{kind=link}

Crude oil prices slipped on Monday after OPEC+ announced another production boost, this time for September. The group confirmed a planned hike of 547k barrels per day, continuing its aggressive push to regain global market share after years of output cuts meant to prop up prices.

The shift began in April with a small supply increase, but since then OPEC+ has stepped on the gas. May through July each saw 411k bpd added, with larger hikes of 548k in August and now 547k bpd set for September.

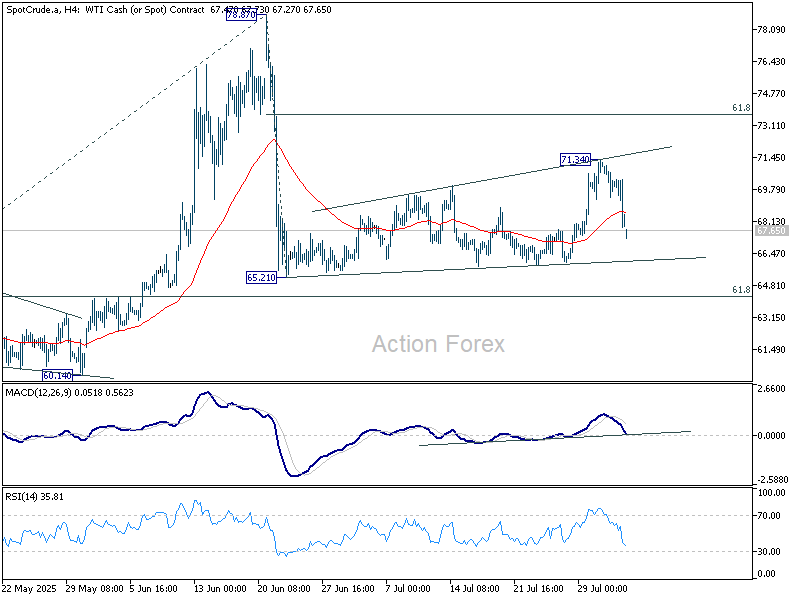

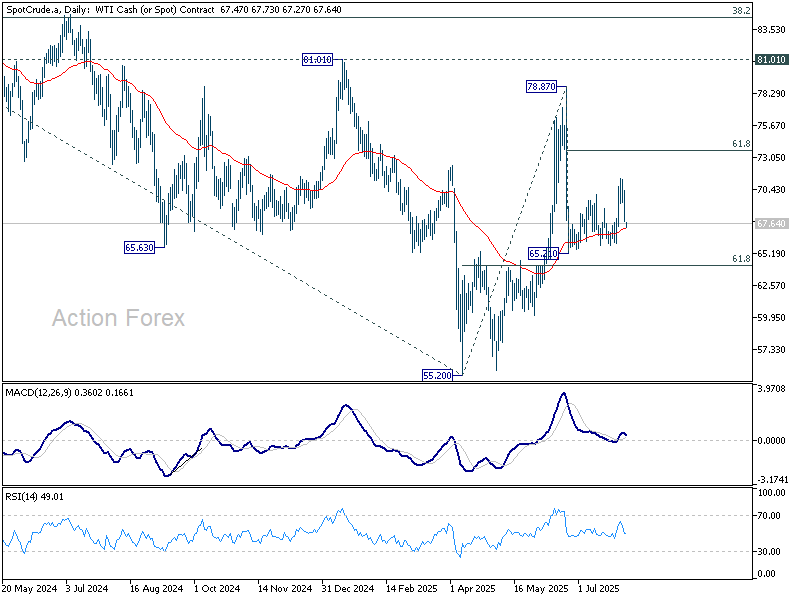

Despite briefly surging to nearly 79 in June amid Middle East tensions, WTI crude reversed sharply after the Israel–Iran ceasefire and dropped back to as low as 65.21. The bounce to 71.34 last week failed to sustain, and prices have turned lower again, signaling ongoing sideways consolidation rather than a breakout.

Technically, oil remains trapped in a range. Downside should be anchored near 65, upside appears capped below $73.65. However, even in event of a bounce through 71.34, momentum is expected to fade as oversupply concerns and tepid demand limit further gains below 61.8% retracement of 78.87 to 65.21 at 73.65.