase that previously stated the Bank expected to hit its inflation target in the fiscal year 2019. Officials also made several references to downside risks surrounding the economy and inflation. While the yen barely reacted to these signals, the Bank’s cautiousness should put to bed any surviving speculation that an exit from ultra-loose policies is looming anytime soon. In isolation, this is a factor supporting a weaker yen, though the currency’s direction will also depend on how risk sentiment evolves, given its status as a safe haven.

In geopolitics, Kim Jong Un became the first leader of North Korea to cross over into South Korea since the peninsula was divided, as part of talks aimed at defusing tensions.

Elsewhere, both aussie/dollar and kiwi/dollar are roughly 0.2% lower today, continuing to extend their recent collapse.

Day ahead: US & UK GDP figures in focus

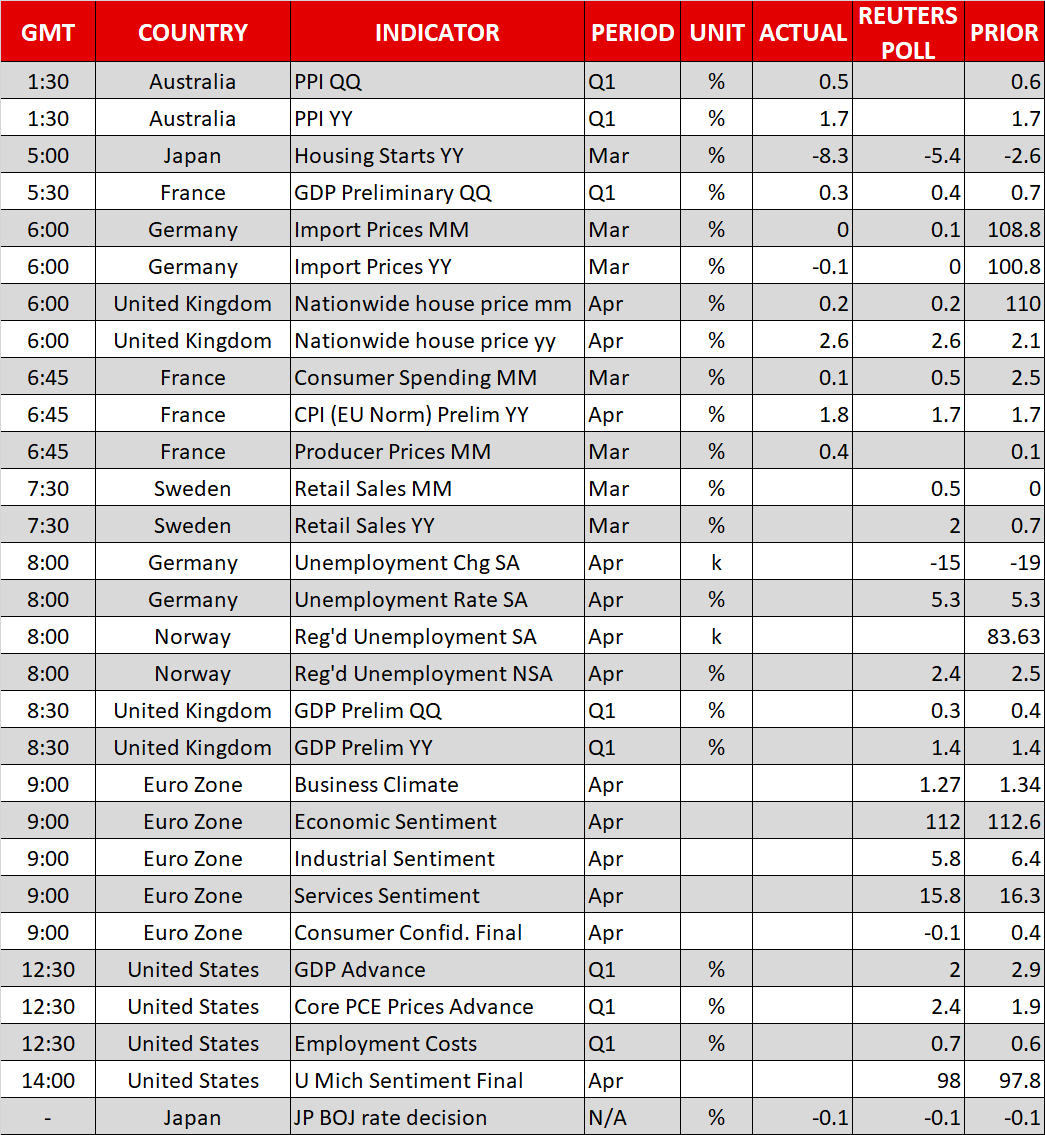

Friday’s economic calendar is a rather packed one and includes the release of preliminary Q1 GDP estimates out of the US and the UK.

At 0800 GMT, Germany will see the release of unemployment-related figures. The unemployment rate in the eurozone’s largest economy is forecast to remain unchanged at 5.3%, this being the lowest since the nation’s reunification in 1990.

The attention will next turn to the UK, with preliminary Q1 GDP estimates scheduled to be made public at 0830 GMT. On a yearly basis, the pace of growth is anticipated to stand at 1.4%, the same as in Q4 2017, while on a quarterly basis it is projected to tick down to 0.3% from 0.4%. The data have the capacity to, at least in part, shape expectations for May’s Bank of England meeting and will thus be closely watched; UK overnight index swaps currently put the odds for a rate hike close to 50%.

