- USD/JPY’s current year-to-date outperformance has started to dissipate based on a shorter-term one-month rolling basis.

- A disappointing Japan Services PMI (flash) for October has failed to ignite an intraday bullish movement in USD/JPY.

- Three main factors that are likely to be the cause; intervention risk, inter-market expectations, and momentum.

- Watch the key 20-day moving average on the USD/JPY, now acting as support at 149.30.

The major uptrend phase of the USD/JPY in place since mid-January 2023 seems to be losing its bullish inertia even though it has recorded a year-to-date gain of +14.16% as of 24 October at this time of the writing, the best US dollar major pair ahead of the USD/CAD (+0.72%), USD/EUR (-0.15%), USDGBP (-1.78%), and USD/CHF (-3.78%).

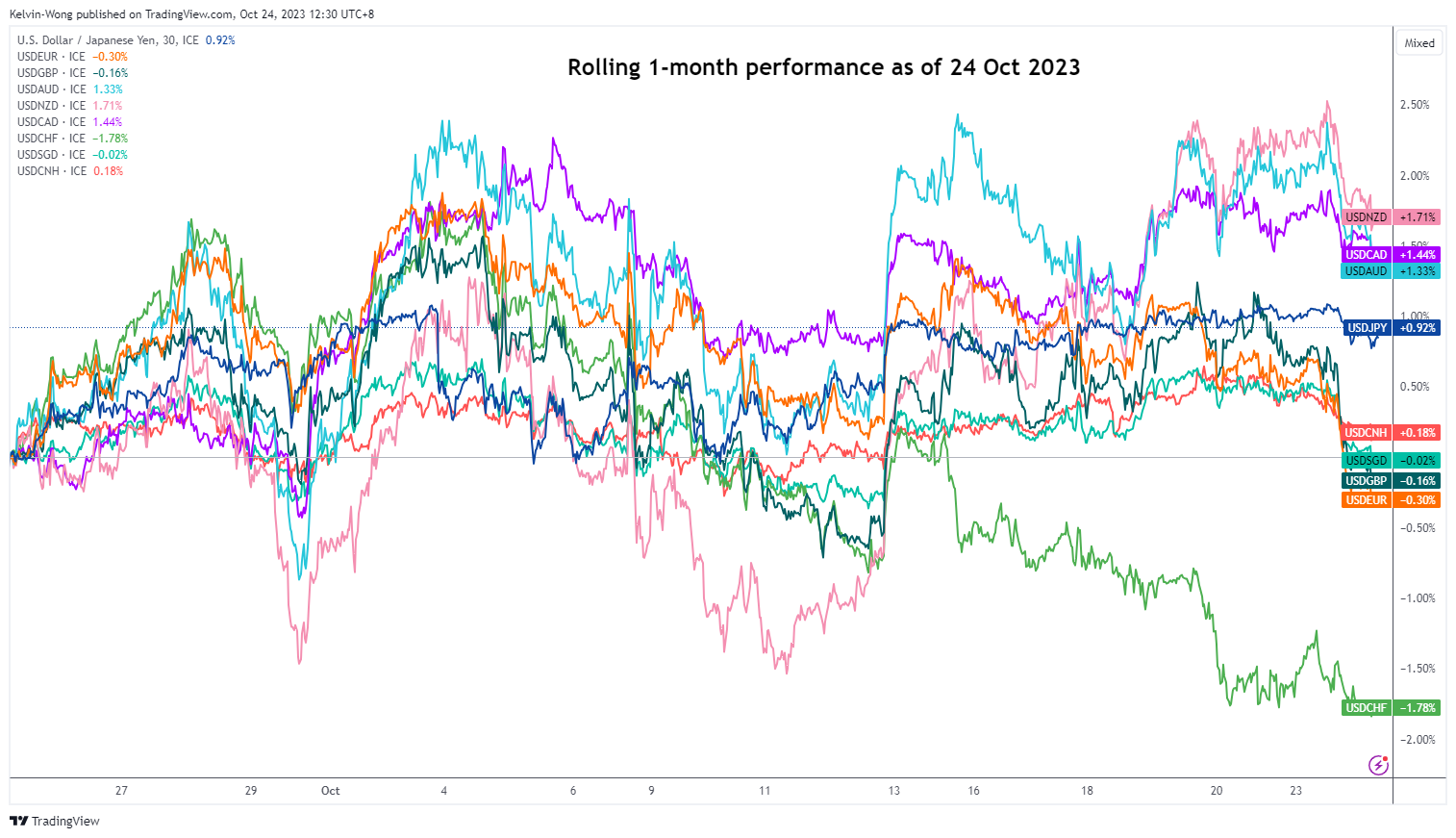

On a shorter horizon based on the one-month rolling performances of the major US dollar pairs as of 24 October 2023, the bullish momentum of the USD/JPY has started to dissipate from a peak of +1.16% to a current gain of +0.90% (see figure 1).

Fig 1: US dollar major pairs rolling 1-month performances as of 24 Oct 2023 (Source: TradingView, click to enlarge chart)

A disappointing Services PMI has failed to ignite a rally in USD/JPY

Also, today’s weak Japan’s flash Services PMI print for October came in below expectations (51.1 versus 52.9 forecasted & 53.8 in September) where the growth in the services sector slowed to a ten-month low has failed to ignite a short-term intraday bullish movement in the USD/JPY.

