The financial markets are relatively quiet entering into US session. Despite a significant downturn in Japanese equities earlier, European markets have remained resilient, with major indices post modest gains. In the commodities sector, oil prices continue their near term decline, driven by expectations of increased supply coupled with dampened demand projections. Conversely, gold is e confined to a narrow range as its recovery efforts are thwarted by strengthening Dollar. Meanwhile, Bitcoin, too, is facing challenges, failing to make a significant rally to conclude its consolidation that started after reaching record highs in March.

In the currency markets, Dollar is the strongest one for the day, making some progress in reversing its near term pullback. Swiss Franc is the second strongest followed by Euro. Aussie is the worst performer so far, followed by Yen , and then Kiwi. Canadian Dollar and Sterling are positioning in the middle.

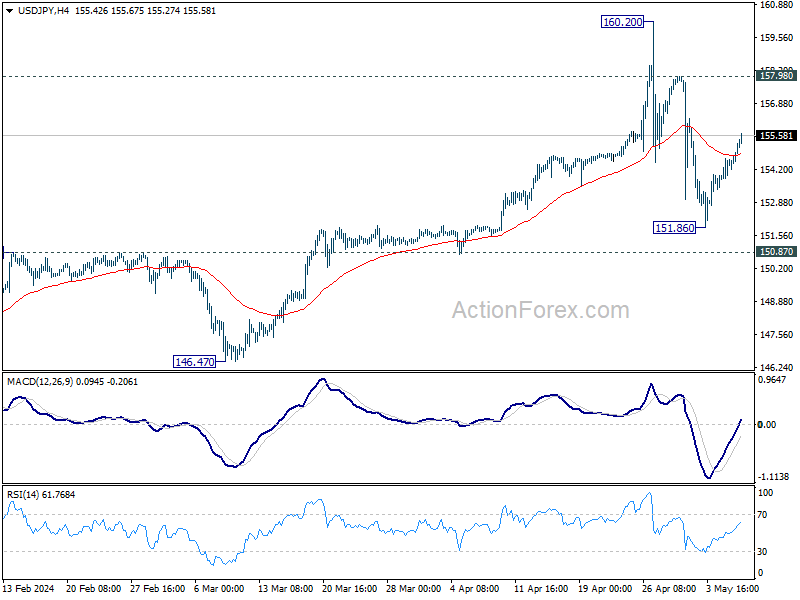

Yen would be a focus in the upcoming Asian session with Japan’s wage data and BoJ summary of opinions featured. From a technical point of view, the break of 55 4H EMA suggests that pull back from 160.20 has completed at 151.86 already. Further rise is now in favor back to 157.98 resistance. The question is on whether Japan would intervene again around this level.

In Europe, at the time of writing, FTSE is up 0.21%. DAX is up 0.09%. CAC is up 0.66%. UK 10-year yield is up 0.0159 at 4.149. Germany 10-year yield is up 0.048 at 2.471. Earlier in Asia, Nikkei fell -1.63%. Hong Kong HSI fell -0.90%. China Shanghai SSE fell -0.61%. Singapore Strait Times fell -1.08%. Japan 10-year JGB yield rose 0.0108 to 0.883.

