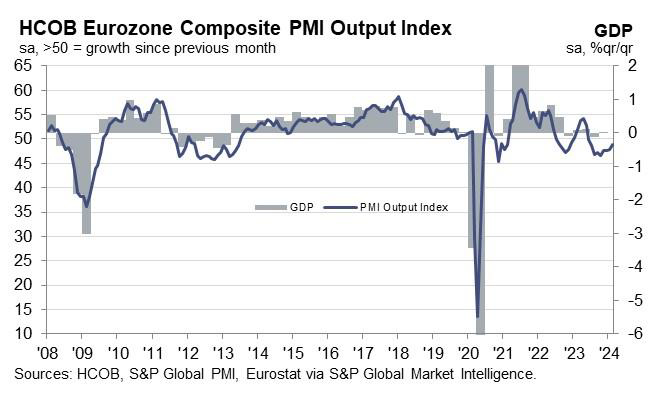

Eurozone PMI Manufacturing dipped further from 46.6 to 46.1 in February, undershooting expectations of a 47.1 reading and signaling continued contraction. Conversely, PMI Services climbed from 48.4 to neutral mark of 50.0, surpassing the forecast of 48.7 and reaching a 7-month high. This uplift in services contributed to PMI Composite’s rise from 47.9 to 48.9, marking an 8-month peak yet still indicating slight overall economic contraction.

Norman Liebke, Economist at Hamburg Commercial Bank, cited a “glimmer of hope” as Eurozone edges closer to recovery, particularly within the services sector. Despite the manufacturing downturn, Liebke reaffirms an annual growth forecast of 0.8% for 2024.

ECB is likely to find the latest PMI figures concerning, especially with output prices increasing for the fourth consecutive month, largely driven by labor-intensive services sector grappling with rising wages. ECB is anticipated to make its first interest rate cut in June according to Liebke’s forecast.

The disparity in economic performance between Germany and France is striking. Germany, Europe’s largest economy, appears to be a significant “drag” on the broader Eurozone growth, with its manufacturing sector facing pronounced challenges. In contrast, France is experiencing a more robust recovery across both services and manufacturing.

Germany’s PMI readings for February further underscore its economic difficulties, with PMI Manufacturing plummeting to a 4-month low of 42.3, PMI Services rising from 48.2 and Composite PMI also hitting a 4-month low at 46.1.

On the other hand, France’s economic indicators offer more positive news, with PMI Manufacturing surging to an 11-month high of 46.8, Services PMI rising to an 8-month high at 48.0, and PMI Composite reaching a 9-month high at 47.7.

{kind=link}