In the past, disappointing key economic data in Japan tended to lead to a bid in USD/JPY as market participants upped the expectations of the Bank of Japan (BoJ) to delay monetary policy normalization away from short-term negative interest rates which in turn maintained the policy divergence status quo between the BoJ and US Federal Reserve as well as the rest of the world’s central banks that have pivoted away from either zero or negative interest rates since 2022.

What is causing the lack of bullish enthusiasm in USD/JPY?

There are three possible factors; intervention risk from policymakers, inter-market expectations, and momentum.

Firstly, verbal interventions in the past two months by Japan’s Ministry of Finance (MoF) officials have been drummed up as the JPY weakened considerably against the US dollar due to robust key US economic data that increased the odds of the Fed’s current stance of keeping US interest rates at a higher level for a longer period.

Also, MoF’s verbal intervention is likely to have morphed into a recent real intervention in the foreign exchange market to halt the pace of JPY weakness on 3 October where the USD/JPY printed an intraday high of 150.16 during the start of the US session before it tumbled significantly by -282 pips to hit an intraday low of 147.34 within a short span of just five minutes even though there was no official intervention confirmation by MoF officials.

Therefore, in the minds of market participants, the USD/JPY’s psychological level of 150 has subconsciously become the “line in the sand” that increases the risk of FX intervention when the movement of the USD/JPY probed close to around 150.

