Here are the latest developments in global markets:

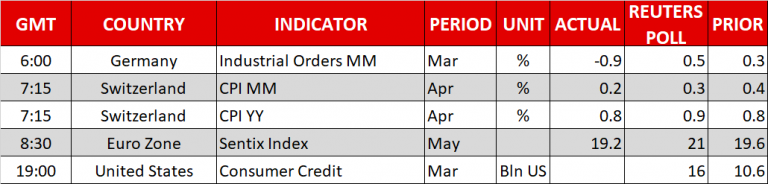

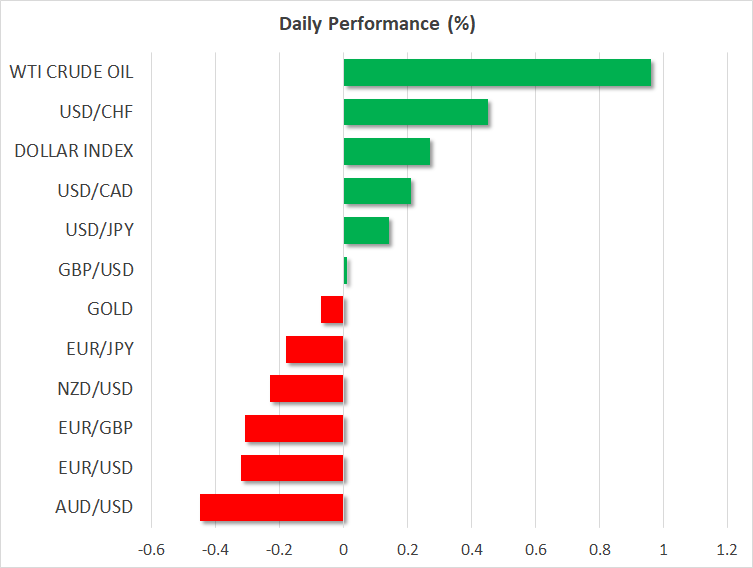

FOREX: The demand for greenback remained strong early in the European session, supported by rising confidence that the Fed, unlike its major counterparts, would keep pace with its stimulus reduction plans despite Friday’s nonfarm payrolls report showing wages growing less than expected. However, risks of a global trade war continued to hang in the background as trade talks between the US and Chinese negotiating teams last week failed to strike a deal. The dollar index rallied to an intra-day high of 92.82 (+0.26%) and dollar/yen reached a peak at 109.32 before it edged down to 109.25 (+0.13%). Euro/dollar extended today’s downfall to 1.1924 (-0.27%) as economic data out of the Eurozone continued to disappoint, with the Eurozone’s Sentix investor confidence index for May falling surprisingly to the lowest since February 2017 on Monday. German factory orders for March also missed forecasts of a growth of 0.5% today, dropping by 0.9% instead, while an ECB researcher warned through an Economic Bulletin article that “In the event of a significant increase in protectionism, the impact on global trade and output could be material.” Pound/dollar erased earlier gains, falling to 1.3534 (+0.02%), while euro/pound was struggling to rebound from 4-day lows, last seen at 0.8800 (-0.33%). In antipodean currencies, aussie/dollar and kiwi/dollar were under pressure in the face of a strengthening dollar, trading lower at 0.7508 (-0.42%) and 0.7000 respectively (-0.21%). Dollar/Lonnie rose to 1.2868 (+0.22%) ahead of the resumption of NAFTA talks today in Washington.

STOCKS: European stocks were mostly positive at 0930 GMT, with the pan-European STOXX 600 and the blue-chip Euro STOXX 50 being 0.15% and 0.01% up. Air France- KLM Group, Europe’s largest air carrier, was the worst performer among companies, with its stocks tumbling by 11.45% after its CEO resigned on Friday following a pay rejection by the staff which spurred strikes in the streets. The French CAC 40 inched up by 0.03%, with gains in the technology sector offsetting losses in telecommunications and financials, the German DAX 30 climbed by 0.36%, while the Italian FTSE MIB rose by 0.31%. UK stock markets were closed for a holiday.

COMMODITIES: Supply concerns lifted oil prices to fresh 3-year highs as hyper-inflated Venezuela headed into default. Analysts were also anticipating the US to pull out of the 2015 Iran nuclear deal on May 12 and reimpose sanctions on Iran as tensions between the two countries were still running high. WTI crude touched a new peak at $70.69/barrel before it fell to $70.41(+1.0%) and Brent hit a new top at $75.89 before it slipped to $75.55 (+0.91%). In precious metals, gold took off one-week highs, retreating to $1,313.90/ounce (-0.08%).

Day Ahead: Quiet day in terms of data; numerous speeches on the agenda

Monday is going to be quiet in terms of economic releases, while market liquidity is expected to be relatively narrower as UK markets are closed for a Bank Holiday today.

The US, the world’s largest economy, will see the release of March consumer credit data at 1900 GMT. Credit is predicted to tick higher by $16.0 billion from $10.6 billion the preceding month.

In terms of public speeches, Atlanta’s Fed President, Raphael Bostic (voting FOMC member in 2018), will be speaking at 1225 GMT, while at 1800 GMT, Richmond’s Fed President, Tom Barkin (voter) and Philadelphia’s Fed chief Patrick Harker (non-voter) will be making comments as well. A bit later, at 1930 GMT, the focus will turn to speeches made by the Dallas Fed President, Robert Kaplan, and the Chicago Fed President Charles Evans (both non-voters).

Early tomorrow, Australia will see the release of retail sales numbers at 0030 GMT; aussie pairs would be eyed. Month-on-month, sales are expected to expand by 0.3% in March versus 0.6% the prior month.

In equities, Walt Disney and Nvidia are two of the companies releasing results this week, on Tuesday and Thursday respectively. Equity market sentiment could be also driven by developments in global trade, as NAFTA talks are resuming today in Washington and US-China discussions seem to have provided no tangible outcome last week.