WTI crude trends downward amid revised EIA supply and demand forecasts

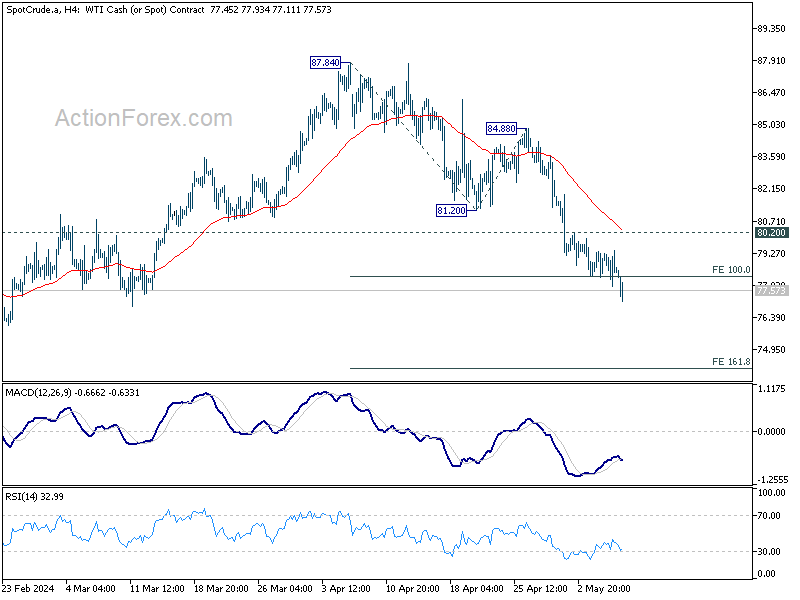

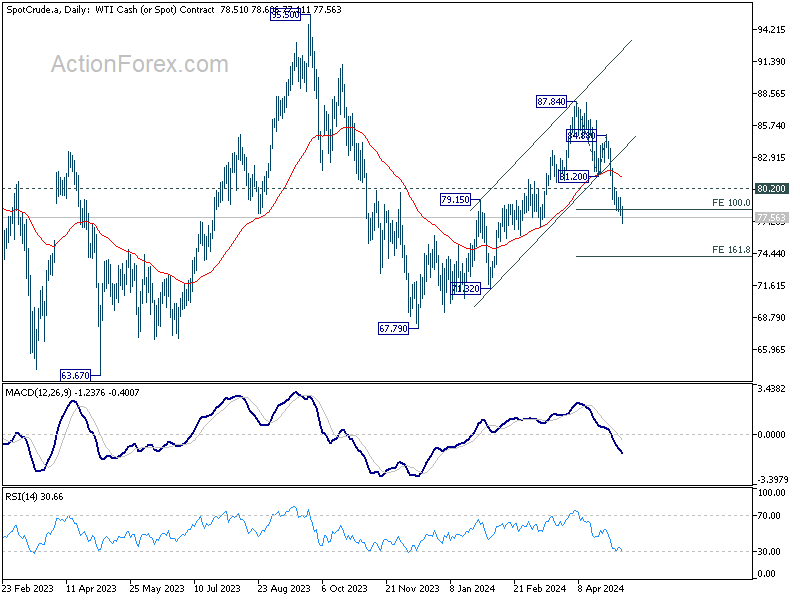

WTI crude oil is extending its near term decline today on expectation of higher production and lower demand ahead. If WTI cannot reclaim 80 mark in short term, there is prospect of downside acceleration through 70 next.

In its latest report, the US Energy Information Administration revised its expectations for this year’s global oil and liquid fuels output upwards while reducing its demand forecasts.

Notably, it now anticipates that global oil and liquid fuels consumption will increase by 920k bpd to 102.84m bpd, a slight reduction from the previously forecasted growth of 950k bpd.

On the production side, total world crude oil and liquid fuels production is expected to rise by 970k bpd to 102.76m bpd, up from the earlier estimate of 850k bpd increase.

Technically, the break of 100% projection of 87.84 to 81.20 from 84.88 at 78.24 suggests WTI is probably ready for downside acceleration. Near term outlook will stay bearish as long as 80.20 resistance holds. Next target is 161.8% projection at 74.13.

More importantly, the fall from 87.84 is seen as the third leg of the pattern from 95.50. There is prospects of deeper decline through 67.79 towards 63.67 (2023 low) in the medium term.

BoJ Ueda signals shift in focus to exchange rate impacts

In comments made to the parliament today, BoJ Governor Kazuo Ueda underlined growing focus on the effects of currency movements rather than solely on wages, signaling a broadening perspective on economic influences.

Ueda pointed out that as recent behavior in wage- and price-setting has become “somewhat more active,” BoJ has to be “mindful of the risk that the impact of currency volatility on inflation is becoming bigger than in the past.”.

“Foreign exchange rates make a significant impact on the economy and inflation. Depending on those moves, a monetary policy response might be needed,” Ueda said.

Similarly, Finance Minister Suzuki expressed significant concern about the negative aspects of a weaker yen, particularly the pressure it places on import prices.

“Since Japan relies on overseas markets for food and energy, and a large portion of its transactions are denominated in dollars, a weaker yen could raise prices of imported goods,” Suzuki said.

EUR/USD Mid-Day Outlook

Daily Pivots: (S1) 1.0739; (P) 1.0764; (R1) 1.0779; More…

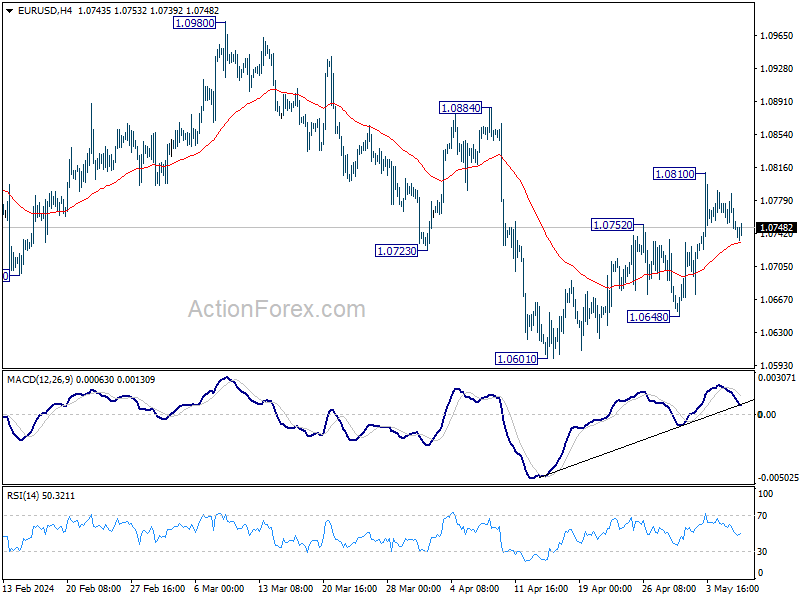

Intraday bias in EUR/USD stays neutral for the moment. More consolidations could be seen below 1.0810. Further rally is expected as long as 55 4H EMA (now at 1.0731) holds. On the upside, above 1.0810 will resume the rebound from 1.0601 to 1.0884 resistance next. However, firm break of 55 4H EMA will argue that the rebound has completed, and turn bias to the downside for 1.0648 support instead.

In the bigger picture, price actions from 1.1274 are viewed as a corrective pattern. Fall from 1.1138 is seen as the third leg and could have completed. Firm break of 1.1138 will argue that larger up trend from 0.9534 (2022 low) is ready to resume through 1.1274 high. On the downside, break of 1.0601 will extend the corrective pattern instead.

Economic Indicators Update

| GMT | Ccy | Events | Actual | Forecast | Previous | Revised |

|---|---|---|---|---|---|---|

| 06:00 | EUR | Germany Industrial Production M/M Mar | -0.40% | -1.10% | 2.10% | |

| 08:00 | EUR | Italy Retail Sales M/M Mar | 0.00% | 0.20% | 0.10% | |

| 14:00 | USD | Wholesale Inventories Mar F | -0.40% | -0.40% | ||

| 14:30 | USD | Crude Oil Inventories | -1.0M | 7.3M |

{kind=link}