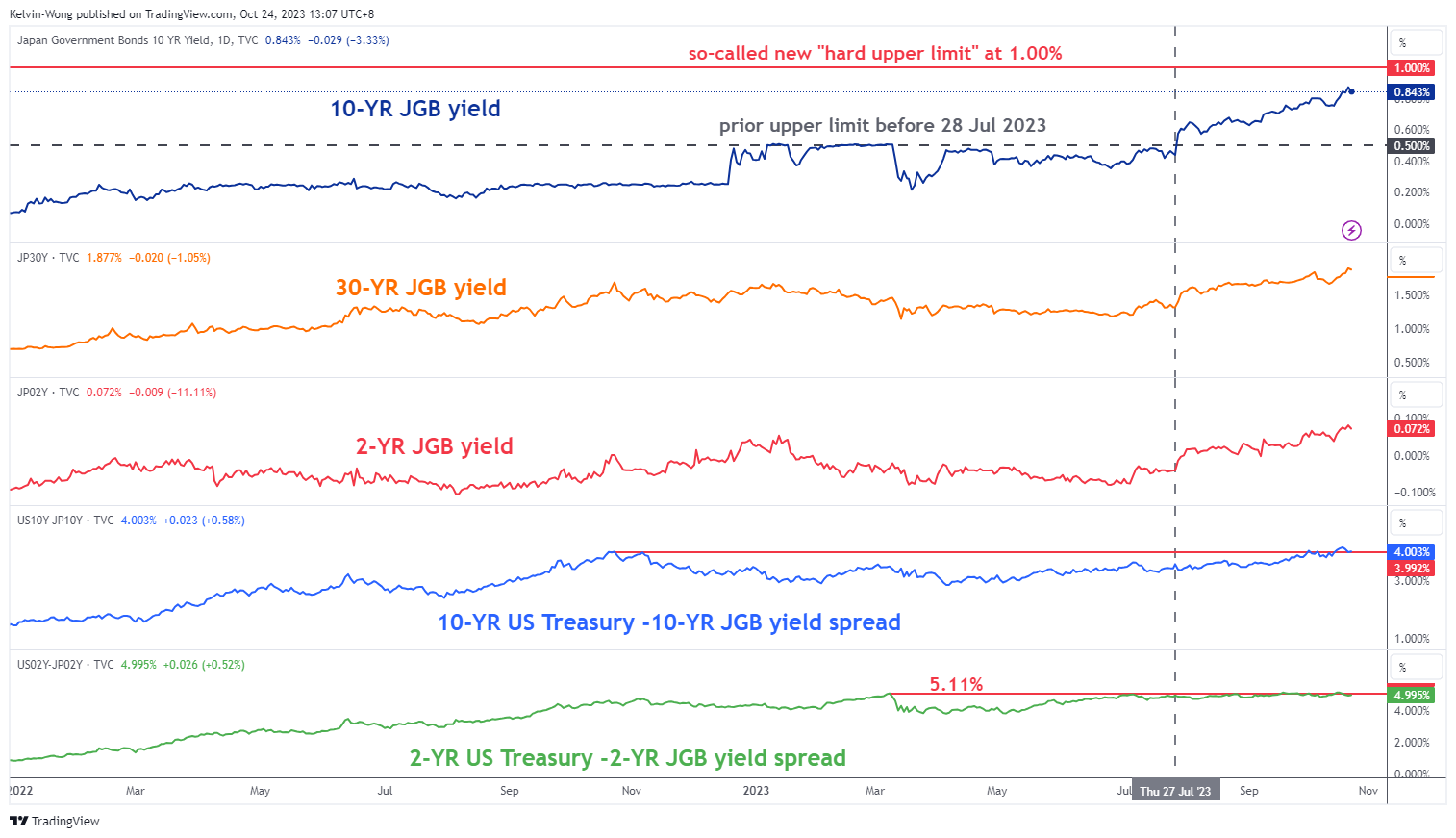

Fig 2: JGB yields & yield spread with US Treasuries as of 24 Oct 2023 (Source: TradingView, click to enlarge chart)

Secondly, the shorter-term 2-year yield spread premium of the US Treasury not over the Japanese government bonds (JGB) has started to narrow since 28 July after the implementation of “flexible yield curve control” on the 10-year JGB yield by BoJ. Also, it has failed to break above its current year-to-date peak of 5.11% printed in March 2023 (see figure 2).

The 2-year sovereign yield tends to be more sensitive to a central bank’s monetary policy and the 2-year JGB yield has jumped significantly from -0.04% to 0.07% at this time of the writing due to increasing expectations that BoJ is likely to scrap its short-term negative interest rates policy by the first half of 2024.

In addition, recent data from Japan’s overnight index swap curve has indicated a 20% chance that BoJ will end negative interest rates in December 2023, and the probability rises to 100% by April 2024.

Thirdly, the medium-term bullish momentum of the USD/JPY as indicated by the daily RSI indicator has flashed a bearish divergence condition just below a medium-term resistance of 150.30 (see figure 3).

Fig 3: US/JPY medium-term & major trends as of 24 Oct 2023 (Source: TradingView, click to enlarge chart)

This technical observation suggests an easing of bullish momentum. A clear break with a daily close below the key 20-day moving average (price actions have traded above it since 31 July 2023) now acting as support at 149.30 increases the odds of a potential multi-week bearish reversal towards the medium-term support at 144.80.

, USD/EUR (-0.15%), USDGBP (-1.78%), and USD/CHF (-3.78%).){kind=link}