The eurozone will be on the receiving end of numerous business surveys at 0900 GMT, all of them expected to show further deterioration of sentiment in April. Meanwhile, the European Commission’s Directorate General for Economic and Financial Affairs will release its final reading on consumer confidence for the month of April at the same time. The relevant print is expected to enter into negative territory for the first time since October.

Later in the day, the focus will shift to the US, with the advance estimate of Q1 GDP growth due at 1230 GMT. A considerable decline in the pace of expansion is projected relative to the preceding quarter – 2.0% expected vs 2.9% in Q4. The US economy routinely delivers poorer growth figures in the beginning of the year though, and FOMC members are likely to look past first-quarter weakness when they gather next week for their two-day monetary policy meeting concluding on May 2. Other releases that will be made public alongside GDP numbers are Q1 employment costs, as well as the advance estimate of core PCE prices for the same quarter, while the University of Michigan’s final print on consumer sentiment for the month of April will be released at 1400 GMT.

Energy giants Chevron and Exxon Mobil will be reporting their Q1 results before the US market open.

In oil markets, the Baker Hughes oil rig count is due at 1700 GMT.

Policymakers making appearances include ECB Executive Board member Yves Mersch who will be speaking on the unwinding of QE at 0800 GMT. At the same time, the Swiss National Bank President Jean Studer and the Bank’s Chairman Thomas Jordan will be speaking at the central bank’s General Meeting of Shareholders. BoE Governor Mark Carney will be making an appearance as well (1400 GMT), though the topic of discussion renders comments on monetary policy unlikely.

In politics, a meeting between US President Donald Trump and German Chancellor Angela Merkel at the White House might attract interest, while the Korean summit with the leaders of North and South Korea meeting is also considered of importance.

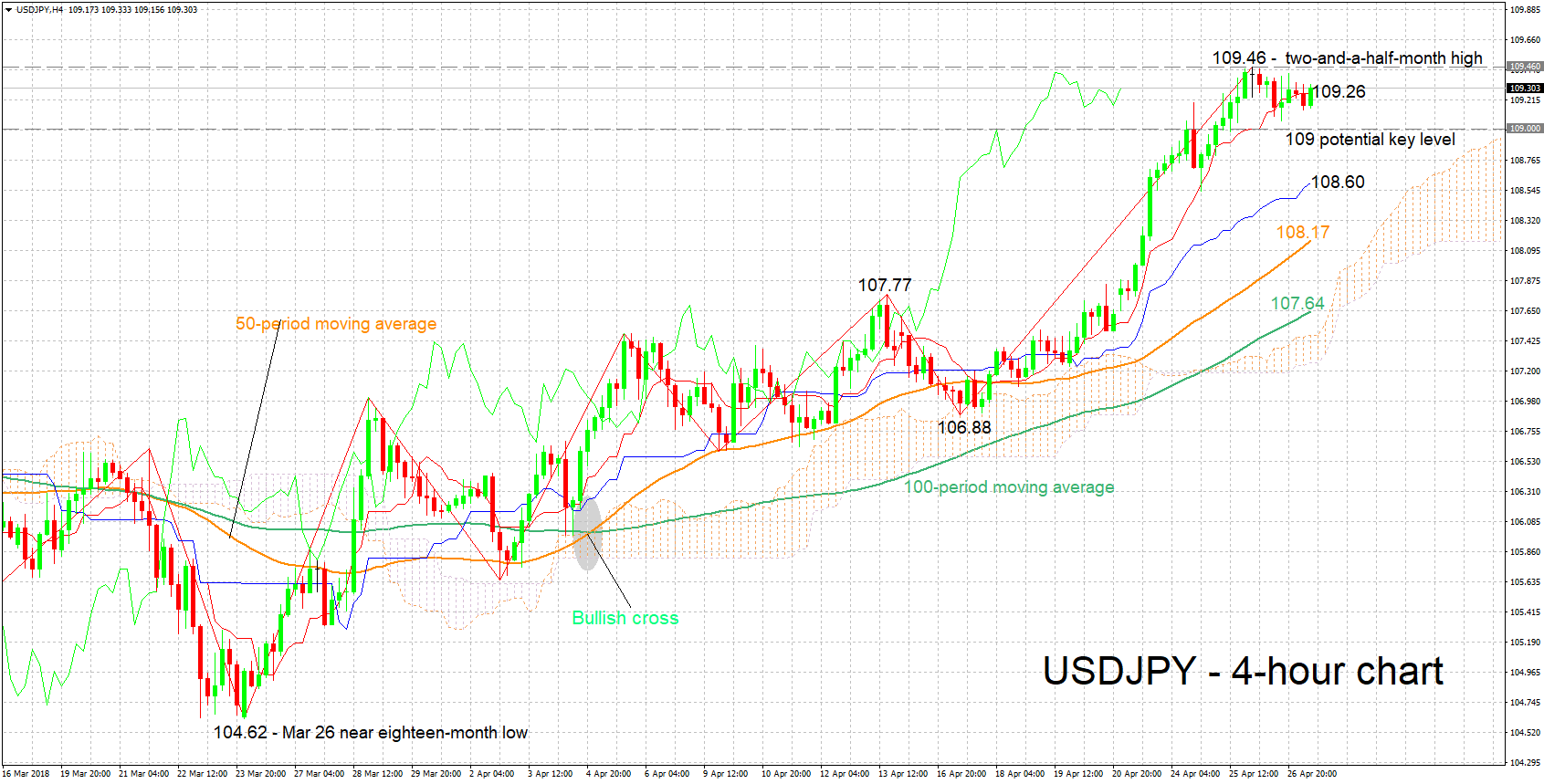

Technical Analysis: USDJPY short-term bullish; trades not far below 2½-month high

USDJPY has posted significant gains in recent days, rising to a two-and-a-half-month high of 109.46 on Thursday. It currently trades roughly 16 pips below that peak. The Tenkan- and Kijun-sen lines are positively aligned in support of a bullish picture in the short-term.

Upbeat US GDP figures are likely to boost the pair which currently may be meeting resistance around the Tenkan-sen at 109.26 (the Tenkan-sen itself being violated). A more decisive break above could meet a barrier around yesterday’s high of 109.46 and the 110 round figure which may be of psychological importance.

Weaker-than-anticipated US figures might push the pair lower. Support in case of declines could come around the 109 handle and further below from the range around the Kijun-sen at 108.60.